Peter Chiappinelli in Advisor Perspectives sheds some interesting light on the active versus passive debate as it relates to fixed income exposure. See below for a few excerpts of his recent article.

The trends are clear. 2016 was the year in which the investment community warmly embraced passive portfolios. Our worry, however, is that investors are feeling a false sense of security, particularly with passive bond portfolios–namely those funds and Exchange Traded Funds (ETFs) linked to a common benchmark, the Bloomberg Barclays U.S. Aggregate Bond Index (the Agg). There is nothing passive about this index, and we would argue it is aggressively taking on more risk at the worst possible time. There are three main reasons for our concern: the simple math of bond duration; the changing composition of the index; and the very logical financing behavior of corporate borrowers.

Bond math and duration

Without doing a rehash of intricate bond math, duration is an important calculation of bond risk. Though it has many variants, at its root duration measures the sensitivity of a bond’s price to a shift in yields. For example, a bond (or a bond portfolio) with a duration of 5 years means that for every 1% shift upwards in yields, there is a 5% drop in the price of the bond. Duration is measured in years because it is a function of the timing and magnitude of a bond’s cash flows (coupons and principal repayment): the more distant the cash flows, the higher the sensitivity (i.e., higher risk) to a change in interest rates, all else held equal. The cleanest example of this is the 30-year zero-coupon bond, which pays a single massive cash flow 30 years down the road, and therefore this bond has a duration of exactly 30 years. There are no coupon payments along the way that would dampen its sensitivity to a change in yields. Generally speaking, the smaller the coupon, the higher the duration (and vice versa); the longer the maturity, the higher the duration (and vice versa). That’s just how the math of bond risk works.

Unfortunately for investors in passive bond portfolios or ETFs tied to the Agg, bond math is making this “safer” bond portfolio much riskier than it was even a few years ago. It is now much more sensitive to a possible rise in bond yields (as we saw in November) due simply to a lower “cushion” of coupons. As shown in the chart below, coupons have dropped dramatically since the Financial Crisis of 2008 and the introduction of Quantitative Easing by the Federal Reserve (Fed). For many years leading up to 2008, the Agg happily paid its investors a healthy coupon of over 5%, but today it is a measly 3%, a number that is among some of the lowest ever recorded. This is problem number one.

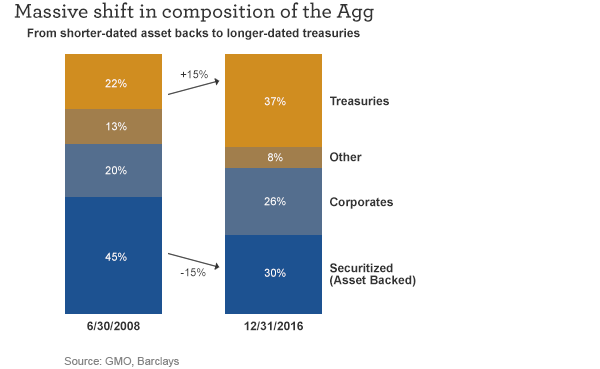

Changing composition of the Agg

Problem number two is that the Agg has dramatically changed its stripes since the Financial Crisis. Eight years ago, the largest bond sector was securitized loans (e.g., asset-backed securities, mortgage-backed securities), and most of these types of securities have shorter maturities and duration. Today, longer-dated Treasuries are now the dominant sector of the Agg, while securitized bonds have dropped off significantly. This, again, has shifted both the maturity and duration of the Agg upward.

Click here for the rest of Chiappinelli’s article, but following paragraph is a nice conclusion to his analysis:

The bond math of lower coupons, the changing composition of the Agg, and the issuance of longer-maturity bonds by corporate America all conspired to increase risk, at possibly the worst time. By any reasonable fiduciary standard, this was a time to be reducing duration, yet the Agg, and the passive bond portfolios and ETFs tied to it, has seen a 62% increase in duration over the past 8 years. There is nothing passive about the Agg–it has actually become more aggressive! Be careful.

Contrary to popular belief, passive does not necessarily mean static. The composition of the Aggregate Bond Index has changed dramatically over time and this has important implications for its investors. Part of the reason that we introduced our Tactical Fixed Income portfolio (available as a separately managed account) in 2013 is that we thought that we were likely entering a period of time where active could be increasingly important in the fixed income space. See below for the FAQ on this strategy:

Why is there a need for Tactical Fixed Income?

