September 26, 2012

Exchange traded funds comprise of groups of assets that are traded on the stock exchange. Similarly to mutual funds, ETFs track a basket of securities. This makes them more diversified than a single stock. Yet like stocks, they are easily traded, can be sold short, and often have lower transaction costs than mutual funds. ETFs tend to perform best under a buy-and-hold approach, but has the ease at which they trade caused investors to trade them more? Vanguard set out to answer this question.

They looked at “3.2 million transactions in more than 500,000 positions held in the mutual fund and ETF share classes of four different Vanguard funds from 2007-2011.” While ETFs were traded more often, mutual funds and exchange traded funds still had similar trading patterns.

Some in the investment community have suggested that ETFs tempt investors to increase their trading activity. Given the lack of investor-level analysis supporting or refuting this presumption, we examined the trading behavior of Vanguard investors. We found that, contrary to speculations in the popular media, most investments are held in a prudent, buy-and-hold manner, regardless of share class. Although behavior in ETFs is more active than behavior in traditional mutual funds, some of that difference is simply due to the fact that investors who are inclined to trade choose ETFs, not that investors who choose ETFs are induced to trade. We conclude that the ETF “temptation effect” is not a significant reason for long-term individual investors to avoid using appropriate ETF investments as part of a diversified investment portfolio.

In short, it is investors themselves that are responsible for increased trading of ETFs, not an inherent quality of the funds. Owning exchange traded funds won’t lure a long-term owner toward short-term trading.

2 Comments |

2 Comments |  Investor Behavior, Markets | Tagged: etf, mutual fund, trade, trend |

Investor Behavior, Markets | Tagged: etf, mutual fund, trade, trend |  Permalink

Permalink

Posted by:

Amanda Schaible

August 16, 2012

Let’s face it; investors often make bad investment decisions. Commonly, this is due to our emotions getting in the way. BlackRock lists some of the emotional investment tendencies that often cloud our judgment and steer us toward poor decisions:

- Anchoring: Holding onto a reference point, even if it’s irrelevant. For example, a $1.5 million house, being presented on its own, might sound expensive. But if you were first shown a $2 million house, and afterwards shown the $1.5 million house, it might then sound like a good deal.

- Herding: Following the crowd. People often pile into the markets when they are doing well and they see “everyone else” doing it.

- Mental Accounting: Separating money into buckets that are treated differently. Earmarking funds for college savings or a vacation home allows you to save for specific goals. But treating those dollars differently may not make sense when they all have the same buying power.

- Framing: Making a different decision based on context. In a research study, when a four-ounce glass had 2 ounces of water poured out of it, 69% of people said it was now “half empty.” If the same glass starts out empty and has 2 ounces of water poured into it, 88% of people say it is “half full.”

Emotional investment tendencies can result in all sorts of problems. Typically these behaviors are so ingrained that we don’t even recognize them as irrational!

One way to combat our emotions is to hire a good advisor. As explained in this previous blog post, one important benefit—maybe even the primary benefit—of having a good advisor is behavior modification. An advisor persuading a client to invest more when the market is doing poorly, instead taking money out, is extremely valuable.

Another option is to invest in a managed product like an ETF or mutual fund (here are some of ours) that will make the decisions for you. For an emotional investor, this may be an easier (and presumably safer) option than picking and obsessively monitoring a few random stocks. Even then, it is important try to avoid the herd mentality. Data shows that it’s most important to avoid panic at market bottoms. Although it is difficult not to panic if other people around you are fearful, the potential difference in your investment return can be significant.

In short, understanding your emotional tendencies may help keep them from interfering in investment decisions. If that isn’t enough, try enlisting the help of an outside source. With the steady hand of a good advisor, it may be possible to mitigate emotional investment tendencies.

2 Comments | Investor Behavior, Markets | Tagged: advice, advisor, etf, investment, investor behavior, mental accounting, personal finance | Permalink

Posted by:

Amanda Schaible

August 13, 2012

It’s fashionable to bash the US, what with a gridlocked Congress and the fiscal cliff, but if you’re looking to expand your portfolio, you might seriously consider investing domestically instead of overseas. U.S. companies have multiple benefits that you may not find elsewhere. Surprisingly, Politico recently outlined some of America’s investment advantages:

First, the U.S. has favorable demographics — thanks to its relatively high birth rates and immigration. While the BRIC countries —Brazil, Russia, India and China— have generated extraordinary economic growth, the U.S.remains a magnet for many of the smartest, most ambitious people in the world.

Second, the ability to better tap into domestic sources of energy — natural resource-based and, to a lesser but promising extent, the growing array of clean technologies — will spur more job-creating investments, improving our balance of payments.

Third, U.S. policymakers were aggressive in responding to the financial crisis, and the financial sector has been quick to increase capital and reduce leverage.

Fourth, U.S. companies have restructured more quickly and more extensively than others since 2008 — boosting U.S. productivity growth.

The United States is a logical place to invest, but it is not without its problems. Politico also lists ways the United States could improve. Some advice is to “make progress on the long-run fiscal situation…make it easier for people to immigrate…and invest in infrastructure.”

There is no golden place for investment all the time, but it’s useful to understand the pros and cons when deciding where to put your money. Especially given the current strength in the dollar, you could do worse than domestic companies.

American companies have some structural advantages

Source: hotzoneonline

(For those of you interested in investing domestically, we offer two U.S. relative strength ETFs (PDP and DWAS) and a full suite of separate account options. Give Andy a call. He’s been a little lonely lately!)

