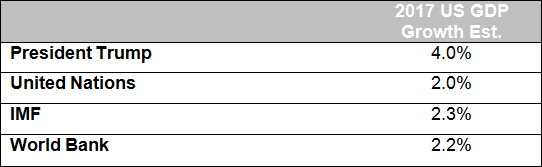

2016 was a lackluster year for GDP growth in the US, early estimates put 4th quarter estimates at 1.9% with a full year estimate at 1.6%. This is significantly lower than the 4% growth rate the president has targeted for 2017 and is much closer to estimates of an approximately 2.0-2.2% GDP growth rate in 2017 by several international groups.

Sources: www. knoema.com/qhswwkc/us-gdp-growth-forecast-2015-2019-and-up-to-2060-data-and-charts, www.whitehouse.gov/bringing-back-jobs-and-growth

That is not to say the major infrastructure spending that is being proposed, the possibility of corporate tax reform and repatriation of billions in overseas cash will not have an impact on short term growth rates. The questions are how long is it sustainable and what are the risks to the market if we see GDP slow?

For many investors, international markets have a more appealing long term growth story when faced with 2% growth. The IMF has a 1.9% growth projection for the Advanced Economies (Including the US) and a 4.5% growth projection for emerging and developing (frontier) markets. An accelerated growth rate and a large young population of people striving for a better life are several points investors continue champion when making allocations to emerging markets. Our D.A.L.I. model currently has international equities in the number two position behind US equities with the emerging markets, specifically Latin America showing stronger indicators than the majority developed regions.

The problem that many face when making international allocations is do they stick to the less volatile developed markets or do they dip their toe into riskier emerging and frontier market countries that have the potential for higher returns? It is our opinion that an either or philosophy will not be a winning strategy, if you bind yourself to only developed or emerging markets you are leaving returns on the table. Below is a relative strength chart of emerging markets (EEM) vs. developed markets (EFA) over that past 10 years. Each market experienced different period of strength. By widening your investment universe you can rotate markets as the trend shifts over time allowing for the opportunity of a better risk adjusted return.

The added portfolio diversification achieved by including emerging alongside developed markets is notable. When looking at asset correlations between 1/1/2009 to 12/31/2016 shifting from developed only (EFA) to global ex US (ACWX) which has a 16% allocation to emerging markets reduced correlation by almost 5% against US large cap equities (SPY) and US small cap equities (IWM) by 2.5%. Holding just emerging markets (EEM) for your international allocation is the best tool for diversification in this example, with only a 0.57 correlation to large and small cap equities. However this over exposes you to a high volatility asset that some investors would not be comfortable in for long periods of time.

Correlation of Asset Classes

In our SRS International strategy we have chosen to widen our investable universe to include the global ex US market. The wider universe allows for the ability to select from more securities that have higher technical attributes. Over the past 10 years we have used Relative Strength as a main factor to find the best performing securities agnostic to developed and emerging markets.

As shown above, nearly 70% of our Systematic RS International strategy is currently allocated to emerging markets. This however was not the case in 2012 when emerging markets only held 30% of the portfolio. Flexibility, especially when it comes to international equity exposure can make a big difference in investment returns if you are willing to expand your investable universe.

Nothing contained herein should be construed as an offer to sell or the solicitation of an offer to buy any security. This report does not attempt to examine all the facts and circumstances which may be relevant to any company, industry or security mentioned herein. We are not soliciting any action based on this document. It is for the general information of clients of Dorsey, Wright & Associates, LLC (“Dorsey, Wright & Associates”). This document does not constitute a personal recommendation or take into account the particular investment objectives, financial situations, or needs of individual clients. Before acting on any analysis, advice or recommendation in this document, clients should consider whether the security or strategy in question is suitable for their particular circumstances and, if necessary, seek professional advice. The relative strength strategy is NOT a guarantee. There may be times where all investments and strategies are unfavorable and depreciate in value. Relative Strength is a measure of price momentum based on historical price activity. Relative Strength is not predictive and there is no assurance that forecasts based on relative strength can be relied upon. Past performance is no guarantee of future returns.