February 27, 2014

Morgan Housel at Motley Fool has a wonderful article on how investors can learn from failure. He sets the tone with a few different quotes and anecdotes that point out that a lot of being a success is just avoiding really dumb mistakes.

At a conference years ago, a young teen asked Charlie Munger how to succeed in life. “Don’t do cocaine, don’t race trains to the track, and avoid all AIDS situations,” Munger said. Which is to say: Success is less about making great decisions and more about avoiding really bad ones.

People focus on role models; it is more effective to find antimodels—people you don’t want to resemble when you grow up. Nassim Taleb

I’ve added the emphasis, but Mr. Housel makes a good point. Learning from failure is equally important as learning from success. In fact, he argues it may be more important.

If it were up to me, I would replace every book called How to Invest Like Warren Buffett with a one called How to Not Invest Like Lehman Brothers, Long-Term Capital Management, and Jesse Livermore. There are so many lessons to learn from these failed investors about situations most of us will face, like how quickly debt can ruin you. I’m a fan of learning from Buffett, but the truth is most of us can’t devote as much time to investing as he can. The biggest risk you face as an investor isn’t that you’ll fail to be Warren Buffett; it’s that you’ll end up as Lehman Brothers.

But there’s no rule that says you have to learn by failing yourself. It is far better to learn vicariously from other people’s mistakes than suffer through them on your own.

That’s his thesis in a nutshell. He offers three tidbits from his study of investing failures. I’ve quoted him in full here because I think his context is important (and the writing is really good).

1. The overwhelming majority of financial problems are caused by debt, impatience, and insecurity. People want to fit in and impress other people, and they want it right now. So they borrow money to live a lifestyle they can’t afford. Then they hit the inevitable speed bump, and they find themselves over their heads and out of control. That simple story sums up most financial problems in the world. Stop trying to impress people who don’t care about you anyways, spend less than you earn, and invest the rest for the long run. You’ll beat 99% of people financially.

2. Complexity kills. You can make a lot of money in finance, so the industry attracted some really brilliant people. Those brilliant people naturally tried to make finance more like their native fields of physics, math, and engineering, so finance has grown exponentially more complex in the last two decades. For most, that’s been a disservice. I think the evidence is overwhelming that simple investments like index funds and common stocks will demolish complicated ones like derivatives and leveraged ETFs. There are two big stories in the news this morning: One is about how the University of California system is losing more than $100 million on a complicated interest rate swap trade. The other is about how Warren Buffett quintupled his money buying a farm in Nebraska. Simple investments usually win.

3. So does panic. In his book Deep Survival, Laurence Gonzalez chronicles how some people managed to survive plane crashes, getting stranded on boats, and being stuck in blizzards while their peers perished. The common denominator is simple: The survivors didn’t panic. It’s the same in investing. I’ve seen people make a lifetime of good financial decisions only to blow it all during a market panic like we saw in 2008. Any financial decision you make with an elevated heart rate is probably going to be one you’ll regret. Napoleon’s definition of a military genius was “the man who can do the average thing when all those around him are going crazy.” It’s the same in investing.

I think these are really good points. It’s true that uncontrolled leverage accompanies most real blowups. Having patience in the investing process is indeed necessary; we’ve written about that a lot here too. The panic, impatience, and insecurity he references are really all behavioral issues—and it just points out that having your head on straight is incredibly important to investment success. How successful you are in your profession or how much higher math you know is immaterial. As Adam Smith (George Goodman) wrote, “If you don’t know who you are, the stock market is an expensive place to find out.”

Mr. Housel’s point on complexity could be a book in itself. Successful investing just entails owning productive assets—the equity and debt of successful enterprises—acquired at a reasonable price. Whether you own the equity directly, like Warren Buffett and his farm, or in security form is immaterial. An enterprise can be a company—or even a country—but it’s got to be successful.

Complexity doesn’t help with this evaluation. In fact, complexity often obscures the whole point of the exercise.

This is actually one place where I think relative strength can be very helpful in the investment process. Relative strength is incredibly simple and relative strength is a pretty good signaling mechanism for what is successful. Importantly, it’s also adaptive: when something is no longer successful, relative strength can signal that too. Sears was once the king of retailing. Upstart princes like K-Mart in its day, and Wal-Mart and Costco later, put an end to its dominance. Once, homes were lit with candles and heated with fuel oil. Now, electricity is much more common—but tomorrow it may be something different. No asset is forever, not even Warren Buffett’s farmland. When the soil is depleted, that farm will become a lead anchor too. Systematic application of relative strength, whether it’s being used within an asset class or across asset classes, can be a very useful tool to assess long-term success of an enterprise.

Most investing problems boil down to behavioral issues. Impatience and panic are a couple of the most costly. Avoiding complexity is a different dimension that Mr. Housel brings up, and one that I think should be included in the discussion. There are plenty of millionaires that have been created through owning businesses, securities, or real estate. I can’t think of many interest rate swap millionaires (unless you count the people selling them). Staying calm and keeping things simple might be the way to go. And if the positive prescription doesn’t do it for you, the best way to be a good investor may be to avoid being a terrible investor!

8 Comments |

8 Comments |  From the MM, Investor Behavior, Markets, Thought Process | Tagged: behavioral finance, decision-making, investor behavior, relative strength, stock market, systematic investment process, warren buffett |

From the MM, Investor Behavior, Markets, Thought Process | Tagged: behavioral finance, decision-making, investor behavior, relative strength, stock market, systematic investment process, warren buffett |  Permalink

Permalink

Posted by:

Mike Moody

February 3, 2014

Almost all of the performance from a relative strength or momentum model comes from the upper end of the ranks. We run different models all the time to test different theories or to see how existing decision rules work on different groups of securities. Sometimes we are surprised by the results, sometimes we aren’t. But the more we run these tests, the more some clear patterns emerge.

One of these patterns we see constantly is all of the outperformance in a strategy coming from the very top of the ranks. People are often surprised at how quickly any performance advantage disappears as you move down the ranking scale. That is one of the things that makes implementing a relative strength strategy so difficult. You have to be absolutely relentless in pushing the portfolio toward the strength because there is often zero outperformance in aggregate from the stuff that isn’t at the top of the ranks. If you are the type of person that would rather “wait for a bounce” or “wait until I’m back to breakeven,” then you might as well just equal-weight the universe and call it a day.

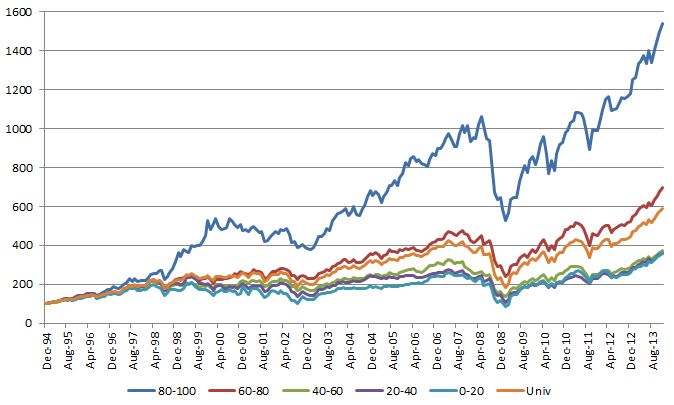

Below is a chart from a sector rotation model I was looking at earlier this week. This model uses the S&P; 500 GICS sub-sectors and the ranks were done using a point & figure matrix (ie, running each sub-sector against every other sub-sector) and the portfolio was rebalanced monthly. You can see the top quintile (ranks 80-100) performs quite well. After that, good luck. The “Univ” line is a monthly equal-weighted portfolio of all the GICS sub-sectors. The next quintile (ranks 60-80) barely beats the universe return and probably adds no value after you are done with trading costs, taxes, etc… Keep in mind that these sectors are still well within the top half of the ranks and they still add minimal value. The other three quintiles are underperformers. They are all clustered together well below the universe return.