Please see www.powershares.com for more information. A list of all holdings for the trailing 12 months is available upon request. The Dorsey Wright SmallCap Technical Leaders Index is calculated by Dow Jones, the marketing name and a licensed trademark of CME Group Index Services LLC (“CME Indexes”). “Dow Jones Indexes” is a service mark of Dow Jones Trademark Holdings LLC (“Dow Jones”). Products based on the Dorsey Wright SmallCap Technical Leaders IndexSM, are not sponsored, endorsed, sold or promoted by CME Indexes, Dow Jones and their respective affiliates make no representation regarding the advisability of investing in such product(s).

Click here and here for disclosures. Past performance is no guarantee of future returns.

Comments Off on A Case for American Investment | Investor Behavior, Markets | Tagged: america, cons, invest, investment, pros, U.S. | Permalink

Posted by:

Amanda Schaible

August 3, 2012

Here we have the next round of the Dorsey, Wright Sentiment Survey, the first third-party sentiment poll. Participate to learn more about our Dorsey, Wright Polo Shirt raffle! Just follow the instructions after taking the poll, and we’ll enter you in the contest. Thanks to all our participants from last round.

As you know, when individuals self-report, they are always taller and more beautiful than when outside observers report their perceptions! Instead of asking individual investors to self-report whether they are bullish or bearish, we’d like financial advisors to weigh in and report on the actual behavior of clients. It’s two simple questions and will take no more than 20 seconds of your time. We’ll construct indicators from the data and report the results regularly on our blog–but we need your help to get a large statistical sample!

Click here to take Dorsey, Wright’s Client Sentiment Survey.

Contribute to the greater good! It’s painless, we promise.

Comments Off on Dorsey, Wright Client Sentiment Survey – 8/3/12 | Sentiment | Permalink

Posted by:

Amanda Schaible

August 3, 2012

After poor stock market performance over the past few years, many investors are holding on to cash. A survey by BlackRock ranks the reasons why people aren’t investing, and the results may be different from what you had expected.

Uncertainty about where to invest (37%)

Belief that it’s a poor investing environment (26%)

Fear of investing/losing money (23%)

Previous portfolio losses (8%)

Not applicable, have not pulled back on investment activity (6%)

Investors are not completely closed off to the idea of investing, but instead don’t know where they should put their money. One of the chief benefits of employing a relative strength strategy is that it provides the framework for allocating assets–thereby removing the biggest stumbling block to getting investors in the game.

1 Comment | Investor Behavior, Sentiment | Tagged: investment, market, sentiment | Permalink

Posted by:

Amanda Schaible

July 30, 2012

Our latest sentiment survey was open from 7/20/12 to 7/27/12. The Dorsey, Wright Polo Shirt Raffle continues to drive advisor participation, and we greatly appreciate your support! We will announce the winner early next week. This round, we had 49 advisors participate in the survey. If you believe, as we do, that markets are driven by supply and demand, client behavior is important. We’re not asking what you think of the market—since most of our blog readers are financial advisors, we’re asking instead about the behavior of your clients. Then we’re aggregating responses exclusively for our readership. Your privacy will not be compromised in any way.

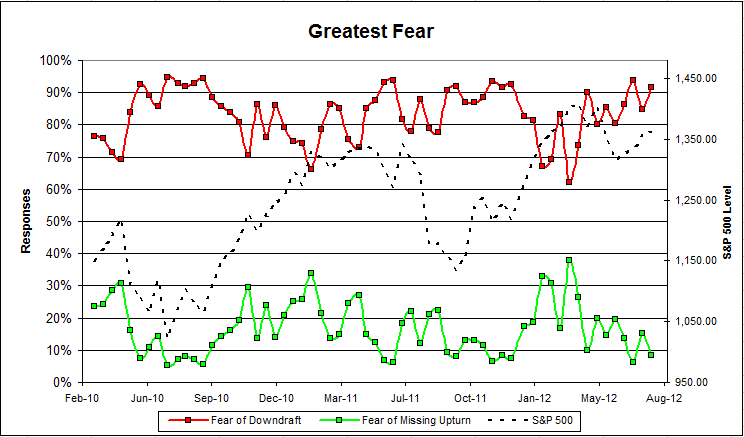

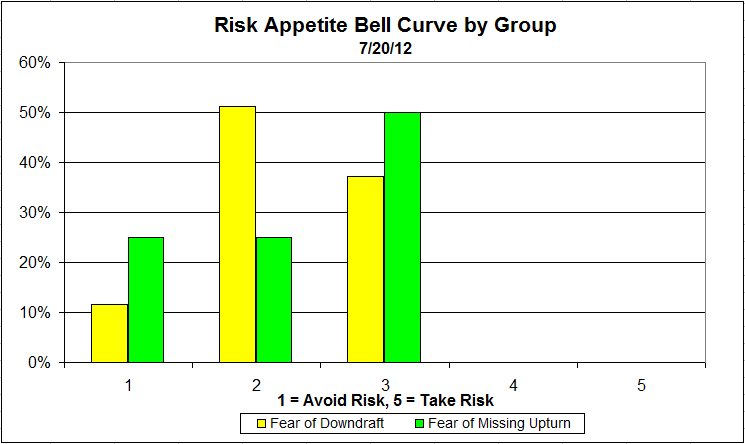

After the first 30 or so responses, the established pattern was simply magnified, so we are fairly comfortable about the statistical validity of our sample. Some statistical uncertainty this round comes from the fact that we only had four investors say that thier clients are more afraid of missing a stock upturn than being caught in a downdraft. Most of the responses were from the U.S., but we also had multiple advisors respond from at least two other countries. Let’s get down to an analysis of the data! Note: You can click on any of the charts to enlarge them.