Bond buyers face a dilemma. Yields are very, very low. If interest rates stay low this low, bondholders are facing minimal returns, all the while having those returns eaten away by inflation. If interest rates rise, bondholders are facing potentially significant capital losses. Both outcomes, obviously, are problematic. This situation demands a tactical solution that can manage through either outcome.

At Dorsey Wright, we have taken our time-tested relative strength tools and have applied them in a unique way to the fixed income markets. This solution is now available as a separately managed account. We think it will be welcome news for bond holders and prospective bond buyers who are grappling with the current bond market dilemma. Equally important, we think it will be a robust solution in the future across a broad range of possible interest rate environments.

What is the investment universe for the Tactical Fixed Income strategy?

The Tactical Fixed Income strategy can invest in short-term and long-term U.S. Treasurys, inflation-protected bonds, corporate, convertible, high yield, and international bonds. This is a broad universe of fixed income types that have varying yields and volatility characteristics.

How is the risk managed in the Tactical Fixed Income portfolio?

The Tactical Fixed Income model structures the portfolio in a way that balances risk and reward. Certain types of fixed income behave better in “risk-on” environments, while other fixed income categories are more defensive. Our model is built to ensure that the portfolio remains diversified. It’s very important to understand that this is designed as core fixed income exposure. We’re trying to generate good fixed income returns, without creating equity-like volatility.

Our model compares the relative strength of all of the ETFs in the investment universe. Those fixed income sectors exhibiting the strongest trends will be represented in the portfolio.

How does the strategy handle a rising rate environment?

Although the general trend of interest rates has been down over the past three decades, there have been periods where rates have generally risen. The period of mid-2003 to mid-2007 was generally a period of rising interest rates, while the period of mid-2007 to late 2016 was generally been a period of declining interest rates. Sectors like long term government bonds tend to perform much better in a declining interest rate environment while sectors like convertible bonds tend to perform much better during rising rate environments.

Our Tactical Fixed Income strategy is designed to be adaptive and seeks to add value in both environments.

Will the strategy invest in inverse bond ETFs?

We do not use inverse bond ETFs in the portfolio due to the cost of carrying the short positions, which includes the management fees of the ETFs as well as paying out the interest payments while you own these funds. However, a rising rate environment typically is accompanied by a strong economy. We do have ample ability to have exposure to sectors of the fixed income market, like high yield, international, and convertible bonds, that may perform well during these environments.

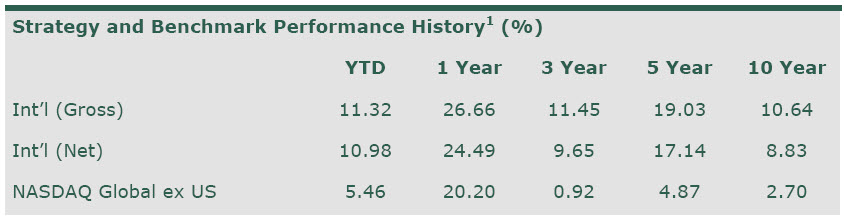

How has the strategy performed since it was introduced in March 2013?

We have been pleased with the performance of this strategy. As shown below, it has outperformed the Barclays Aggregate Bond Total Return Index since inception:

As of 2/28/17

To receive the fact sheet for this portfolio please e-mail [email protected] or call 626-535-0630.

Net performance shown is total return net of management fees for all Dorsey, Wright & Associates accounts, managed for each complete quarter for each objective. The advisory fees are described in Part II of the adviser’s Form ADV. All returns since inception of actual Accounts are compared against the Barclays Aggregate Bond Index. A list of all holdings over the past 12 months is available upon request. The performance information is based on data supplied by the Manager or from statistical services, reports, or other sources which the Manager believes are reliable. There are risks inherent in international investments, which may make such investments unsuitable for certain clients. These include, for example, economic, political, currency exchange, rate fluctuations, and limited availability of information on international securities. Past performance does not guarantee future results. In all securities trading, there is a potential for loss as well as profit. It should not be assumed that recommendations made in the future will be profitable or will equal the performance as shown. Investors should have long-term financial objectives when working with Dorsey, Wright & Associates.