(Click on image to enlarge)

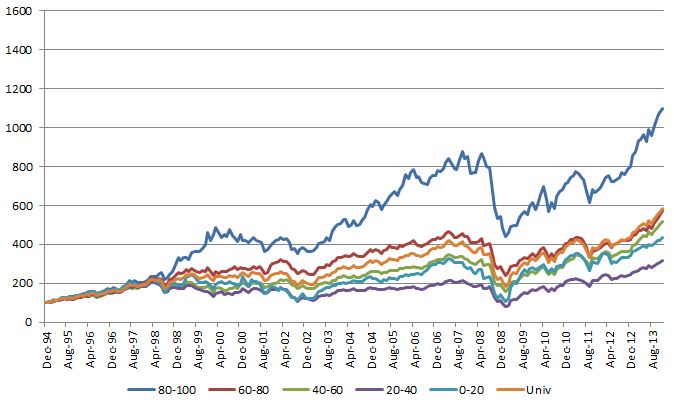

The overall performance numbers aren’t as good, but you get the exact same pattern of results if you use a 12-Month Trailing Return to rank the sub-sectors instead of a point & figure matrix:

(click on image to enlarge)

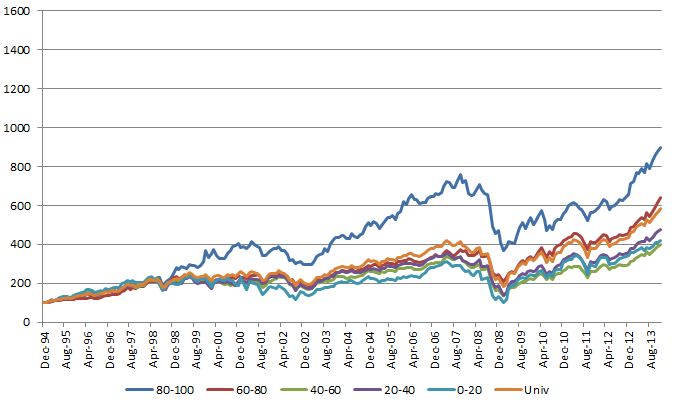

Same deal if you use a 6-Month Trailing Return:

(click on image to enlarge)

This is a constant theme we see. The very best sectors, stocks, markets, and so on drive almost all of the outperformance. If you miss a few of the best ones it is very difficult to outperform. If you are unwilling to constantly cut the losers and buy the winners because of some emotional hangup, it is extremely difficult to outperform. The basket of securities in a momentum strategy that delivers the outperformance is often smaller than you think, so it is crucial to keep the portfolio focused on the top-ranked securities.

13 Comments | Markets, Portfolio Theory, Relative Strength Research, Thought Process | Tagged: relative strength, systematic investment process | Permalink

Posted by:

John Lewis

January 27, 2014

Our Systematic Relative Strength portfolios are available as managed accounts at a large and growing number of firms.

- Wells Fargo Advisors (Global Macro available on the Masters/DMA Platforms)

- Morgan Stanley (IMS Platform)

- TD Ameritrade Institutional

- UBS Financial Services (Aggressive and Core are available on the MAC Platform)

- RBC Wealth Management (MAP Platform)

- Raymond James (Outside Manager Platform)

- Stifel Nicolaus

- Kovack Securities

- Deutsche Bank

- Charles Schwab Institutional

- Sterne Agee

- Scott & Stringfellow

- Envestnet

- Placemark

- Scottrade Institutional

- Janney Montgomery Scott

- Robert W. Baird

- Wedbush Morgan

- Prospera

- Oppenheimer (Star Platform)

- SunTrust

- Lockwood

Different Portfolios for Different Objectives: Descriptions of our seven managed accounts strategies are shown below. All managed accounts use relative strength as the primary investment selection factor.

Aggressive: This Mid and Large Cap U.S. equity strategy seeks to achieve long-term capital appreciation. It invests in securities that demonstrate powerful relative strength characteristics and requires that the securities maintain strong relative strength in order to remain in the portfolio.

Core: This Mid and Large Cap U.S. equity strategy seeks to achieve long-term capital appreciation. This portfolio invests in securities that demonstrate powerful relative strength characteristics and requires that the securities maintain strong relative strength in order to remain in the portfolio. This strategy tends to have lower turnover and higher tax efficiency than our Aggressive strategy.

Growth: This Mid and Large Cap U.S. equity strategy seeks to achieve long-term capital appreciation with some degree of risk mitigation. This portfolio invests in securities that demonstrate powerful relative strength characteristics and requires that the securities maintain strong relative strength in order to remain in the portfolio. This portfolio also has an equity exposure overlay that, when activated, allows the account to hold up to 50% cash if necessary.

International: This All-Cap International equity strategy seeks to achieve long-term capital appreciation through a portfolio of international companies in both developed and emerging markets. This portfolio invests in those securities with powerful relative strength characteristics and requires that the securities maintain strong relative strength in order to remain in the portfolio. Exposure to international markets is achieved through American Depository Receipts (ADRs).

Global Macro: This global tactical asset allocation strategy seeks to achieve meaningful risk diversification and investment returns. The strategy invests across multiple asset classes: Domestic Equities (long & inverse), International Equities (long & inverse), Fixed Income, Real Estate, Currencies, and Commodities. Exposure to each of these areas is achieved through exchange-traded funds (ETFs).

Balanced: This strategy includes equities from our Core strategy (see above) and high-quality U.S. fixed income in approximately a 60% equity / 40% fixed income mix. This strategy seeks to provide long-term capital appreciation and income with moderate volatility.

Tactical Fixed Income: This strategy seeks to provide current income and strong risk-adjusted fixed income returns. The strategy invests across multiple sectors of the fixed income market: U.S. government bonds, investment grade corporate bonds, high yield bonds, Treasury inflation protected securities (TIPS), convertible bonds, and international bonds. Exposure to each of these areas is achieved through exchange-traded funds (ETFs).

To receive fact sheets for any of the strategies above, please e-mail Andy Hyer at [email protected] or call 626-535-0630. Past performance is no guarantee of future returns. An investor should carefully review our brochure and consult with their financial advisor before making any investments.

7 Comments | Markets | Tagged: investment, managed accounts, market, portfolio, relative strength, stock market, Tactical Asset Allocation | Permalink

Posted by:

Andy Hyer

January 16, 2014

As sector ETFs have proliferated, more and more investors have been attracted to sector rotation and tactical asset allocation strategies using ETFs, whether self-managed or implemented by an advisor. Mark Hulbert commented on sector rotation strategies in a recent article on Marketwatch that highlighted newsletters using Fidelity sector funds. All of the newsletters had good returns, but there was one surprising twist:

…you might think that these advisers each recommended more or less the same basket of funds. But you would be wrong. In fact, more often than not, each of these advisers has tended to recommend funds that are not recommended by any other of the top five sector strategies.

That’s amazing, since there are only 44 actively managed Fidelity sector funds and these advisers’ model portfolios hold an average of between five and 10 funds each.

This suggests that there is more than one way of playing the sector rotation game, which is good news. If there were only one profitable sector strategy, it would quickly become so overused as to stop working.

This is even true among those advisers who recommend sectors based on their relative strength or momentum. Because there are so many ways of defining these characteristics, two different sector momentum strategies will often end up recommending two different Fidelity sector funds.

Another way of appreciating the divergent recommendations of these top performing advisers is this: Of the 44 actively managed sector funds that Fidelity currently offers, no fewer than 22 are recommended by at least one of these top five advisers. That’s one of every two, on average, which hardly seems very selective on the advisers’ part.

Amazing, isn’t it? It just shows that there are many ways to skin a cat.

Even with a very limited menu of Fidelity sector funds, there was surprisingly little overlap. Imagine how little overlap there would be within the ETF universe, which is much, much larger! In short, you can safely pursue a sector rotation strategy (and, by extension, tactical asset allocation) with little concern that everyone else will be plowing into the same ETFs.

3 Comments | From the MM, Markets, Momentum, Tactical Asset Alloc, Thought Process | Tagged: momentum, relative strength, sector rotation, Tactical Asset Allocation | Permalink

Posted by:

Mike Moody

January 9, 2014

Leuthold’s January Green Book includes a simple, yet compelling study about applying momentum at the asset class level:

While even academics now acknowledge the existence of a “price persistence” effect at the stock and industry group level, it is less well known that the phenomenon exists at the broad asset class level. We’ve examined a few simple approaches in which allocation decisions are based purely on the prior year’s total return performance of seven asset classes: Large Caps, Small Caps, Foreign Stocks, REITs, Commodities, Gold and U.S. Treasury Bonds. Contrarians might be surprised to learn that a turnaround strategy of buying last year’s laggards (the #5, #6 and #7 performers), has been a consistently poor approach for the last 40 years. Meanwhile, a naive, momentum-surfing strategy of buying last year’s #1 or #2 performer (or both) has soundly beaten the S&P; 500 since 1973. (We suspect these results are especially humbling to those who spend the rest of the year building and monitoring elaborate tools that track valuations, the economic cycle, investor sentiment, etc.)

