Sector has been a popular investment strategy for many years. The proliferation of sector based exchange traded funds has made it quick and easy to implement sector bets, but has also added a level of complexity to the process. There are now many different flavors of ETF’s for each macro sector ranging from simple capitalization weightings to semi-active quantitative models to construct the sector index. The vast array of choices in each sector allows investors to potentially add additional performance over time versus a simple capitalization based model.

Dorsey, Wright has a suite of sector indexes based on our Technical Leaders Momentum factor. These indexes are designed to give exposure to the securities with the best momentum characteristics in each of the 9 broad macro sectors (Telecomm is split between Technology and Utilities depending on the industry group). Long time readers of our blog should be aware of all of the research that demonstrates how effective the momentum factor has been over time providing returns above a broad market benchmark. Using indexes constructed with the momentum factor have the potential to add incremental returns above a simple capitalization weighted sector rotation strategy just like they do on the individual stock side.

The sector SPDRs are the most popular sector suite of exchange traded products. When investors make sector bets using this suite of products they are making a distinct sector bet and also making a bet on large capitalization stocks since the sector SPDRs are capitalization weighted. There are times when large cap stocks outperform, but there are also times when the strength might be in small cap, value, momentum, or some other factor. By not considering other weighting methodologies investors are potentially leaving money on the table.

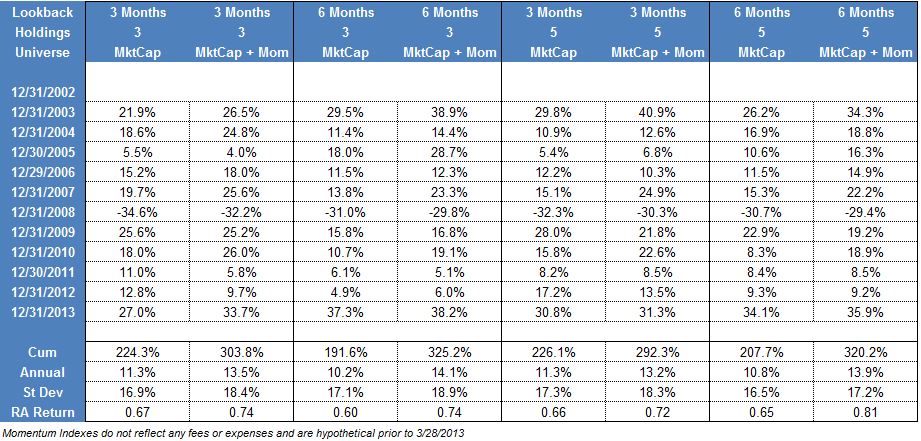

We constructed several very simple sector rotation models to determine how returns might be enhanced by implementing a sector rotation strategy with indexes based on momentum. The base models were created with either 3 or 5 holdings from the sector SPDR universe. Each month a trailing 3 or 6 month return was calculated (based on the model specification) and the top n holdings were included in equal weights in the portfolio. Each month the portfolio was rebalanced with the top 3 or 5 sector SPDRs based on the trailing return. This is an extremely simple way to implement a momentum based sector rotation strategy, but one that proves to be surprisingly effective.

The second group of portfolios expanded the universe of securities we considered to implement the strategy. All of the momentum rankings were still based on the trailing returns of the sector SPDRs, but we made one small change in what was purchased. If, for example, the model selected Healthcare as one of the holdings we would buy either the sector SPDR or our Healthcare Momentum Index. The way we determined which version of the sector to buy was simple: whichever of the two had the best trailing return (the window was the same as the ranking window) was included in the portfolio for the month. In a market where momentum stocks were performing poorly the model would gravitate to the cap weighted SPDRs, but when momentum was performing well the model would tend to buy momentum based sectors. Making that one small change allowed us to determine how important implementing the sector bet actually was.

(Click Image To Enlarge)

The table above shows the results of the tests. Trials were run using either 3 or 6 month look back windows to rank the sectors and also with either 3 or 5 holdings. In each case, allowing the model to buy a sector composed of high momentum securities was materially better than its cap weighted counterpart. Standard deviation also increased, but the returns justified the increased volatility as the risk adjusted return increased in each case.

This is one simple case illustrating how implementing your sector bests with different sector construction philosophies can be additive to investment returns. The momentum factor is one of the premier investment anomalies out there, and using a basket of high momentum stocks in a specific sector has shown to increase returns in the testing we have done.

The performance numbers are not inclusive of any commissions or trading costs . The Momentum Indexes are hypothetical prior to 3/28/2013 and do not reflect any fees or expenses. Past performance is no guarantee of future returns. Potential for profit is accompanied by potential for loss. The models described above are for illustrative purposes only and should not be taken as a recommendation to buy or sell any security or strategy mentioned above. Click here for additional disclosures.