Question 1. Based on their behavior, are your clients currently more afraid of: a) getting caught in a stock market downdraft, or b) missing a stock market upturn?

Chart 1: Greatest Fear. From survey to survey, the S&P; 500 rose 1.5%, but the greatest fear numbers did not perform as expected. The size of the fear of downturn group increased 85% to 91%, while fear of a missed upturn fell from 15% to 9%. Client sentiment remains poor even as the S&P; has risen.

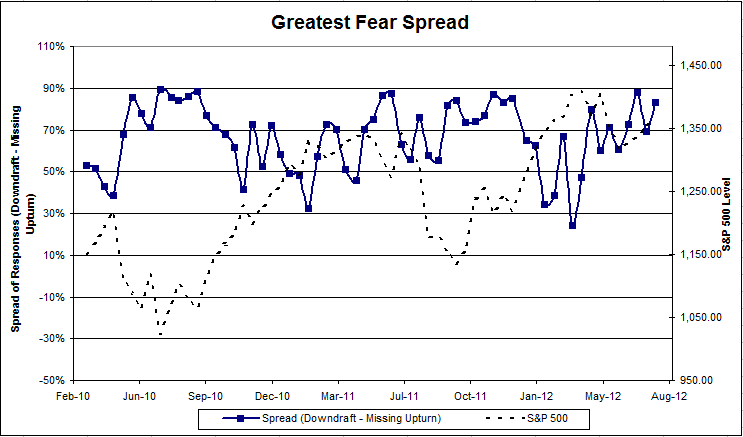

Chart 2: Greatest Fear Spread. Another way to look at this data is to examine the spread between the two groups. The spread increased from 69% to 83%.

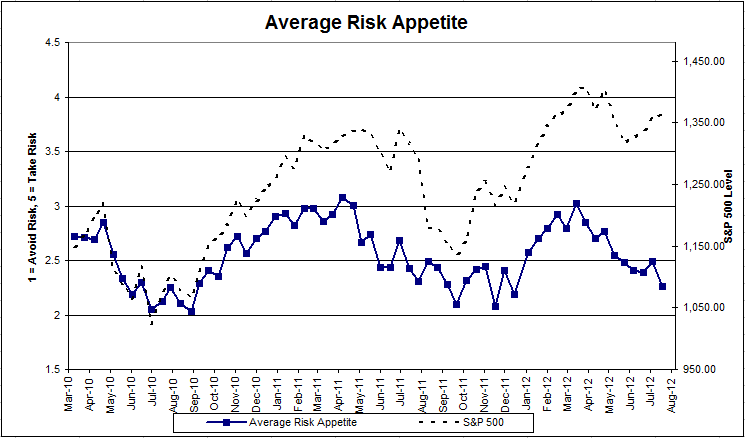

Question 2. Based on their behavior, how would you rate your clients’ current appetite for risk?

Chart 3: Average Risk Appetite. Average risk appetite usually falls in line with the market, but this week it did not. As the S&P; rose, average risk appetite fell from 2.49 to2.27.

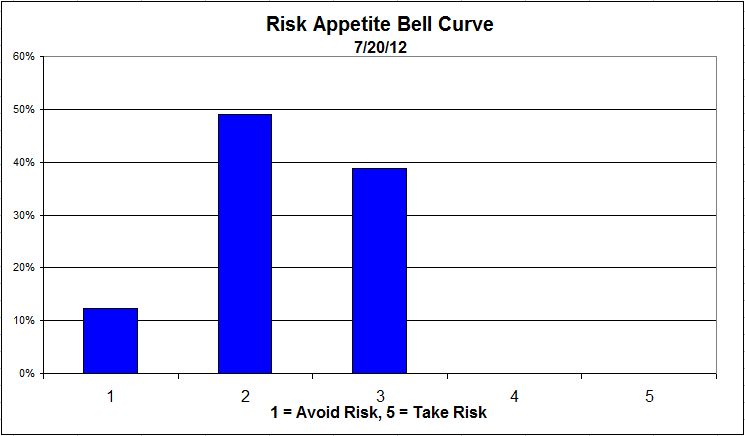

Chart 4: Risk Appetite Bell Curve. This chart uses a bell curve to break out the percentage of respondents at each risk appetite level. We are still seeing low risk appetites, with most clients having a risk appetite of 2 or 3. We had zero advisers say that their clients were looking for high risk investments this week.

Chart 5: Risk appetite Bell Curve by Group. The next three charts use cross-sectional data. The chat plots the reported client risk appetite separately for the fear of downdraft and for the fear of missing upturn groups. This chart performs partially as expected. A higher percentage of the fear of missing an upturn respondents have a risk appetite of 3. However, a higher percentage of the upturn respondents have a risk appetite of 1. Both groups prefer a relatively low amount of risk.