(printed with permission from Leuthold)

Bottom line: momentum also works well at the asset class level. Click here for a white paper written by John Lewis that also confirms that momentum can be successfully applied to a group of asset classes.

12 Comments | Tactical Asset Alloc | Tagged: momentum, relative strength, Tactical Asset Allocation | Permalink

Posted by:

Andy Hyer

January 6, 2014

The Dorsey, Wright Technical Leaders Index is composed of a basket of 100 mid and large cap securities that have strong relative strength (momentum) characteristics. Each quarter we reconstitute the index by selling stocks that have underperformed and by adding new securities that score better in our ranking system. We began calculating the index in real-time at the end of 2006. Over the last seven years there have been quite a few deletions and additions as the index has adapted to some very dynamic market conditions.

Any relative strength or momentum-based investment strategy is a trend following strategy. Trend following has worked for many years in financial markets (although not every year). These systems are characterized by a several common attributes: 1) Losing trades are cut quickly and winners are allowed to run, 2) there are generally a lot of small losing trades, and 3) all of the money is made by the large outliers on the upside. When we look at the underlying trades inside of the index over the years we find exactly that pattern of results. There is a lot going on behind the scenes at each rebalance that is designed to eliminate losing positions quickly and maintain large allocations to the true winners that drive the returns.

We pulled constituent level data for the DWATL Index going back to the 12/31/2006 rebalance. For each security we calculated the return relative to the S&P; 500 and how many consecutive quarters it was held in the index. (Note: stocks can be added, removed, and re-added to the index so any individual stock might have several entries in our data.) The table below shows summary statistics for all the trades inside of the index over the last seven years:

The data shows our underlying strategy is doing exactly what a trend following system is designed to accomplish. Stocks that aren’t held very long (1 to 2 quarters), on average, are underperforming trades. But when we are able to find a security that can be held for several quarters, those trades are outperformers on average. The whole goal of a relative strength process is to ruthlessly cut out losing positions and to replace them with positions that have better ranks. Any investor makes tons of mistakes, but the system we use to reconstitute the DWATL Index is very good at identifying our mistakes and taking care of them. At the same time, the process is also good at identifying winning positions and allowing them to remain in the index.

Here is the same data from the table shown graphically:

You can easily see the upward tilt to the data showing how relative performance on a trade-level basis improves with the time held in the index. For the last seven years, each additional consecutive quarter we have been able to keep a security in the Index has led to an average relative performance improvement of about 920 basis points. That should give you a pretty good idea about what drives the returns: the big multi-year winners.

We often speak to the overall performance of the Index, but we sometimes forget what is going on behind the scenes to generate that return. The process that is used to constitute the index has all of the characteristics of a trend following system. Underperforming positions are quickly removed and the big winning trades are allowed to remain in the index as long as they continue to outperform. It’s a lot like fishing: you just keep throwing the small ones back until you catch a large one. Sometimes it takes a couple of tries to get a keeper, but if you got a big fish on the first try all the time it would be called “catching” not “fishing.” I believe part of what has made this index so successful over the years is there is zero human bias that enters the reconstitution process. When a security needs to go, it goes. If it starts to perform well again, it comes back. It has no good or bad memories. There are just numbers.

The performance numbers are pure price return, not inclusive of fees, dividends, or other expenses. Past performance is no guarantee of future returns. Potential for profit is accompanied by potential for loss. A list of all holdings for the trailing 12 months is available upon request.

46 Comments | Momentum, Portfolio Theory, Relative Strength Research, Thought Process | Tagged: momentum, relative strength, trend following | Permalink

Posted by:

John Lewis

November 26, 2013

…talk about the best advice they have even gotten in a short piece from Fortune. I think it clarifies the difference between a blind value investor and an investor who is looking for good companies (not coincidentally, many of those good companies have good relative strength). Warren Buffett and Charlie Munger have made a fortune implementing this advice.

Buffett: I had been oriented toward cheap securities. Charlie said that was the wrong way to look at it. I had learned it from Ben Graham, a hero of mine. [Charlie] said that the way to make really big money over time is to invest in a good business and stick to it and then maybe add more good businesses to it. That was a big, big, big change for me. I didn’t make it immediately and would lapse back. But it had a huge effect on my results. He was dead right.

Munger: I have a habit in life. I observe what works and what doesn’t and why.

I highlighted the fun parts. Buffett started out as a Ben Graham value investor. Then Charlie wised him up.

Valuation has its place, obviously. All things being equal, it’s better to buy cheaply than to pay up. But Charlie Munger had observed that good businesses tended to keep on going. The same thing is typically true of strong stocks—and most often those are the stocks of strong businesses.

Buy strong businesses and stick with them as long as they remain strong.

Source: CNN/Money (click on image to enlarge)

1 Comment | From the MM, Investor Behavior, Markets, Thought Process | Tagged: Charlie Munger, decision-making, portfolio theory, relative strength, stock market, strategy, warren buffett | Permalink

Posted by:

Mike Moody

October 18, 2013

We use a systematic process for investment because we think that’s the best way to go. Our systematic process also happens to be adaptive because we think adaptation to the current market environment is also an important consideration. (If you don’t adapt you die.) Our decision to use a systematic process is grounded in evidence that, over time, systematic processes tend to win out over inconsistent human decision making. (See here, for example.)

The latest instance of this was an interesting article on Quartz about the coming wave of full-service coffee machines that may have the potential to replace baristas. Consider, for example, what this particular quotation says about the power of a systematic process:

In 2012, Julian Baggini, a British philosophy writer and coffee aficionado, wondered why dozens of Europe’s Michelin-starred restaurants were serving guests coffee that came out of vacuum-sealed plastic capsules manufactured by Nespresso. So he conducted a taste test on a small group of experts. A barista using the best, freshly-roasted beans went head to head with a Nespresso capsule coffee brewing machine. It’s the tale of John Henry all over again, only now it was a question of skill and grace rather than brute strength.

As the chefs at countless restaurants could have predicted, the Nespresso beat the barista.

Suffice it to say that most manufacturing nowadays is done by machine because it is usually faster, less expensive, and more accurate than a human. Perhaps you will miss terribly your nose-ringed, pink-haired, tatooed barista, but then again, maybe not so much.

Systematic investing has its problems—sometimes the adaptation seems too slow or too fast. Sometimes your process is just out of favor. But like a manufacturing process, a systematic investment process holds the promise of consistency and potential improvement as technology and new techniques are incorporated over time. While it may seem less romantic than the lone stock picker, systematic investment could well be the wave of the future.

HT to Abnormal Returns

1 Comment | Just for Fun, Thought Process | Tagged: decision-making, relative strength, systematic investment process | Permalink

Posted by:

Mike Moody

October 14, 2013

In a low-interest rate environment, investors have naturally turned their attention to stocks paying high dividends as a way to generate income. Momentum, as a return factor, has not been in the spotlight. However, as interest rates have moved higher from their lows of last summer (On October 10, 2013 the 10-year US Treasury yield was 2.71% compared to 1.43% on July 25, 2012.), you might wonder how high dividend paying stocks tend to perform in rising rate environments over time. A current trend chart of the 10-year U.S. Treasury Yield Index, shows that yields are trending higher.

Source: Dorsey Wright

A longer-term chart of the 10-year US Treasury Yield Index is shown below:

Jim O’Shaughnessy’s What Works On Wall Street says this about high-yielders:

The high-yielders from Large Stocks do best in market environments in which value is outperforming growth, winning 74 percent of the time. They also do well in markets in which bonds are outperforming stocks, winning 65 percent of the time in those environments.

O’Shaughnessy’s book lays out the performance of portfolios formed by a number of return factors since the 1920s. His book includes the performance of portfolios formed by market capitalization, price-to-earnings ratios, EBITDA, price-to-cash flow ratios, price-to-sales ratios, price-to book ratios, dividend yields, relative strength (momentum), and many other factors.

