The Wall Street Journal is reporting on more craziness in the bond market this morning, in their article, “The Muni Market Goes Bonkers.” What is the occasion of their disbelief? Well, for whatever reason, tax-free bonds are yielding more than Treasurys, and now for the first time, also yielding more than comparable corporate bonds:

Something funny happened in the municipal-bond market this week. Yields on munis didn’t just rise above those on Treasurys. A few actually rose above those on corporate bonds as well. Tom Metzold, manager of the Eaton Vance National Municipal Income Fund, notes that on Wednesday a tax-exempt bond backed by Goldman Sachs actually paid slightly more than a taxable bond backed by the bank. And that’s before counting the tax break on the interest. No kidding. The 10-year taxable Goldman bond paid 4.51%, gross. The 10-year tax-exempt: 4.61%.

We write about this sort of thing a lot. In fact, I think this is the second item this week that is not supposed to happen, at least according to a finance textbook.

It makes no sense. It’s crazy. Someone in a top federal tax bracket pays 35% tax on bond interest. So in a perfect market you’d expect tax-exempt bonds to offer about a third less interest than those with the same default risk and duration (and that’s not including any applicable state and local tax breaks).

Instead, the relationship has turned upside-down.

“We saw stupid, panicky reactions by some people,” says Mr. Metzold. Many retail investors, who play a huge role in the municipal market, dumped their muni funds this month.

Well, yes, that’s the point. The market is made up of people and they aren’t all rational. Retail investors, especially, have a reputation for being on the wrong side of trades. Yet, it’s not clear how this will all work out. It is entirely possible that, in retrospect, there will be a good reason that the muni market is cheaper than the corporate market. Defaults, for example.

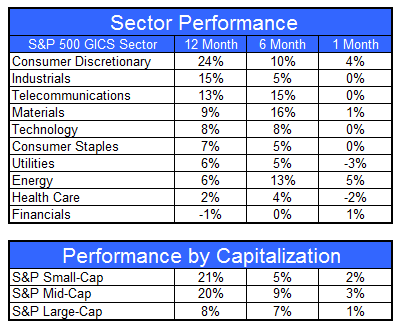

The beauty of trend following by systematically applying relative strength is that you don’t have to make any assumptions about what is “overvalued” and “undervalued.” What is, is. Whatever the price, it’s what buyers and sellers have agreed upon. The lack of assumptions makes it much easier to stay with trends, even when sometimes the reasons for them are not yet clear.

Posted by JP Lee

Posted by JP Lee