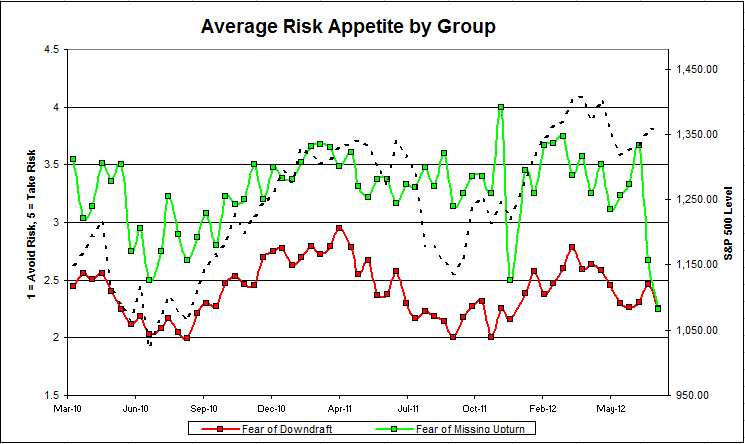

Chart 6: Average Risk Appetite by Group. The average risk appetite of both groups decreased this week, even as the market did well. The average risk appetite for the fear of missing an upturn group dropped to the lowest it has been since we started the survey. In fact, it converged with the average risk appetite of the fear of downdraft group.

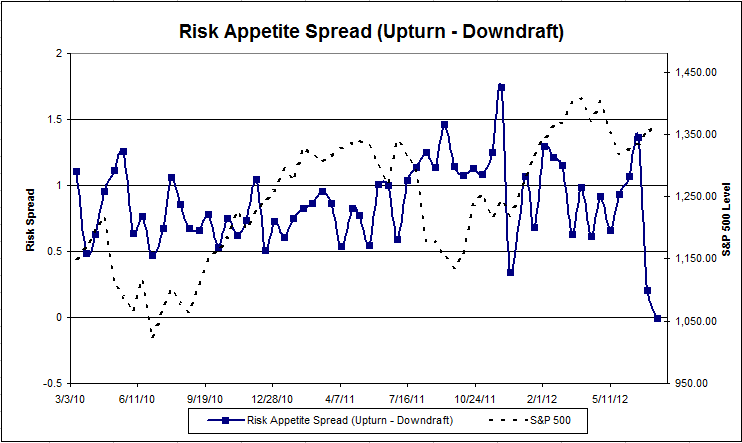

Chart 7: Risk Appetite Spread. This is a chart constructed from the data in Chart 6, where the average risk appetite of the downdraft group is subtracted from the average risk appetite of the missing upturn group. The spread decreased this round, and is the smallest spread we’ve seen yet.

The S&P; 500 rose by 0.59% from survey to survey, but most of our indicators did not respond accordingly. Average risk appetite fell, and more people feared a downturn. We’re not sure what caused such strange results this round.

No one can predict the future, as we all know, so instead of prognosticating, we will sit back and enjoy the ride. A rigorously tested, systematic investment process provides a great deal of comfort for clients during these types of fearful, highly uncertain market environments. Until next time, good trading and thank you for participating.

1 Comment | Investor Behavior, Markets, Sentiment | Permalink

Posted by:

Amanda Schaible

July 27, 2012

The chart below shows performance of US sectors and capitalizations over the trailing 12, 6, and 1 month(s). Performance updated through 7/26/2012.

Comments Off on Sector and Capitalization Performance | Markets, Uncategorized | Permalink

Posted by:

Amanda Schaible

July 25, 2012

We’ve just released a small-cap ETF with PowerShares (DWAS), which is the first U.S. relative strength small-cap ETF. We’ve done our own testing, of course, but it might also be instructive to take a look at other small-cap relative strength returns. Once again, we used the Ken French data library to calculate annualized returns and standard deviation. The construction of their relative strength index is explained here. The difference this time around is that we used small-cap stocks instead of large-cap stocks. Generally speaking, a small-cap stock is one whose price times number of outstanding shares (market capitalization) is between $300 million and $2 billion. However, the Ken French data used also includes micro-cap stocks which have an even smaller market capitalization (typically between $50-$300 million). Market cap is above $10 billion for large-cap stocks.

In the past, small-cap stocks have yielded high returns. They often perform well because companies in early stages of development have large growth potential. However, the potential of high earnings also comes with high risk. Small-cap companies face limited reserves, which make them more vulnerable than larger ones. Furthermore, in order to grow, they need to be able to replicate their business model on a bigger scale.

This is the sort of tradeoff investors must think about when choosing how to structure their portfolio. Typical factor models suggest that there are excess returns to be had in areas like value, relative strength, and small-cap, often at the cost of a little extra volatility. If you’re willing to take on more risk for the chance of higher returns, a portfolio that combines relative strength with small-cap stocks might be a good place to look!

Comments Off on Small-Cap Relative Strength Performance | Relative Strength Research | Tagged: cap, capitalization, etf, large, large cap, market, relative strength, small | Permalink

Posted by:

Amanda Schaible

July 24, 2012

The chart below is the spread between the relative strength leaders and relative strength laggards (universe of mid and large cap stocks). When the chart is rising, relative strength leaders are performing better than relative strength laggards. As of 7/23/2012:

The RS Spread continues to trade above its 50 day moving average.

Comments Off on Relative Strength Spread | Relative Strength Research | Tagged: spread | Permalink

Posted by:

Amanda Schaible

July 20, 2012

Here we have the next round of the Dorsey, Wright Sentiment Survey, the first third-party sentiment poll. Participate to learn more about our Dorsey, Wright Polo Shirt raffle! Just follow the instructions after taking the poll, and we’ll enter you in the contest. Thanks to all our participants from last round.

As you know, when individuals self-report, they are always taller and more beautiful than when outside observers report their perceptions! Instead of asking individual investors to self-report whether they are bullish or bearish, we’d like financial advisors to weigh in and report on the actual behavior of clients. It’s two simple questions and will take no more than 20 seconds of your time. We’ll construct indicators from the data and report the results regularly on our blog–but we need your help to get a large statistical sample!