In the rising interest rate environment of the 1960s and 1970s, O’Shaughessy shows the performance for the portfolio of the highest yielders as follows:

Source: What Works On Wall Street

Not bad—the dividend-focused portfolio was still able to generate modest outperformance. However, a portfolio formed by price momentum was clearly able to generate much higher returns in a rising rate environment. While this may not be the best environment for portfolios of high dividend payers to really stand out, investors may find that momentum can excel in rising-rate periods.

Past performance is no guarantee of future returns.

14 Comments | Markets, Relative Strength Research | Tagged: momentum, relative strength | Permalink

Posted by:

Andy Hyer

October 7, 2013

John Rekenthaler at Morningstar, who usually has some pretty smart stuff to say, took on the topic of smart beta in a recent article. Specifically, he examined a variety of smart beta factors with an eye to determining which ones were real and might persist. He also thought some factors might be fool’s gold.

Here’s what he had to say about value:

The value premium has long been known and continues to persist.

And here’s what he had to say about relative strength (momentum):

I have trouble seeing how momentum can succeed now that its existence is well documented.

The italics are mine. I didn’t take logic in college, but it seems disingenuous to argue that one factor will continue to work after it is well-known, while becoming well-known will cause the other factor to fail! (If you are biased in favor of value, just say so, but don’t use the same argument to reach two opposite conclusions.)

There are a variety of explanations about why momentum works, but just because academics can’t agree on which one is correct doesn’t mean it won’t continue to work. It is certainly possible that any anomaly could be arbitraged away, but Robert Levy’s relative strength work has been known since the 1960s and our 2005 paper in Technical Analysis of Stocks & Commodities showed it continued to work just fine just the way he published it. Academics under the spell of efficient markets trashed his work at the time too, but 40 years of subsequent returns shows the professors got it wrong.

However, I do have a background in psychology and I can hazard a guess as to why both the value and momentum factors will continue to persist—they are both uncomfortable to implement. It is very uncomfortable to buy deep value. There is a terrific fear that you are buying a value trap and that the impairment that created the value will continue or get worse. It also goes against human nature to buy momentum stocks after they have already outperformed significantly. There is a great fear that the stock will top and collapse right after you add it to your portfolio. Investors and clients are quite resistant to buying stocks after they have already doubled, for example, because there is a possibility of looking really dumb.

Here’s the reason I think both factors are psychological in origin: it is absurdly easy to screen for either value or momentum. Any idiot can implement either strategy with any free screener on the web. Pick your value metric or your momentum lookback period and away you go. In fact, this is pretty much exactly what James O’Shaughnessy did in What Works on Wall Street. Both factors worked well—and continue to work despite plenty of publicity. So the barrier is not that there is some secret formula, it’s just that investors are unwilling to implement either strategy in a systematic way–because of the psychological discomfort.

If I were to make an argument—the behavioral finance version—about which smart beta factor could potentially be arbitraged away over time, I would have to guess low volatility. If you ask clients whether they would prefer to buy stocks that a) had already dropped 50%, b) had already gone up 50%, or c) had low volatility, I think most of them would go with “c!” (Although I think it’s also possible that aversion to leverage will keep this factor going.)

Value and momentum also happen to work very well together. Value is a mean reversion factor, while momentum is a trend continuation factor. As AQR has shown, the excess returns of these two factors (unsurprisingly, once you understand how they are philosophical opposites) are uncorrelated. Combining them may have the potential to smooth out an equity return stream a little bit. Regardless, two good return factors are better than one!

8 Comments | Investor Behavior, Portfolio Theory, Relative Strength and Value, Thought Process | Tagged: behavioral finance, investor behavior, momentum, portfolio theory, relative strength, systematic investment process, trend following, value | Permalink

Posted by:

Mike Moody

October 4, 2013

Gary Antonacci has a very nice article at Optimal Momentum regarding long-only momentum. Most academic studies look at long-short momentum, while most practitioners (like us) use long-only momentum (also known as relative strength). Partly this is because it is somewhat impractical to short across hundreds of managed accounts, and partly because clients don’t usually want to have short positions. The article has another good reason, quoting from an Israel & Moskowitz paper:

Using data over the last 86 years in the U.S. stock market (from 1926 to 2011) and over the last four decades in international stockmarkets and other asset classes (from 1972 to 2011), we find that the importance of shorting is inconsequential for all strategies when looking at raw returns. For an investor who cares only about raw returns, the return premia to size, value, and momentum are dominated by the contribution from long positions.

In other words, most of your return comes from the long positions anyway.

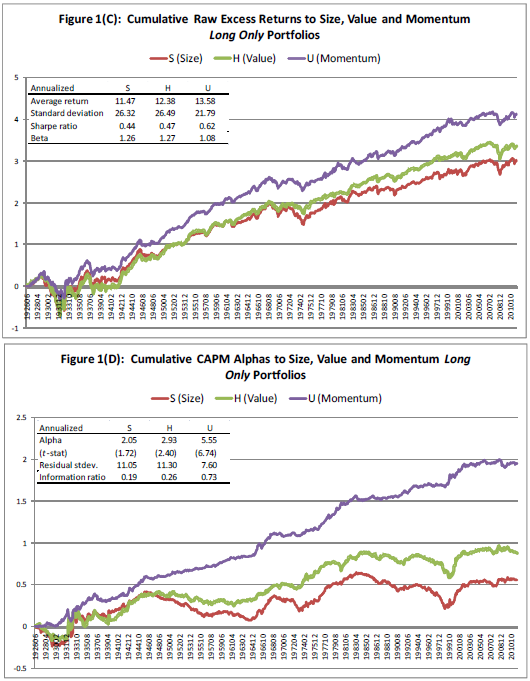

The Israel & Moskowitz paper looks at raw long-only returns from capitalization, value, and momentum. Perhaps even more importantly, at least for the Modern Portfolio Theory crowd, it looks at CAPM alphas from these same segments on a long-only basis. The CAPM alpha, in theory, is the amount of excess return available after adjusting for each factor. Here’s the chart:

Source: Optimal Momentum

(click on image to enlarge)

From the Antonacci article, here’s what you are looking at and the results:

I&M; charts and tables show the top 30% of long-only momentum US stocks from 1927 through 2011 based on the past 12-month return skipping the most recent month. They also show the top 30% of value stocks using the standard book-to-market equity ratio, BE/ME, and the smallest 30% of US stocks based on market capitalization.

Long-only momentum produces an annual information ratio almost three times larger than value or size. Long-only versions of size, value, and momentum produce positive alphas, but those of size and value are statistically weak and only exist in the second half of the data. Momentum delivers significant abnormal performance relative to the market and does so consistently across all the data.

Looking at market alphas across decile spreads in the table above, there are no significant abnormal returns for size or value decile spreads over the entire 1926 to 2011 time period. Alphas for momentum decile portfolio spread returns, on the other hand, are statistically and economically large.

Mind-boggling right? On a long-only basis, momentum smokes both value and capitalization!

Israel & Moskowitz’s article is also quoted in the post, and here is what they say about their results:

Looking at these finer time slices, there is no significant size premium in any sub period after adjusting for the market. The value premium is positive in every sub period but is only statistically significant at the 5% level in one of the four 20-year periods, from 1970 to 1989. The momentum premium, however, is positive and statistically significant in every sub period, producing reliable alphas that range from 8.9 to 10.3% per year over the four sub periods.

Looking across different sized firms, we find that the momentum premium is present and stable across all size groups—there is little evidence that momentum is substantially stronger among small cap stocks over the entire 86-year U.S. sample period. The value premium, on the other hand, is largely concentrated only among small stocks and is insignificant among the largest two quintiles of stocks (largest 40% of NYSE stocks). Our smallest size groupings of stocks contain mostly micro-cap stocks that may be difficult to trade and implement in a real-world portfolio. The smallest two groupings of stocks contain firms that are much smaller than firms in the Russell 2000 universe.

What is this saying? Well, the value premium doesn’t appear to exist in the biggest NYSE stocks (the stuff your firm’s research covers). You can find value in micro-caps, but the effect is still not very significant relative to momentum in long-only portfolios. And momentum works across all cap levels, not just in the small cap area.

All of this is quite important if you are running long-only portfolios for clients, which is what most of the industry does. Relative strength (momentum) is a practical tool because it appears to generate excess return over many time periods and across all capitalizations.

101 Comments | From the MM, Relative Strength Research, Thought Process | Tagged: long-only momentum, momentum, relative strength | Permalink

Posted by:

Mike Moody

September 19, 2013

No, this is not a post on personality disorders.

