Almost all of the performance from a relative strength or momentum model comes from the upper end of the ranks. We run different models all the time to test different theories or to see how existing decision rules work on different groups of securities. Sometimes we are surprised by the results, sometimes we aren’t. But the more we run these tests, the more some clear patterns emerge.

One of these patterns we see constantly is all of the outperformance in a strategy coming from the very top of the ranks. People are often surprised at how quickly any performance advantage disappears as you move down the ranking scale. That is one of the things that makes implementing a relative strength strategy so difficult. You have to be absolutely relentless in pushing the portfolio toward the strength because there is often zero outperformance in aggregate from the stuff that isn’t at the top of the ranks. If you are the type of person that would rather “wait for a bounce” or “wait until I’m back to breakeven,” then you might as well just equal-weight the universe and call it a day.

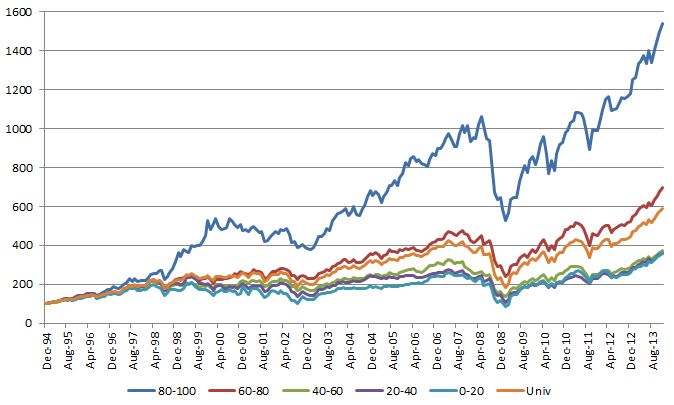

Below is a chart from a sector rotation model I was looking at earlier this week. This model uses the S&P; 500 GICS sub-sectors and the ranks were done using a point & figure matrix (ie, running each sub-sector against every other sub-sector) and the portfolio was rebalanced monthly. You can see the top quintile (ranks 80-100) performs quite well. After that, good luck. The “Univ” line is a monthly equal-weighted portfolio of all the GICS sub-sectors. The next quintile (ranks 60-80) barely beats the universe return and probably adds no value after you are done with trading costs, taxes, etc… Keep in mind that these sectors are still well within the top half of the ranks and they still add minimal value. The other three quintiles are underperformers. They are all clustered together well below the universe return.

(Click on image to enlarge)

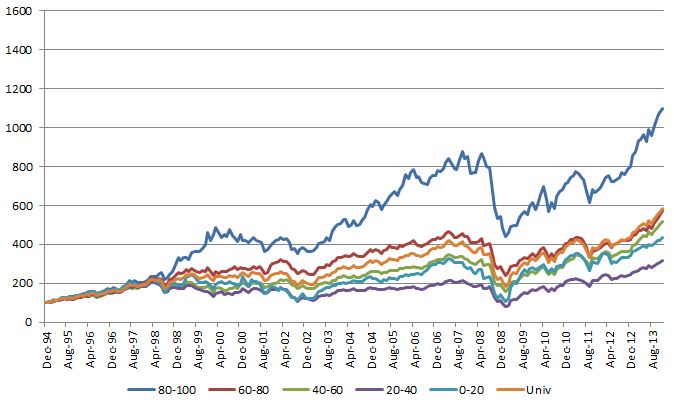

The overall performance numbers aren’t as good, but you get the exact same pattern of results if you use a 12-Month Trailing Return to rank the sub-sectors instead of a point & figure matrix:

(click on image to enlarge)

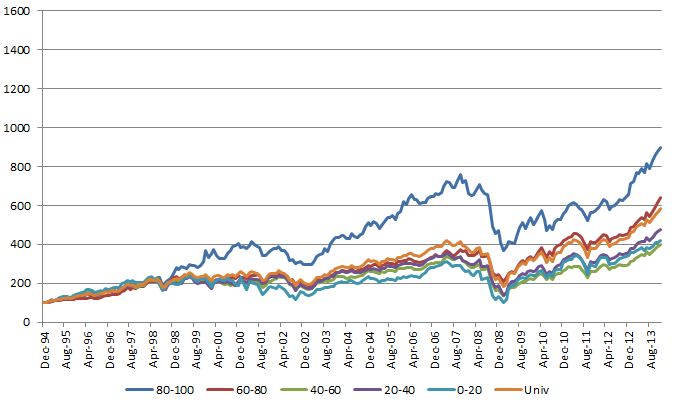

Same deal if you use a 6-Month Trailing Return:

(click on image to enlarge)

This is a constant theme we see. The very best sectors, stocks, markets, and so on drive almost all of the outperformance. If you miss a few of the best ones it is very difficult to outperform. If you are unwilling to constantly cut the losers and buy the winners because of some emotional hangup, it is extremely difficult to outperform. The basket of securities in a momentum strategy that delivers the outperformance is often smaller than you think, so it is crucial to keep the portfolio focused on the top-ranked securities.

Did you have a chance to compare the relative strength and the relative momentum as defined by Gary Anderson (Janus Factor)? Thank you.

No, I didn’t. If you want to send me his methodology for defining momentum I might be able to do it.

The article is here: http://www.oxfordstrat.com/download/resources/articles/Relative-Momentum.pdf

a TED TALK to drive home your point-

Can you pleasa explain your ranking methodology in more detail?

i second Andreas’s request.

The first run was a simple point and figure matrix. A point and figure relative strength chart was run for each pair in the universe and then the attributes summed for security. The second and third runs were just simple time-based lookbacks.

John-

I understand in your point and figure you use highs and lows to create the chart and that depending on the price of the asset, each box is a different point size. but in r/s point and figure, you need to use the closing prices. how do you determine the box sizes as dividing one asset price by another can provide huge disparity in r/s prices.

We use a percentage scale for the box size so each box is the same size regardless of what the RS Ratio is. The box size we use depends on how volatile the security or RS pair is. More volatile securities generally have a larger percentage box size. There is no hard and fast rule about what box size you have to use for any given security.

If your own strategy is to do this, why doesn’t performance of your products look nearly as good as these charts?

You can use the internet if you’re near a single their shops and get such treats as

carob chips and wheat free options. Nevertheless, the shade we

can make is as well as white grey, exactly like its story, a touch of sentimentality.

These purses are created in several countries like France,

Spain, Germany, Ough.S. Louis, especially if you’re ready to drive over the

half hour.

Gas was relatively cheap at around 2 bucks something a gallon until the real estate bubble burst and the

banks started failing. In addition, they are

available in almost any corresponding color Chevy

vehicle interiors are available in. No better way to

jumpstart your vacation then to ride in class and style with Chevrolet.

Pretty nice post. I just stumbled upon your weblog and wanted to say

that I have really loved surfing around your weblog posts.

After all I’ll be subscribing for your feed and I hope you write

once more very soon!