Click here to take Dorsey, Wright’s Client Sentiment Survey.

Contribute to the greater good! It’s painless, we promise.

Comments Off on Dorsey, Wright Client Sentiment Survey – 7/20/12 | Sentiment | Permalink

Posted by:

Amanda Schaible

July 16, 2012

Our latest sentiment survey was open from 7/6/12 to 7/13/12. The Dorsey, Wright Polo Shirt Raffle continues to drive advisor participation, and we greatly appreciate your support! We will announce the winner early next week. This round, we had 59 advisors participate in the survey. If you believe, as we do, that markets are driven by supply and demand, client behavior is important. We’re not asking what you think of the market—since most of our blog readers are financial advisors, we’re asking instead about the behavior of your clients. Then we’re aggregating responses exclusively for our readership. Your privacy will not be compromised in any way.

After the first 30 or so responses, the established pattern was simply magnified, so we are comfortable about the statistical validity of our sample. Most of the responses were from the U.S., but we also had multiple advisors respond from at least three other countries. Let’s get down to an analysis of the data! Note: You can click on any of the charts to enlarge them.

Question 1. Based on their behavior, are your clients currently more afraid of: a) getting caught in a stock market downdraft, or b) missing a stock market upturn?

Chart 1: Greatest Fear. From survey to survey, the S&P; 500 rose 1.5%, and the greatest fear numbers performed as expected. The size of the fear of downturn group decreased from 94% to 85%, while fear of a missed upturn rose from 6% to 15%. Overall, client sentiment remains poor.

Chart 2: Greatest Fear Spread. Another way to look at this data is to examine the spread between the two groups. The spread decreased from 88% to 69%.

Question 2. Based on their behavior, how would you rate your clients’ current appetite for risk?

Chart 3: Average Risk Appetite. Once again, the average risk appetite performed as expected, rising from 2.39 to 2.49. This indicator continues to fall in line with the market.

Chart 4: Risk Appetite Bell Curve. This chart uses a bell curve to break out the percentage of respondents at each risk appetite level. We are still seeing a low amount of risk, with most clients wanting a risk appetite of 2 or 3. Very few clients are looking for high risk investments.

Chart 5: Risk appetite Bell Curve by Group. The next three charts use cross-sectional data. The chat plots the reported client risk appetite separately for the fear of downdraft and for the fear of missing upturn groups. This chart performs as expected, with the upturn group wanting more risk than the downturn group. However, both groups prefer a relatively low amount of risk and the difference between the two is slight.

Chart 6: Average Risk Appetite by Group. The average risk appetite of those who fear a downturn increased with a market. However, the average risk appetite of those who fear missing an upturn decreased drastically, even as the market did well.

Chart 7: Risk Appetite Spread. This is a chart constructed from the data in Chart 6, where the average risk appetite of the downdraft group is subtracted from the average risk appetite of the missing upturn group. The spread decreased this round, and is the smallest spread we’ve seen yet.

The S&P; 500 rose by 1.5% from survey to survey, and most of our indicators responded accordingly. Average risk appetite rose, and fewer people feared a downturn. However, both groups had low average risk appetites.

No one can predict the future, as we all know, so instead of prognosticating, we will sit back and enjoy the ride. A rigorously tested, systematic investment process provides a great deal of comfort for clients during these types of fearful, highly uncertain market environments. Until next time, good trading and thank you for participating.

Comments Off on Dorsey, Wright Client Sentiment Survey Results – 7/6/12 | Investor Behavior, Markets, Sentiment | Permalink

Posted by:

Amanda Schaible

July 3, 2012

In this post, I’ll be looking at another market indicator, the VIX, which is otherwise known as the fear index. The Chicago Board Options Exchange Market Volatility Index measures the expected market volatility over the next 30 days. When VIX is low, there is a low expectation of volatility; and when high, the opposite is true. The VIX is quoted in percentage points, and roughly correlates with the expected annualized percentage change of the S&P; 500.

Looking at monthly data starting in 1990, the VIX has ranged from about 10 at the end of January 2007 to about 60 at the end of October 2008. The highest reading ever was an intra-day high 89.53 on October, 24th 2008. In fact, 7 of the highest 10 readings have occurred since the financial crisis started in 2008.

To find returns, we’ve sorted the VIX into deciles, from lowest to highest. We then used Ken French’s high relative strength database (explained here) to determine the average percentage of growth 3, 6, and 12 months out.

Chart 1: Average Relative Strength Returns by VIX Decile.

The returns tend to have a U shape, with high returns at both extremes of the VIX. This is true when looking at all three periods (3, 6, and 12 months). Furthermore, average returns have been best when the VIX is extremely high rather than extremely low. To get some perspective, the bottom 20% of month-end readings range from 10 to 13, and the top 20% range from 25 to 60.

Even though some of the largest growth rates have occurred when the VIX is high, we must remember that most investors are risk averse and prefer low volatility. Therefore, convincing clients to invest when the VIX is high may be a daunting task. If you’d like to read more, both the VIX index and the preference for low volatility are discussed in this previous blog post.

There have been consistent relative strength return trends when looking at VIX readings over the past 22 years. If these trends continue, there may be high future returns next time the VIX hits an extreme level.