Rather, it is a post on the inherently unstable nature of correlations between securities and between asset classes. This is important because the success of many of the approaches to portfolio management make the erroneous assumption that correlations are fairly stable over time. I was reminded just how false this belief is while reading The Leuthold Group‘s April Green Book in which they highlighted the rolling 10-year correlations in monthly percentage changes between the S&P; 500 and the 10-year bond yield. Does this look stable to you? Chart is shown by permission from The Leuthold Group.

(Click to Enlarge)

If you are trying to use this data, would you conclude that higher bond yields are good for the stock market or bad? The answer is that the correlations are all over the map. In 2006, William J. Coaker II published The Volatility of Correlations in the FPA Journal. That paper details the changes in correlations between 15 different asset classes and the S&P; 500 over a 34-year time horizon. To give you a flavor for his conclusions, he pointed out that Real Estate’s rolling 5-year correlations to the S&P; 500 ranged from 0.17 to 0.75, and for Natural Resources the range was -0.34 to 0.49. History is conclusive – correlations are unstable.

This becomes a big problem for strategic asset allocation models that use historical data to calculate an average correlation between securities or asset classes over time. Those models use that stationary correlation as one of the key inputs into determining how the model should currently be allocated. That may well be of no help to you over the next five to ten years. Unstable correlations are also a major problem for “financial engineers” who use their impressive physics and computer programming abilities to identify historical relationships between securities. They may find patterns in the historical data that lead them to seek to exploit those same patterns in the future (i.e. LTCM in the 1990′s.) The problem is that the future is under no obligation to behave like the past.

Many of the quants are smart enough to recognize that unstable correlations are a major problem. The solution, which I have heard from several well-known quants, is to constantly be willing to reexamine your assumptions and to change the model on an ongoing basis. That logic may sound intelligent, but the reality is that many, if not most, of these quants will end up chasing their tail. Ultimately, they end up in the forecasting game. These quants are rightly worried about when their current model is going to blow up.

Relative strength relies on a different premise. The only historical pattern that must hold true for relative strength to be effective in the future is for long-term trends to exist. That is it. Real estate (insert any other asset class) and commodities (insert any other asset class) can be positively or negatively correlated in the future and relative strength models can do just fine either way. Relative strength models make zero assumptions about what the future should look like. Again, the only assumption that we make is that there will be longer-term trends in the future to capitalize on. Relative strength keeps the portfolio fresh with those securities that have been strong relative performers. It makes no assumptions about the length of time that a given security will remain in the portfolio. Sure, there will be choppy periods here and there where relative strength models do poorly, but there is no need (and it is counterproductive) to constantly tweak the model.

Ultimately, the difference between an adaptive relative strength model and most quant models is as different as a mule is from a horse. Both have four legs, but they are very different animals. One has a high probability of being an excellent performer in the future, while the other’s performance is a big unknown.

—-this article originally appeared 4/16/2010. It’s important to understand the difference between a model that relies on historical correlations and a model that just adapts to current trends.

48 Comments | From the Archives, Portfolio Theory, Thought Process | Tagged: correlation, portfolio theory, relative strength | Permalink

Posted by:

Mike Moody

September 6, 2013

Marshall Jaffe wrote an excellent article on investment process versus investment performance in the most recent edition of ThinkAdvisor. I think it is notable for a couple of reasons. First, it’s pithy and well-written. But more importantly, he’s very blunt about the problems of focusing only on investment performance for both clients and the industry. And make no mistake—that’s how the investment industry works in real life, even though it is a demonstrably poor way to do things. Consider this excerpt:

We see the disclaimer way too often. “Past performance is no guarantee of future results.” It is massively over-used—plastered on countless investment reports, statements and research. It’s not simply meaningless; it’s as if it’s not even there. And that creates a huge problem, because the message itself is really true: Past performance has no predictive value.

Since we are looking for something that does have predictive value—all the research, experience and hard facts say: Look elsewhere.

This is not a controversial finding. There are no fringe groups of investors or scholars penning op-ed pieces in the Wall Street Journal shooting holes in the logic of this reality. Each year there is more data, and each year that data reconfirms that past performance is completely unreliable as an investment tool. Given all that, you would think it would be next to impossible to find any serious investors still using past performance as a guideline. Indeed, that would be a logical conclusion.

But logical conclusions are often wrong when it comes to understanding human behavior. Not only does past performance remain an important issue in the minds of investors, for the vast majority it is the primary issue. In a study I referred to in my August column, 80% of the hiring decisions of large and sophisticated institutional pension plans were the direct result of outstanding past performance, especially recent performance.

The truth hurts! The bulk of the article discusses why investors focus on performance to their detriment and gives lots of examples of top performers that focus only on process. There is a reason that top performers focus on process—because results are the byproduct of the process, not an end in themselves.

The reason Nick Saban, our best athletes, leading scientists, creative educators, and successful investors focus on process is because it anchors them in reality and helps them make sensible choices—especially in challenging times. Without that anchor any investor observing the investment world today would be intimidated by its complexity, uncomfortable with its volatility and (after the meltdown in 2008) visibly fearful of its fragility. Of course we all want good returns—but those who use a healthy process realize that performance is not a goal; performance is a result.

Near the end of the article, I think Mr. Jaffe strikes right to the core of the investment problem for both individual investors and institutions. He frames the right question. Without the right question, you’re never going to get the right answer!

In an obsessive but fruitless drive for performance too many fund managers compromise the single most important weapon in their arsenal: their investment process.

Now we can see the flaw in the argument that an investor’s basic choice is active or passive. An investor indeed has two choices: whether to be goal oriented or process oriented. In reframing the investment challenge that way, the answer is self-evident and the only decision is whether to favor a mechanical process or a human one.

Reframing the question as “What is your investment process?” sidelines everything else. (I added the bold.) In truth, process is what matters most. Every shred of research points out the primacy of investment process, but it is still hard to get investors to look away from performance, even temporarily.

We focus on relative strength as a return factor—and we use a systematic process to extract whatever return is available—but it really doesn’t matter what return factor you use. Value investors, growth investors, or firms trying to harvest more exotic return factors must still have the same focus on investment process to be successful.

If you are an advisor, you should be able to clearly explain your investment process to a client. If you are an investor, you should be asking your advisor to explain their process to you. If there’s no consistent process, you might want to read Mr. Jaffe’s article again.

HT to Abnormal Returns

1 Comment | From the MM, Investor Behavior, Markets, Thought Process | Tagged: investment process, investor behavior, relative strength, return factor, systematic investment process | Permalink

Posted by:

Mike Moody

September 4, 2013

I’ve long been a fan of portfolio buckets or sleeves, for two reasons. The first reason is that it facilitates good diversification, which I define as diversification by volatility, by asset class, and by strategy. (We happen to like relative strength as one of these primary strategies, but there are several offsetting strategies that might make sense.) A bucket portfolio makes this kind of diversification easy to implement.

The second benefit is largely psychological—but not to be underestimated. Investors with bucket portfolios had better performance in real life during the financial crisis because they didn’t panic. While the lack of panic is a psychological benefit, the performance benefit was very real.

Another champion of bucketed portfolios is Christine Benz at Morningstar. She recently wrote a series of article in which she stress-tested bucketed portfolios, first through the 2007-2012 period (one big bear market) and then through the 2000-2012 period (two bear markets). She describes her methodology for rebalancing and the results.

If you have any interest in portfolio construction for actual living, breathing human beings who are prone to all kinds of cognitive biases and emotional volatility, these articles are mandatory reading. Better yet for fans of portfolio sleeves, the results kept clients afloat. I’ve included the links below. (Some may require a free Morningstar registration to read.)

Article: A Bucket Portfolio Stress Test http://news.morningstar.com/articlenet/article.aspx?id=605387∂=1

Article: We Put the Bucket System Through Additional Stress Tests http://news.morningstar.com/articlenet/article.aspx?id=607086

Article: We Put the Bucket System Through a Longer Stress Test http://news.morningstar.com/articlenet/article.aspx?id=608619

2 Comments | From the MM, Investor Behavior, Portfolio Theory, Thought Process | Tagged: behavioral finance, bucket, diversification, investor behavior, portfolio theory, relative strength | Permalink

Posted by:

Mike Moody

September 3, 2013

What the heck is fictive learning? Well, I’m glad you asked. Fictive learning refers to our ability to imagine “what if” situations. We learn not only from our actual actions, but from our perceptions of what would have happened if we had done something differently. It turns out that fictive learning has a lot to do with investor behavior too. Here are a few excerpts about relevant experiments discussed in an article in Wired magazine.

