The main thing that should matter to a long-term investor is real return. Real return is return after inflation is factored in. When your real return is positive, you are actually increasing your purchasing power— and purchasing goods and services is the point of having a medium of exchange (money) in the first place.

A recent article in The New York Times serves as a useful reminder about real return.

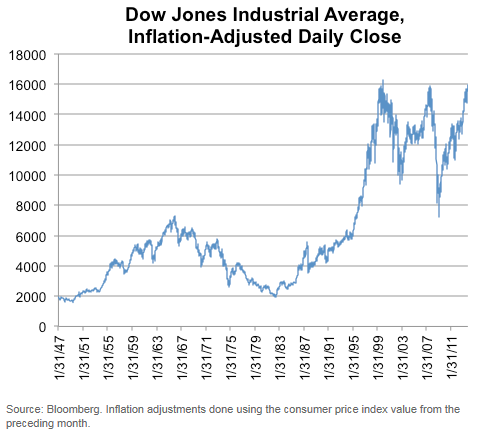

The Dow Jones industrial average broke through 16,000 on Monday for the first time on record — well, at least in nominal terms. If you adjust for inflation, technically the highest level was on Jan. 14, 2000.

Adjusting for price changes, the Dow’s high today was still about 1.3 percent below its close on Jan. 14, 2000 (and about 1.6 percent below its intraday high from that date).

There’s a handy graphic as well, of the Dow Jones Industrial Average adjusted for inflation.

Source: New York Times/Bloomberg

(click on image to enlarge)

This chart, I think, is a good reminder that buy-and-hold (known in our office as “sit-and-take-it”) is not always a good idea. In most market environments there are asset classes that are providing real return, but that asset class is not always the broad stock market. There is value in tactical asset allocation, market segmentation, strategy diversification, and other ways to expose yourself to assets that are appreciating fast enough to augment your purchasing power.

I’ve read a number of pieces recently that contend that “risk-adjusted” returns are the most important investment outcome. Really? This would be awesome if I could buy a risk-adjusted basket of groceries at my local supermarket, but strangely, they seem to prefer the actual dollars. Your client could have wonderful risk-adjusted returns rolling Treasury bills, but would then also get to have a lovely risk-adjusted retirement in a mud hut. If those dollars are growing more slowly than inflation, you’re just moving in reverse.

Real returns are where it’s at.