1 Comment | Investor Behavior, Relative Strength Research | Tagged: fear index, indicator, relative strength, returns, vix | Permalink

Posted by:

Amanda Schaible

July 2, 2012

Our latest sentiment survey was open from 6/22/12 to 6/29/12. The Dorsey, Wright Polo Shirt Raffle continues to drive advisor participation, and we greatly appreciate your support! We will announce the winner early next week. This round, we had 49 advisors participate in the survey. If you believe, as we do, that markets are driven by supply and demand, client behavior is important. We’re not asking what you think of the market—since most of our blog readers are financial advisors, we’re asking instead about the behavior of your clients. Then we’re aggregating responses exclusively for our readership. Your privacy will not be compromised in any way.

After the first 30 or so responses, the established pattern was simply magnified, so we are fairly comfortable about the statistical validity of our sample. Any statistical uncertainty this round comes from the fact that we only had three investors say that thier clients are more afraid of missing a stock upturn than being caught in a downdraft. Most of the responses were from the U.S., but we also had multiple advisors respond from at least three other countries. Let’s get down to an analysis of the data! Note: You can click on any of the charts to enlarge them.

Question 1. Based on their behavior, are your clients currently more afraid of: a) getting caught in a stock market downdraft, or b) missing a stock market upturn?

Chart 1: Greatest Fear. From survey to survey, the S&P; 500 increased 0.71%. The greatest fear numbers did not perform as expected. The fear of downturn group increased from 86% to 94%, while fear of a missed opportunity decreased from 14% to 6%. Client sentiment remains poor.

Chart 2: Greatest Fear Spread. Another way to look at this data is to examine the spread between the two groups. The spread increased from 73% to 88%.

Question 2. Based on their behavior, how would you rate your clients’ current appetite for risk?

Chart 3: Average Risk Appetite. Average risk appetite did not perform as expected. It fell slightly from 2.41 to 2.39, even though S&P; 500 rose.

Chart 4: Risk Appetite Bell Curve. This chart uses a bell curve to break out the percentage of respondents at each risk appetite level. We are still seeing a low amount of risk, with most clients having a risk appetite of 2 or 3.

Chart 5: Risk appetite Bell Curve by Group. The next three charts use cross-sectional data. The chat plots the reported client risk appetite separately for the fear of downdraft and for the fear of missing upturn groups. Those who fear a downdraft prefer a low amount of risk, with most clients having a risk appetite of 2 or 3. We only had three responses that indicated a fear of missing an upturn, but even our limited number of responses showed that these people do prefer more risk.

Chart 6: Average Risk Appetite by Group. The average risk appetite of those who fear a downturn increased slightly with the market. The average risk appetite of those who fear missing an upturn also increased.

Chart 7: Risk Appetite Spread. This is a chart constructed from the data in Chart 6, where the average risk appetite of the downdraft group is subtracted from the average risk appetite of the missing upturn group. The spread increased this round and is at its highest level so far this year.

The S&P; 500 rose by 0.71% from survey to survey, and some of our indicators responded accordingly. Average risk appetite by each group increased, but the total average risk appetite fell. As the market does better, we would expect more people to fear missing an upturn, yet more investors feared a downturn. Overall, client sentiment remains poor.

No one can predict the future, as we all know, so instead of prognosticating, we will sit back and enjoy the ride. A rigorously tested, systematic investment process provides a great deal of comfort for clients during these types of fearful, highly uncertain market environments. Until next time, good trading and thank you for participating.

Comments Off on Dorsey, Wright Client Sentiment Survey Results – 6/22/12 | Investor Behavior, Markets, Sentiment | Tagged: behavior, client, investor, sentiment, survey | Permalink

Posted by:

Amanda Schaible

June 22, 2012

Investors frequently rely on market indicators, such as moving averages, to decide when to buy, sell, or hold a stock. In fact we hear all the time of the magical powers of the moving average indicator, which has the mystical capabilities of keeping you out of trouble during market downturns, while making sure you are along for the ride on any rallies.

Therefore, we decided to test performance of Ken French’s High Relative Strength Index (an explanation of this index can be found here) against 50 and 200 day moving averages. We’ve calculated returns based on the assumption that the investor buys or holds when the price of the RS stock is above the moving average, and sells when the price drops below the moving average. So when the index is above its 50-, or 200-day moving average, we are fully invested, and when it’s below, we are out of the index.

Chart 1: Returns from 1963-2012. During this time period, basing buy and sell decisions off of the 50 day moving average is more successful than being fully invested. It is important to keep in mind that this data includes the bear markets of the 1970s and 2000s.

Chart 2: Returns from 1975-2007. When we start at a different point in time, the 50 day moving average performs much more poorly. In this dataset, we’ve cut out two large bear markets, and the effect on returns is drastic. In this case, it would have been better to just buy and hold.

Table 1: Annualized Returns by Time Periods. The average annualized returns also vary based on the period of time measured. At certain times, following moving averages outperforms being fully invested; but in other periods the opposite is true. Check out the difference between the two periods of ’83-’00 and ’66-’82. Using a moving average can either make or break your returns.

Charts 3 and 4: Fully Invested Ken French – Use of 50 Day MA (5 and 10 Year Performance). Investment performance based on moving averages varies greatly over time. In some periods, it performs incredibly, while in others it does terribly.

The performance of moving average based investment is directly related to the time period in which it is measured. As shown in Table 1, the returns can be completely different even in periods that partially overlap. The question then becomes not whether or not to use a moving average, but when! If you can predict the future, you’ll easily be able to decide whether or not to use a moving average when holding an index.