To better understand the source of our compulsive speculation, Read Montague, a neuroscientist now at Virginia Tech, has begun investigating the formation of bubbles from the perspective of the brain. He argues that the urge to speculate is rooted in our mental software. In particular, bubbles seem to depend on a unique human talent called “fictive learning,” which is the ability to learn from hypothetical scenarios and counterfactual questions. In other words, people don’t just learn from mistakes they’ve actually made, they’re able to learn from mistakes they might have made, if only they’d done something different.

Investors, after all, are constantly engaging in fictive learning, as they compare their actual returns against the returns that might have been, if only they’d sold their shares before the crash or bought Google stock when the company first went public. And so, in 2007, Montague began simulating stock bubbles in a brain scanner, as he attempted to decipher the neuroscience of irrational speculation. His experiment went like this: Each subject was given $100 and some basic information about the “current” state of the stock market. After choosing how much money to invest, the players watched nervously as their investments either rose or fell in value. The game continued for 20 rounds, and the subjects got to keep their earnings. One interesting twist was that instead of using random simulations of the stock market, Montague relied on distillations of data from famous historical markets. Montague had people “play” the Dow of 1929, the Nasdaq of 1998 and the S&P; 500 of 1987, so the neural responses of investors reflected real-life bubbles and crashes.

Montague, et. al. immediately discovered a strong neural signal that drove many of the investment decisions. The signal was fictive learning. Take, for example, this situation. A player has decided to wager 10 percent of her total portfolio in the market, which is a rather small bet. Then, she watches as the market rises dramatically in value. At this point, the investor experiences a surge of regret, which is a side-effect of fictive learning. (We are thinking about how much richer we would be if only we’d invested more in the market.) This negative feeling is preceded by a swell of activity in the ventral caudate, a small area in the center of the cortex. Instead of enjoying our earnings, we are fixated on the profits we missed, which leads us to do something different the next time around.

When markets were booming, as in the Nasdaq bubble of the late 1990s, people perpetually increased their investments. In fact, many of Montague’s subjects eventually put all of their money into the rising market. They had become convinced that the bubble wasn’t a bubble. This boom would be different.

And then, just like that, the bubble burst. The Dow sinks, the Nasdaq collapses, the Nikkei implodes. At this point investors race to dump any assets that are declining in value, as their brain realizes that it made some very expensive mistakes. Our investing decisions are still being driven by regret, but now that feeling is telling us to sell. That’s when we get a financial panic.

Montague has also begun exploring the power of social comparison, or what he calls the “country club effect,” on the formation of financial bubbles. “This is what happens when you’re sitting around with your friends at the country club, and they’re all talking about how much money they’re making in the market,” Montague told me. “That casual conversation is going to change the way you think about investing.” In a series of ongoing experiments, Montague has studied what happens when people compete against each other in an investment game. While the subjects are making decisions about the stock market, Montague monitors their brain activity in two different fMRI machines. The first thing Montague discovered is that making more money than someone else is extremely pleasurable. When subjects “win” the investment game, Montague observes a large increase in activity in the striatum, a brain area typically associated with the processing of pleasurable rewards. (Montague refers to this as “cocaine brain,” as the striatum is also associated with the euphoric high of illicit drugs.) Unfortunately, this same urge to outperform others can also lead people to take reckless risks.

More recently, a team of Italian neuroscientists led by Nicola Canessa and Matteo Motterlini have shown that regret is also contagious, so that “observing the regretful outcomes of another’s choices reactivates the regret network.” (In other words, we internalize the errors of others. Or, as Motterlini wrote in an e-mail, “We simply live their emotions like these were our own.”) Furthermore, this empathy impacts our own decisions: The “risk-aptitude” of investors is significantly shaped by how well the risky decisions of a stranger turned out. If you bet the farm on some tech IPO and did well, then I might, too.

If you are an investment advisor, all of this is sounding pretty familiar. We’ve all seen clients make decisions based on social comparison, regret, or trying to avoid regret. Sometimes they are simply paralyzed, trapped between wanting to do as well as their brother-in-law and wanting to avoid the regret of losing money if their investment doesn’t work out.

The broader point is that a lot of what drives trends in the market is rooted in human behavior, not valuations and fundamentals. Human nature is unlikely to change, especially a feature like fictive learning which is actually incredibly helpful in many other contexts. As a result, markets will continue to trend and reverse, to form bubbles and to have those bubbles implode periodically.

While social science may be helpful in understanding why the market behaves as it does, we still have to figure out a way to navigate it. As long as markets trend, relative strength trend following should work. (That’s the method we follow.) As long as bubbles form and implode, other methods like buying deep value should help mitigate the risk of permanent loss. Most important, the discipline to execute a systematic investment plan and not get sucked into all of the cognitive biases will be necessary to prosper with whatever investment method you choose.

177 Comments | From the MM, Investor Behavior, Thought Process | Tagged: behavioral finance, fictive learning, investor behavior, relative strength, systematic investment process | Permalink

Posted by:

Mike Moody

August 30, 2013

Index Universe carried an interview with Tad Rivelle, the chief investment officer at Trust Company of the West, that touched on the difference between finance theory and the reality in the markets. Mr. Rivelle is mainly a bond guy and the interview mostly discussed interest rates and so on, but it contained this gem:

IU.com: We’re hearing projections of 3.5 percent rates by next year, 4.5 percent by 2015. What happens if the bond market decides to rush there at once rather than to gradually get to those levels? Could it derail the economic recovery?

Rivelle: Yes. In fact, that’s precisely what we saw when we had that taper tantrum back in May and June. It was catalyzed by Bernanke’s statement to the effect that the Fed was carefully considering an initiation of a taper late this year, and the bond market sold off horrifically in a very short period of time. It was a generalized deleveraging. I think it frightened the Fed, and consequently they walked those comments back.

The conflict here is that the Fed tends to approach things from a model-driven academic perspective—what’s supposed to happen in theory versus the realities of the marketplace. When people are looking to front-run one another to offload risk before the next guy does, these models basically go out the window.

How the bond market will respond is absolutely unknown, but it’s more typical for the bond market to move very rapidly, to gallop to what it believes is the next point of equilibrium and not to sell off gradually. I’ve never seen that happen.

I put the fun part in bold—in a real market, academic models go out the window and human behavior takes over. Mr. Rivelle points out that markets trade on perception, and often make adjustments abruptly when perceptions change.

To me, this is the real strength of tactical asset allocation driven by relative strength. As perceptions change, different securities or asset classes come to the forefront and others fade away. As relative strength investors, we don’t have to predict what these changes might be. We simply have to adapt our portfolio as the changes occur. Relative strength adapts to changes in human behavior, not some elusive equilibrium proposed by academics.

Leave a Comment » | Markets, Tactical Asset Alloc, Thought Process | Tagged: finance theory, relative strength, Tactical Asset Allocation | Permalink

Posted by:

Mike Moody

August 28, 2013

At first, you might not think that relative strength and philosophy are related in any way. But they are, because every strategy is based on some philosophy of the market. Different philosophies lead to different strategies. We like relative strength because it is simple, straightforward, and performs well over time. Of course, there are other strategies that work also, including some that are quite complementary to relative strength. A nice encapsulation of philosophy leading to strategy appeared on The Bloodhound System blog. A couple of excerpts from the article are instructive. The first is a quote from Rick Ferri in a Morningstar interview:

“Strategy comes from philosophy. If you don’t have a philosophy, you can develop a strategy, but it’s only going to blow apart the next time it doesn’t work for a month or two. And you are going to go onto another strategy, and that’s the worst thing you can do.”

This is very true. Over my career, I’ve seen many investors careen from strategy to strategy, never sticking long enough with any of them to enjoy success. The author of the blog piece, Bill Moore, I think really cuts to the core of why a deeply held philosophy is so important to success. Having some kind of belief system is necessary to have conviction. With conviction comes discipline—and discipline is the key to everything. I put the good part in bold.

…what’s really important is that you have a philosophy that makes sense to you and that you believe in–and that you then create a strategy which you would execute with discipline. As much as pundits might dogmatically espouse one investing philosophy or another–making it seem like it’s their way or the highway–there are thousands of investment philosophies–and in turn strategies. The reason multiple philosophies can work out well is that inherent in having a philosophy, or belief system, is that you have conviction in it. That kind of discipline, not so much the philosophy itself, is the key to an investment plan.

