How much you can pull from a retirement portfolio depends, of course, on how much it earns over time. Spending policies are going to become a big focus in the financial industry because the big demographic bump from the Baby Boom is going into retirement right now. Every year for the next fifteen or so, all of us will be dealing with more retirees nervous about making their money last. Chances are that you are already experiencing this in your business, but you are still at the tip of the demographic iceberg.

Pensions everywhere, corporate and government, are potentially underfunded by trillions of dollars. Again, it all depends on the return expectations. In the most recent issue of Investments & Wealth Monitor (sorry, behind a pay wall), author Christopher Brightman cites an expected return study by Research Affilates. The study uses beginning dividend yield, long-term real earnings growth, and implied inflation to forecast the expected equity return for the market. It uses the beginning bond yield to forecast the expected return for bonds. The expected return that is derived is a 10-year estimate. Based on their forecasting method, their average gross error was about 2.1% (+ or -) between the expected return for the decade and the actual realized return.

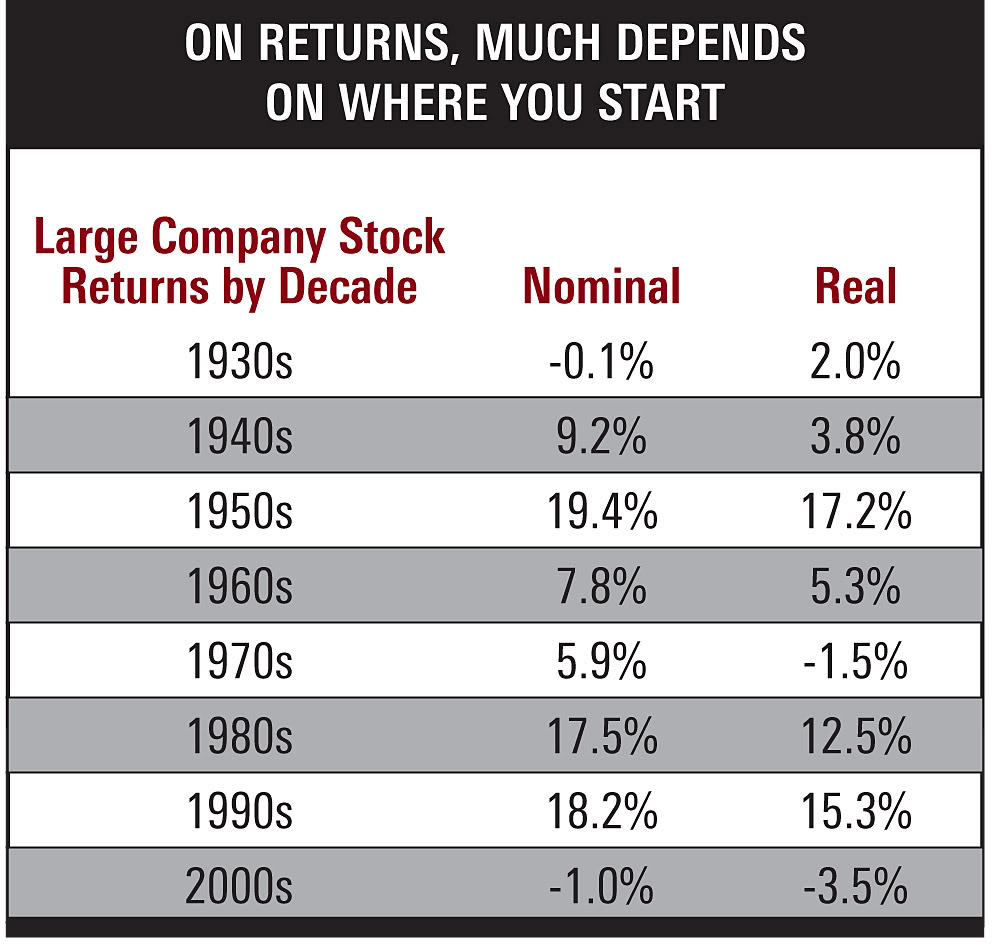

There is no real precision in forecasting, obviously, but there may be some merit in altering expectations depending on your starting place. Reported performance, even for an individual account, is extremely dependent on the starting and ending points. Consider, for example, this table from an article on performance at AdvisorOne:

Source: AdvisorOne (click on image to enlarge)

A spending policy that seemed prudent during the 1980s and 1990s is going to freak out a client in the current environment.

The concept of fecundity, as espoused by James Garland, may provide both a simple spending rule and serve as a proxy for estimating returns. Garland points out that you can’t sustainably spend all of your earnings (dividends + capital gains), but you can probably spend more than just the income because there is often some capital growth over time. His rule of thumb is that sustainable spending is about 130% of the yield on the major indexes. By combining this data with some of the inputs in the Research Affiliates estimation process, I discovered that return estimates with a similar average gross error (2.0% + or -) could be calculated. All of the inputs are readily available. Just for fun, here’s where we are now.

Current S&P; 500 yield: 2.0%

Current breakeven 10-year yield: 2.3%

Current US 10-year note yield: 2.0%

60/40 balanced account return expectation over next 10 years:[( ( 1.3 x 2.0% ) + 2.3% ) x .6] + [2.0% x .4] = 3.74%

The equity return expectation is 4.9% (130% of yield + expected inflation) and the bond return expectation is 2.0% (the current yield).

If that number seems low to you, I would suggest that pushing a client to save diligently and invest intelligently is going to be very important to your Baby Boomer retirees. There’s still time for a lot of the Baby Boom generation, although some of them might need a kick in the pants.

I also feel pretty certain that even if the equity market return is 4.9% for the next decade that there will be other markets where returns are much higher, or years when the equity market does much better than 4.9%. It’s important to be aware of global trends and asset class returns. To make money over time, you at least need to have a sense for where the action is. In other words, what is showing the best relative strength?