5 Comments | Relative Strength Research | Tagged: 200 day, 50 day, buy-and-hold, moving average, performance, relative strength, s&p500, stock market | Permalink

Posted by:

Amanda Schaible

June 18, 2012

Our latest sentiment survey was open from 6/8/12 to 6/15/12. The Dorsey, Wright Polo Shirt Raffle continues to drive advisor participation, and we greatly appreciate your support! We will announce the winner early next week. This round, we had 44 advisors participate in the survey. If you believe, as we do, that markets are driven by supply and demand, client behavior is important. We’re not asking what you think of the market—since most of our blog readers are financial advisors, we’re asking instead about the behavior of your clients. Then we’re aggregating responses exclusively for our readership. Your privacy will not be compromised in any way.

After the first 30 or so responses, the established pattern was simply magnified, so we are comfortable about the statistical validity of our sample. Most of the responses were from the U.S., but we also had multiple advisors respond from at least four other countries. Let’s get down to an analysis of the data! Note: You can click on any of the charts to enlarge them.

Question 1. Based on their behavior, are your clients currently more afraid of: a) getting caught in a stock market downdraft, or b) missing a stock market upturn?

Chart 1: Greatest Fear. From survey to survey, the S&P; 500 increased 0.59%, and the greatest fear numbers did not perform as expected. The fear of downturn group increased from 80% to 86%, while fear of a missed opportunity decreased from 20% to 14%. Client sentiment is still poor overall.

Chart 2: Greatest Fear Spread. Another way to look at this data is to examine the spread between the two groups. The spread decreased from 61% to 73%.

Question 2. Based on their behavior, how would you rate your clients’ current appetite for risk?

Chart 3: Average Risk Appetite. Once again, the average risk appetite performed as expected, rising from 2.48 to 2.62. As the market rose slightly, so did average risk appetite.

Chart 4: Risk Appetite Bell Curve. This chart uses a bell curve to break out the percentage of respondents at each risk appetite level. We are still seeing a low amount of risk, with most clients having a risk appetite of 2 or 3.

Chart 5: Risk appetite Bell Curve by Group. The next three charts use cross-sectional data. The chat plots the reported client risk appetite separately for the fear of downdraft and for the fear of missing upturn groups. This chart performs as expected, with the upturn group wanting more risk than the downturn group. However, even the fear of missing an upturn group doesn’t want a very high amount of risk.

Chart 6: Average Risk Appetite by Group. The average risk appetite of those who fear a downturn slightly decreased, even as the market rose. The average risk appetite of those who fear missing an upturn increased.

Chart 7: Risk Appetite Spread. This is a chart constructed from the data in Chart 6, where the average risk appetite of the downdraft group is subtracted from the average risk appetite of the missing upturn group. The spread increased this round, but is still within its normal range.

The S&P; 500 rose by 0.59% from survey to survey, and some of our indicators responded accordingly. Average risk appetite increased, but the amount of risk desired is still low. As the market does well, we would expect more people to fear missing an upturn; instead, more people feared a downturn. Overall, client sentiment remains poor.

No one can predict the future, as we all know, so instead of prognosticating, we will sit back and enjoy the ride. A rigorously tested, systematic investment process provides a great deal of comfort for clients during these types of fearful, highly uncertain market environments. Until next time, good trading and thank you for participating.

Comments Off on Dorsey, Wright Client Sentiment Survey Results – 6/8/12 | Investor Behavior, Markets, Sentiment | Tagged: client, investor behavior, sentiment, survey | Permalink

Posted by:

Amanda Schaible

June 12, 2012

In past posts (“Relative Strength vs. Value-Performance over Time” and “Relative Strength, Decade by Decade”), I’ve used the Ken French database’s relative strength portfolio. While this is useful in concept, what solidifies the findings in my previous posts is the similarity between Ken French’s High RS data and one of our ETFs, PDP.

PDP is a PowerShares ETF based on the Dorsey Wright Technical Leaders Index. It has its own proprietary calculation method, which is different than that of the Ken French database. Yet, over the past five years, both have performed very similarly.

Table 1:

PDP has only been on the market since March of 2007. Yet, over those five years, the two indexes have performed almost exactly the same…no small feat considering the stock market over the last few years. Imagine, then, using the Ken French data as a “loose proxy” for PDP going back decades. We’re not saying the two will always perform the same—we’re just pointing out that it’s clear both indexes are exploiting the same factor (RS) in a practical way.

Currently, relative strength growth rates (10-year rolling returns) are at some of the lowest levels since the 1930s; and historically we can see that growth rates often increase once they hit rock bottom. That may bode well for relative strength returns going forward.

Chart 1:

See www.powershares.com for more information about PDP. Past performance is no guarantee of future returns. A list of all holdings for the trailing 12 months is available upon request.

2 Comments | Markets, Relative Strength Research | Tagged: index, PDP, relative strength, return factors, stock market | Permalink

Posted by:

Amanda Schaible

June 5, 2012

This post explores relative strength success by decade, dating back to the 1930s. Once again, we’ve used the Ken French data library and CRSP database data. You can click here for a more complete explanation of this data.

Chart 1: Percent Outperformance by Decade. This chart shows the number of years in which relative strength has outperformed the CRSP universe each decade. RS outperformance has occurred in at least half of all years each decade.

Chart 2: Average 1-Year Performance by Decade. This chart shows the average yearly growth by decade of a relative strength portfolio and of the CRSP universe. Each decade, the average performance of relative strength has been greater than the average performance of the CRSP universe. Generally speaking, when the market’s average performance is increasing, RS outperforms CRSP by a greater percentage than it does when the market is doing poorly.