One of our senior portfolio managers, Harold Parker, likes to say “to the disciplined go the spoils.” He’s right. Even a good strategy that is poorly executed will lead to bad results. Every strategy might be driven by some philosophy, but none of them are worth a darn without conviction and the resultant discipline to execute well.

Leave a Comment » | From the MM, Investor Behavior, Thought Process | Tagged: investor behavior, relative strength, strategy | Permalink

Posted by:

Mike Moody

August 8, 2013

Simplicity is the ultimate sophistication.—-Leonardo di Vinci

This quotation doubles as the title of a Vanguard piece discussing the merits of a simple fund portfolio. However, it occurred to me that their guidelines that make the simple fund portfolio work are the same for making any investment strategy work. They are:

- adopt the investment strategy

- embrace it with confidence, and

- endure the inevitable ups and downs in the markets

Perhaps this seems obvious, but we see many investors acting differently, more like this:

- adopt the investment strategy that has been working lately

- embrace it tentatively, as long as it has good returns

- bail out during the inevitable ups and downs in the markets

- adopt another investment strategy that has been working lately…

You can see the problem with this course of action. The investment strategy is only embraced at the peak of popularity—usually when it’s primed for a pullback. Even that would be a minor problem if the commitment to the investment strategy were strong. But often, investors bail out somewhere near a low. This is the primary cause of poor investor returns according to DALBAR.

Investing well need not be terribly complicated. Vanguard’s three guidelines are good ones, whether you adopt relative strength as we have or some different investment strategy. If the strategy is reasonable, commitment and patience are the big drivers of return over time. As Vanguard points out:

Complexity is not necessarily sophisticated, it’s just complex.

Words to live by.

Leave a Comment » | From the MM, Investor Behavior, Portfolio Theory, Thought Process | Tagged: patience, relative strength, strategy | Permalink

Posted by:

Mike Moody

July 31, 2013

Modern portfolio theory imagines that you can construct an optimal portfolio, especially if you can find investments that are uncorrelated. There’s a problem from the correlation standpoint, though. As James Picerno of The Capital Spectator points out, correlations are rising:

A new study from the Bank of International Settlements (BIS) raises doubts about the value of commodities as a tool for enhancing portfolio diversification. The paper’s smoking gun, so to speak, is that “the correlation between commodity and equity returns has substantially increased after the onset of the recent financial crisis.”

Correlations are a key factor in the design and management of asset allocation, but they’re not the only factor. And even if we can find assets and strategies with reliably low/negative correlations with, say, equities, that alone isn’t enough, as I discussed last week. You also need to consider other factors, starting with expected return. It may be tempting to focus on one pair of assets and consider how the trailing correlation stacks up today. But that’s hardly the last word on making intelligent decisions on how to build a diversified portfolio.

As more investors pile into commodities, REITs, hedge funds, and other formerly obscure corners, the historical diversification benefits will likely fade. Granted, the outlook for expected diversification benefits fluctuates through time, and so what looks unattractive today may look considerably more compelling tomorrow (and vice versa). But as a general proposition, it’s reasonable to assume that correlations generally will inch closer to 1.0. That doesn’t mean that diversifying across asset classes is destined to become worthless, but the expected payoff is likely to dim with the passage of time.

Mathematically, any two items that are not 100% correlated will reduce volatility when combined. But that doesn’t necessarily mean it’s a good addition to your portfolio—or that modern portfolio theory is a very good way to construct a portfolio. (We will set aside for now the MPT idea that volatility is necessarily a bad thing.) The article includes a nice graphic, reproduced below, that shows how highly correlated many asset classes are with the US market, especially if you keep in mind that these are 36-month rolling correlations. Many asset classes may not reduce portfolio volatility much at all.

Source: The Capital Spectator (click on image to enlarge)

As Mr. Picerno points out, optimal allocations are far more sensitive to returns than to correlations or volatility. So even if you find a wonderfully uncorrelated investment, if it has a lousy return it may not help the overall portfolio much. It would reduce volatility, but quite possibly at a big cost to overall returns. The biggest determinant of your returns, of course, is what assets you actually hold and when. The author puts this a slightly different way:

Your investment results also rely heavily on how and when you rebalance the mix.

Indeed they do. If you hold equities when they are doing well and switch to other assets when equities tail off, your returns will be quite different than an investor holding a static mix. And your returns will be way different than a scared investor that holds cash when stocks or other assets are doing well.

In other words, the return of your asset mix is what impacts your performance, not correlations or volatility. This seems obvious, but in the fog of equations about optimal portfolio construction, this simple fact is often overlooked. Since momentum (relative strength) is generally one of the best-performing and most reliable return factors, that’s what we use to drive our global tactical allocation process. The idea is to own asset classes as long as they are strong—and to replace them with a stronger asset class when they begin to weaken. In this context, diversification can be useful for reducing volatility, if you are comfortable with the potential reduction in return that it might entail. (We generally advocate diversifying by volatility, by asset class, and by strategy, although the specific portfolio mix might change with the preference of the individual investor.) If volatility is well-tolerated, maybe the only issue is trying to generate the strongest returns.

Portfolio construction can’t really be reduced to some “optimal” set of tradeoffs. It’s complicated because correlations change over time, and because investor preferences between return and volatility are in constant flux. There is nothing stable about the portfolio construction process because none of the variables can be definitively known; it’s always an educated approximation. Every investor gets to decide—on an ongoing basis—what is truly important: returns (real money you can spend) or volatility (potential emotional turmoil). I always figure I can afford Maalox with the extra returns, but you can easily see why portfolio management is overwhelming to so many individual investors. It can be torture.

Portfolio reality, with all of its messy approximations, bears little resemblance to the seeming exactitude of Modern Portfolio Theory.

6 Comments | Markets, Portfolio Theory | Tagged: diversification, factor investing, momentum, portfolio theory, relative strength, Tactical Asset Allocation, volatility | Permalink

Posted by:

Mike Moody

July 30, 2013

Advisor Perspectives recently carried an article by Michael Nairne of Tacita Capital about factor investing. The article discussed a number of aspects of factor investing, including factor performance and periods of factor underperformance (factor failure). The remarkable thing about relative strength (termed momentum in his article) is the nice combination of strong performance and relatively short periods of underperformance that it affords the investor seeking alpha.

Mr. Nairne discusses a variety of factors that have been shown to generate excess returns over time. He includes a chart showing their performance versus the broad market.

Source: Advisor Perspectives/Tacita Capital (click on image to enlarge)

Yep, the one at the top is momentum.

All factors, even very successful ones, underperform from time to time. In fact, the author points out that these periods of underperformance might even contribute to their factor returns.

No one can guarantee that the return premia originating from these dimensions of the market will persist in the future. But, the enduring nature of the underlying causes – cognitive biases hardwired into the human psyche, the impact of social influences and incremental risk – suggests that higher expected returns should be available from these factor-based strategies.

There is another reason to believe that these strategies offer the prospect of future return premia for patient, long-term investors. These premia are very volatile and can disappear or go negative for many years. The chart on the following page highlights the percentage of 36-month rolling periods where the factor-based portfolios – high quality, momentum, small cap, small cap value and value – underperformed the broad market.

To many investors, three years of under-performance is almost an eternity. Yet, these factor portfolios underperformed the broad market anywhere from almost 15% to over 50% of the 36-month periods from 1982 to 2012. If one were to include the higher transaction costs of the factor-based portfolios due to their higher turnover, the incidence of underperformance would be more frequent. One of the reasons that these premia will likely persist is that many investors are simply not patient enough to stay invested to earn them.

The bold is mine, but I think Mr. Nairne has a good point. Many investors seem to believe in magic and want their portfolio to significantly outperform—all the time.

That’s just not going to happen with any factor. Not surprisingly, though, momentum has tended to have shorter stretches of underperformance than many other factors, a consideration that might have been partially responsible for its good performance over time. Mr. Nairne’s excellent graphic on periods of factor failure is reproduced below.

Source: Advisor Perspectives/Tacita Capital (click on image to enlarge)

Once again, whether you choose to try to harvest returns from relative strength or from one of the other factors, patience is an underrated component of actually receiving those returns. The market can be a discouraging place, but in order to reap good factor performance you have to stay with it during the inevitable periods of factor failure.

