John Rekenthaler at Morningstar, who usually has some pretty smart stuff to say, took on the topic of smart beta in a recent article. Specifically, he examined a variety of smart beta factors with an eye to determining which ones were real and might persist. He also thought some factors might be fool’s gold.

Here’s what he had to say about value:

The value premium has long been known and continues to persist.

And here’s what he had to say about relative strength (momentum):

I have trouble seeing how momentum can succeed now that its existence is well documented.

The italics are mine. I didn’t take logic in college, but it seems disingenuous to argue that one factor will continue to work after it is well-known, while becoming well-known will cause the other factor to fail! (If you are biased in favor of value, just say so, but don’t use the same argument to reach two opposite conclusions.)

There are a variety of explanations about why momentum works, but just because academics can’t agree on which one is correct doesn’t mean it won’t continue to work. It is certainly possible that any anomaly could be arbitraged away, but Robert Levy’s relative strength work has been known since the 1960s and our 2005 paper in Technical Analysis of Stocks & Commodities showed it continued to work just fine just the way he published it. Academics under the spell of efficient markets trashed his work at the time too, but 40 years of subsequent returns shows the professors got it wrong.

However, I do have a background in psychology and I can hazard a guess as to why both the value and momentum factors will continue to persist—they are both uncomfortable to implement. It is very uncomfortable to buy deep value. There is a terrific fear that you are buying a value trap and that the impairment that created the value will continue or get worse. It also goes against human nature to buy momentum stocks after they have already outperformed significantly. There is a great fear that the stock will top and collapse right after you add it to your portfolio. Investors and clients are quite resistant to buying stocks after they have already doubled, for example, because there is a possibility of looking really dumb.

Here’s the reason I think both factors are psychological in origin: it is absurdly easy to screen for either value or momentum. Any idiot can implement either strategy with any free screener on the web. Pick your value metric or your momentum lookback period and away you go. In fact, this is pretty much exactly what James O’Shaughnessy did in What Works on Wall Street. Both factors worked well—and continue to work despite plenty of publicity. So the barrier is not that there is some secret formula, it’s just that investors are unwilling to implement either strategy in a systematic way–because of the psychological discomfort.

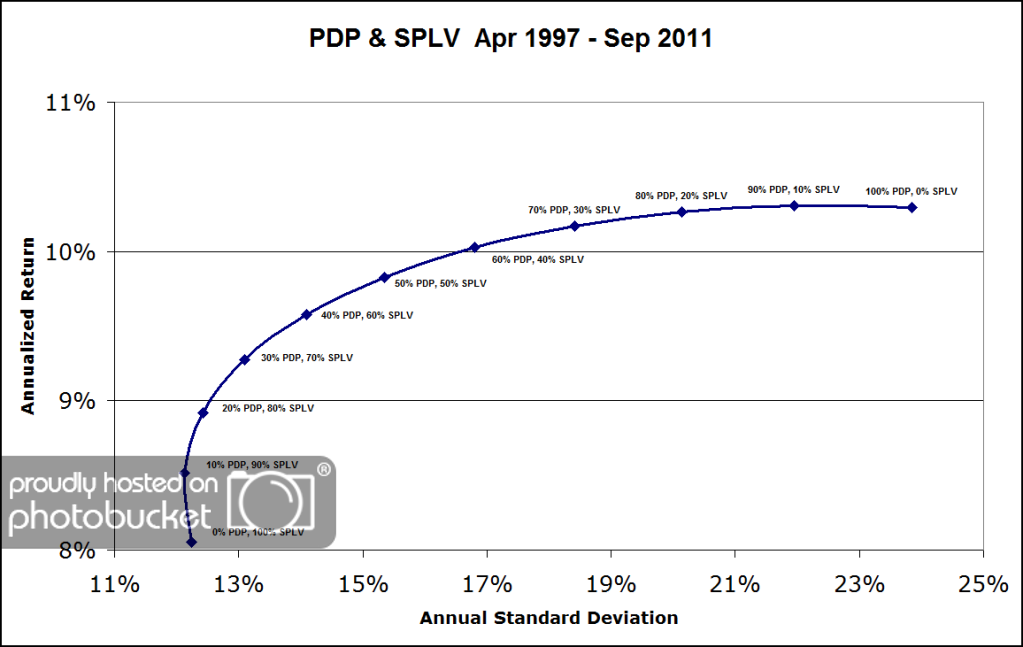

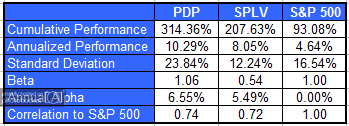

If I were to make an argument—the behavioral finance version—about which smart beta factor could potentially be arbitraged away over time, I would have to guess low volatility. If you ask clients whether they would prefer to buy stocks that a) had already dropped 50%, b) had already gone up 50%, or c) had low volatility, I think most of them would go with “c!” (Although I think it’s also possible that aversion to leverage will keep this factor going.)

Value and momentum also happen to work very well together. Value is a mean reversion factor, while momentum is a trend continuation factor. As AQR has shown, the excess returns of these two factors (unsurprisingly, once you understand how they are philosophical opposites) are uncorrelated. Combining them may have the potential to smooth out an equity return stream a little bit. Regardless, two good return factors are better than one!