To read Part 1 click here

To read Part 2 click here

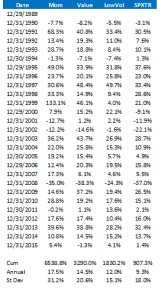

I am using three different factor strategies (Momentum, Low Volatility, and Value) to form a Core Equity strategy. A fourth factor, Size, will also be considered in the portfolio construction process (equal weighted instead of cap weighted).

All three of the factor strategies are constructed in a similar way. The universe is the top 1000 market cap stocks traded in the U.S. All of these stocks should have plenty of liquidity and should eliminate a lot of the issues that occur when you are dealing with small or micro-cap stocks. All three strategies are rebalanced at the end of each month and have 100 stocks. The strategies are run separately so in theory a stock could appear in all three strategies (I will account for this in the final model). In addition, all three strategies use a Point and Figure momentum overlay that was discussed in part 2. One of the goals was to make the three factor strategies as similar as possible in terms of portfolio construction to avoid as much optimization and curve fitting as possible. All three of the factor strategies use very simple metrics and I believe they should be robust going forward. There will certainly be times of underperformance (sometimes dramatic underperformance) from each of the strategies, but over time they have all shown to work very well.

The momentum strategy uses a simple, well-known momentum measure with a Point and Figure relative strength overlay. Each month stocks are ranked by their trailing 250 day performance skipping the most recent 20 days (or one month). This is a pretty standard definition for momentum. The Point and Figure overlay actually does help returns over time, but not anywhere near what it does for the Value and Low Volatility models. However, I wanted to include the Point and Figure overlay to keep the momentum model similar in portfolio construction to the other two. Momentum provides really good returns, but is really volatile. Momentum also has the distinction of being the least correlated with the other factors so they really help smooth out the volatility of a stand-alone momentum strategy.

The Value strategy uses a composite of four value ratios to rank the stocks in the universe: Price/Sales, Price/Book, Price/Free Cash Flow, and Price/Earnings. Again, we use a Point and Figure relative strength overlay to improve the returns and filter out some of the value traps. The universe is the same as the momentum model as are the rebalance dates and weightings.

The Low Volatility strategy uses the standard deviation of daily returns over the trailing year to rank stocks in the universe. The Point and Figure overlay is also used to keep everything consistent, and the other portfolio construction parameters remain the same.

All three models perform very well versus the broad market (S&P; 500 Total Return). They do have their bumps along the way in terms of when they outperform and underperform, but often one strategy’s underperformance is offset by outperformance in another.

The returns used within this article are the result of a back-test using indexes that are not available for direct investment. Returns do include dividends, but do not include transaction costs. Back-tested performance is hypothetical (it does not reflect trading in actual accounts) and is provided for informational purposes to illustrate the effects of the discussed strategy during a specific period. Back-tested performance results have certain limitations. Such results do not represent the impact of material economic and market factors might have on an investment advisor’s decision making process if the advisor were actually managing client money. Back-testing performance also differs from actual performance because it is achieved through retroactive application of a model investment methodology designed with the benefit of hindsight. Dorsey, Wright & Associates believes the data used in the testing to be from credible, reliable sources, however; Dorsey, Wright & Associates, LLC (collectively with its affiliates and parent company, “DWA”) makes no representation or warranties of any kind as to the accuracy of such data. Past performance is not indicative of future results. Potential for profits is accompanied by possibility of loss.