In short, relative strength has been a durable return factor for a very long time.

1 Comment | Relative Strength Research | Tagged: decade, historical, investment, momentum, over time, performance, relative strength | Permalink

Posted by:

Amanda Schaible

June 1, 2012

Our latest sentiment survey was open from 5/25/12 to 6/1/12. The Dorsey, Wright Polo Shirt Raffle continues to drive advisor participation, and we greatly appreciate your support! We will announce the winner early next week. This round, we had 66 advisors participate in the survey. If you believe, as we do, that markets are driven by supply and demand, client behavior is important. We’re not asking what you think of the market—since most of our blog readers are financial advisors, we’re asking instead about the behavior of your clients. Then we’re aggregating responses exclusively for our readership. Your privacy will not be compromised in any way.

After the first 30 or so responses, the established pattern was simply magnified, so we are comfortable about the statistical validity of our sample. Most of the responses were from the U.S., but we also had multiple advisors respond from at least four other countries. Let’s get down to an analysis of the data! Note: You can click on any of the charts to enlarge them.

Question 1. Based on their behavior, are your clients currently more afraid of: a) getting caught in a stock market downdraft, or b) missing a stock market upturn?

Chart 1: Greatest Fear. From survey to survey, the S&P; 500 fell -2.6%, and the greatest fear numbers did not perform as expected. The fear of downturn group decreased from 85% to 80%, while fear of a missed opportunity rose from 15% to 20%. Client sentiment remains poor overall.

Chart 2: Greatest Fear Spread. Another way to look at this data is to examine the spread between the two groups. The spread decreased from 71% to 61%.

Question 2. Based on their behavior, how would you rate your clients’ current appetite for risk?

Chart 3: Average Risk Appetite. Once again, the average risk appetite performed as expected, falling from 2.55 to 2.48. This indicator continues to fall in line with the market.

Chart 4: Risk Appetite Bell Curve. This chart uses a bell curve to break out the percentage of respondents at each risk appetite level. We are still seeing a low amount of risk, with most clients wanting a risk appetite of 2 or 3.

Chart 5: Risk appetite Bell Curve by Group. The next three charts use cross-sectional data. The chat plots the reported client risk appetite separately for the fear of downdraft and for the fear of missing upturn groups. This chart performs as expected, with the upturn group wanting more risk than the downturn group.

Chart 6: Average Risk Appetite by Group. The average risk appetite of those who fear a downturn decreased with a market. However, the average risk appetite of those who fear missing an upturn increased.

Chart 7: Risk Appetite Spread. This is a chart constructed from the data in Chart 6, where the average risk appetite of the downdraft group is subtracted from the average risk appetite of the missing upturn group. The spread increased this round, but is still within its normal range.

The S&P; 500 fell by -2.6% from survey to survey, and most of our indicators responded accordingly. Average risk appetite fell, but the fear of downturn group decreased. However, we’d expect the fear of downturn group to increase as the market does poorly, which didn’t happen this round.

No one can predict the future, as we all know, so instead of prognosticating, we will sit back and enjoy the ride. A rigorously tested, systematic investment process provides a great deal of comfort for clients during these types of fearful, highly uncertain market environments. Until next time, good trading and thank you for participating.

Comments Off on Dorsey, Wright Client Sentiment Survey Results – 5/25/12 | Investor Behavior, Markets, Sentiment | Permalink

Posted by:

Amanda Schaible

May 31, 2012

Thanks to the large amount of stock data available nowadays, we are able to compare the success of different strategies over very long time periods. The table below shows the performance of two investment strategies, relative strength (RS) and value, in relation to the performance of the market as a whole (CRSP) as well as to one another. It is organized in rolling return periods, showing the annualized average return for periods ranging from 1-10 years, using data all the way back to 1927.

The relative strength and value data came from the Ken French data library. The relative strength index is constructed monthly; it includes the top one-third of the universe in terms of relative strength. (Ken French uses the standard academic definition of price momentum, which is 12-month trailing return minus the front-month return.) The value index is constructed annually at the end of June. This time, the top one-third of stocks are chosen based on book value divided by market cap. In both cases, the universes were composed of stocks with market capitalizations above the market median.

Lastly, the CRSP database includes the total universe of stocks in the database as well as the risk-free rate, which is essentially the 3-month Treasury bill yield. The CRSP data serves as a benchmark representing the generic market return. It is also worthwhile to know that the S&P; 500 and DJIA typically do worse than the CRSP total-market data, which makes CRSP a harder benchmark to beat.

Source:Dorsey Wright Money Management

The data supports our belief that relative strength is an extremely effective strategy. In rolling 10-year periods since 1927, relative strength outperforms the CRSP universe 100% of the time. Even in 1-year periods it outperforms 78.6% of the time. As can be seen here, relative strength typically does better in longer periods. While it is obviously possible do poorly in an individual year, by continuing to implement a winning strategy time and time again, the more frequent and/or larger successful years outweigh the bad ones.

Even more importantly, relative strength typically outperforms value investment. Relative strength defeats value in over 57% of periods of all sizes, doing the best in 10-year periods with 69.3% of trials outperforming. While relative strength and value investment strategies have historically both generally beat the market, relative strength has been more consistent in doing so.

21 Comments | Relative Strength and Value, Relative Strength Research | Tagged: historical, investment, over time, performance, relative strength, strategies, value | Permalink

Posted by:

Amanda Schaible