To read Part 1 click here

The first post in this series laid out the background for a Core Equity strategy. The goal is to use different factor strategies to create a more efficient portfolio than what you would get from traditional cap weighting.

The Value and Low Volatility strategies actually have a momentum component to them. As I mentioned in the background post, we work with momentum all the time so it is easy for me to incorporate that with other factors to try and improve returns. I realize this will lower some of the correlation benefits, but I think the potential return trade-off is worth it.

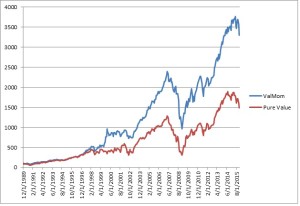

The graph below shows two versions of a Value model. The Pure Value model selects the 100 cheapest stocks based on a composite indicator of Price/Sales, Price/Book, Price/Free Cash Flow, and Price/Earnings. The Pure Value model below rebalances the portfolio quarterly with the 100 cheapest stocks out of a universe of the top 1000 market cap names. The ValMom model uses the same value composite ranking system, but requires the stocks to be on a Point and Figure Buy Signal plus be in a Column of X’s. For those of you not familiar with Point and Figure relative strength, this simply means the stock has been outperforming the broad market on an intermediate and long-term basis.

You can see adding the momentum overlay to the value strategy is beneficial to returns. Essentially, this helps filter a lot of the value traps. More experienced Value investors have other methods to accomplish this goal, but adding the momentum overlay is something that works very well for what we do.

I did the same thing with the Low Volatility model. This model picked 100 stocks with the lowest trailing one year daily standard deviation from a universe of 1000 top market cap names. The portfolio was rebalanced quarterly. Adding a momentum overlay helps ensure you have a portfolio of stocks that isn’t volatile, but has also demonstrated the ability to outperform the broad market over time. Again, this will cut in to some of the correlation benefits of the factor strategies, but I think the return tradeoff is worth it.

Adding the momentum overlay doesn’t improve returns as much as the Value example above, but it definitely does help.

The next post will detail the actual models I used for the factor strategies inside of the Core Equity model, but what has been discussed above is the basis for why I’m doing a couple of things differently than other models you might see and why the final model will have more of a momentum tilt.

The returns used within this article are the result of a back-test using indexes that are not available for direct investment. Returns do include dividends, but do not include transaction costs. Back-tested performance is hypothetical (it does not reflect trading in actual accounts) and is provided for informational purposes to illustrate the effects of the discussed strategy during a specific period. Back-tested performance results have certain limitations. Such results do not represent the impact of material economic and market factors might have on an investment advisor’s decision making process if the advisor were actually managing client money. Back-testing performance also differs from actual performance because it is achieved through retroactive application of a model investment methodology designed with the benefit of hindsight. Dorsey, Wright & Associates believes the data used in the testing to be from credible, reliable sources, however; Dorsey, Wright & Associates, LLC (collectively with its affiliates and parent company, “DWA”) makes no representation or warranties of any kind as to the accuracy of such data. Past performance is not indicative of future results. Potential for profits is accompanied by possibility of loss.

[…] To read Part 2 click here […]