132 Comments | Markets, Portfolio Theory, Relative Strength Research | Tagged: factor failure, factor investing, momentum, patience, relative strength | Permalink

Posted by:

Mike Moody

July 22, 2013

…has been discovered by the Wall Street Journal. Recently, they wrote an article about better ways to index—alternative beta—and referenced a study by Cass Business School. (We wrote about this study here in April.)

Here’s the WSJ’s take on the Cass Business School study:

The Cass Business School researchers examined how 13 alternative index methodologies would have performed for the 1,000 largest U.S. stocks from 1968 to 2011.

All 13 of the alternative indexes produced higher returns than a theoretical market-cap index the researchers created. While the market-cap index generated a 9.4% annualized return over the full period, the other indexes delivered between 9.8% and 11.4%. The market-cap-weighted index was the weakest performer in every decade except the 1990s.

The most interesting part of the article, to me, was the discussion of the growing acceptance of alternative beta. This is truly exciting.

Indeed, a bevy of funds tracking alternative indexes have been launched in recent years. And their popularity is soaring: 43% of inflows into U.S.-listed equity exchange-traded products in the first five months of 2013 went to products that aren’t weighted by market capitalization, up from 20% for all of last year, according to asset manager BlackRock Inc.

And then there was one mystifying thing: although one of the best-performing alternative beta measures is relative strength (“momentum” to academics), relative strength was not mentioned in the WSJ article at all!

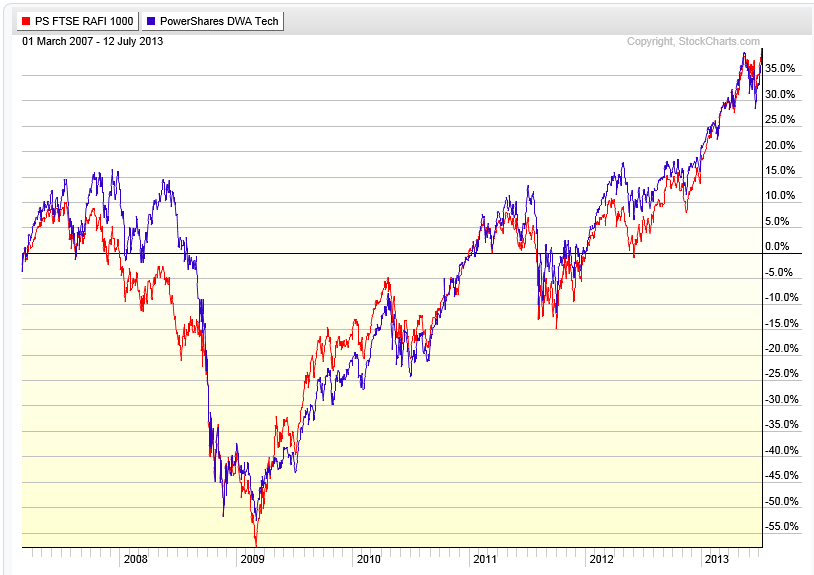

Instead there was significant championing of fundamental indexes. Fundamental indexes are obviously a valid form of alternative beta, but I am always amazed how relative strength flies under the radar. (See The #1 Investment Return Factor No One Wants to Talk About.) Indeed, as you can see from the graphic below, the returns of two representative ETFs, PRF and PDP are virtually indistinguishable. One can only hope that relative strength will eventually gets its due.

The performance numbers above are pure price returns, based on the applicable index not inclusive of dividends, fees, commissions, or other expenses. Past performance not indicative of future results. Potential for profits accompanied by possibility of loss. See www.powershares.com for more information.

1 Comment | Portfolio Theory, Relative Strength Research, Thought Process | Tagged: etf, factor investing, momentum, PDP, relative strength | Permalink

Posted by:

Andy Hyer

July 22, 2013

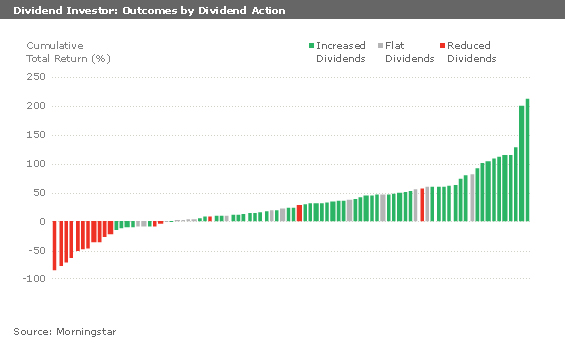

Dividend investing is all the rage these days. It can be a valuable investment strategy if it is done well—and a very negative experience if it is done poorly. The editor of Morningstar’s DividendInvestor, Josh Peters, recently penned a great column after his model portfolio collected its 1000th dividend payment. The article involves the lessons he learned in his foray into dividend investing. It is a must-read for all dividend investors.

One interesting thing, to me, was that many of the dividend investing problems that he experienced could have been avoided with a relative strength screen. (We use just such a screeen for the First Trust dividend UITs we specify the portfolios for.) Allow me to explain what I mean.

Morningstar’s first lesson was that quality was important in dividend investing. Mr. Peters writes:

The dividend cutters occupy a land of agony: We lost money on 13 of the 16 portfolio holdings that cut their dividends, and the 3 that have been profitable–General Electric (GE), U.S. Bancorp (USB), and Wells Fargo (WFC)–only pulled into the black long after their dividends began to recover.

One of the first things we noticed when screening the dividend investing universe by relative strength was this: companies that cut their dividends overwhelmingly had negative relative strength. In fact, when I looked through the list of S&P; Dividend Aristocrats that cut their dividends in the middle of the Great Recession, I discovered that all but two of them had negative relative strength before the dividend cut. Some had had poor relative strength for many years. Pitney Bowes (PBI) is just the most recent example. You can see from Morningstar’s chart below that most of their losses came from dividend cutters.

Source: Morningstar (click on image to enlarge)

In other words, screening for good relative strength is a pretty good insurance policy to avoid the land of agony.

Morningstar’s second lesson was that many of the best dividend stocks were not fundamentally cheap.

I’ve always believed dividends were the most important aspect of our investment strategy, but I’ve always been something of a cheapskate, too. I don’t like paying full price for anything if I can help it. In the first year or two of DividendInvestor’s run, I brought this impulse to my stock-picking, but I was often disappointed. In the banking industry, for example, I originally passed on top performers like M&T; (MTB) and gravitated toward statistically cheaper names like National City and First Horizon (FHN).

Guess what top performers have in common? You guessed it—good relative strength. A relative strength screen is also a useful way to avoid slugs that are cheap and never perform well.

The third lesson is just that time is important. If you are doing dividend investing, a lot of the benefit can come from compounding over time, or perhaps from reinvesting all of the yield.

If you choose to use the Dorsey Wright-managed First Trust UITs, we always recommend that you buy a series of four UITs and just keep rolling them over time. That way you always have a current portfolio of strong performers, screened to try to avoid some of the dividend cutters. If the portfolio appreciates over the holding period—beyond just paying out the dividend yield—it might make sense when you roll it over to use the capital gains to buy additional units, in an effort to have the payout level increase over time.

Even if you never use our products, you might want to consider some basic relative strength screening of your dividend stock purchases.

Past performance is not indicative of future results. Potential for profits is accompanied by possibility of loss. See http://www.ftportfolios.com for more information.

10 Comments | Markets, Thought Process | Tagged: dividend investing, relative strength | Permalink

Posted by:

Andy Hyer

July 18, 2013

Factor investing is one of the new frontiers in portfolio construction. We love this trend because relative strength (known as momentum to academics) is one of the premier factors typically used when constructing portfolios. The Technical Leaders ETFs that we construct for Powershares have really benefited from the movement toward factor investing.

Larry Swedroe recently wrote a glowing article on factor investing for Index Universe that serves as a good introduction. His article is full of great points distilled from a paper in the Journal of Index Investing. (The link to the journal paper is included in his article if you want to read the original source.)

The basic idea is that you can generate superior performance by building a portfolio of return factors. A corollary benefit is that because some of the factors are negatively correlated, you can often reduce the portfolio volatility as well. A couple of excerpts from his article should give you the flavor:

The evidence keeps piling up that investors can benefit from building portfolios that diversify across factors that not only explain stock market returns but that also generate superior returns.