February 21, 2014

That’s the title of a Marketwatch article by mutual fund columnist Chuck Jaffe. I have to admit that usually I like his columns. But columns like this make me nuts! (See also The $ Value of Patience for an earlier rant on a similar topic.)

Here’s the thesis in a nutshell:

…safe driving comes down to a mix of equipment and personnel.

The same can be said for mutual funds and exchange-traded funds, and while there is growing consensus that ETFs are the better vehicle, there’s growing evidence that the people using them may not be so skilled behind the wheel.

The article goes on to point out that newsletters with model portfolios of mutual funds and ETFs have disparate results.

Over the last 12 months, the average model portfolio of traditional funds—as tracked by Hulbert Financial Digest—was up 20.9%, a full three points better than the average ETF portfolio put together by the same advisers and newsletter editors. The discrepancy narrows to two full percentage points over the last decade, and Hulbert noted he was only looking at advisers who run portfolios on both sides of the aisle.

Hulbert posited that if you give one manager both vehicles, the advantages of the better structure should show up in performance.

It didn’t.

Hulbert—who noted that the performance differences are “persistent” — speculated “that ETFs’ advantages are encouraging counterproductive behavior.” Effectively, he bought into Bogle’s argument and suggested that if you give an investor a trading vehicle, they will trade it more often.

Does it make any sense to blame the vehicle for the poor driving? (Not to mention that DALBAR data make it abundantly clear that mutual fund drivers frequently put themselves in the ditch.) Would it make sense to run a headline like “The Growing Case Against Stocks” because stocks can be traded?

Mutual funds, ETFs, and other investment products exist to fulfill specific needs. Obviously not every product is right for every investor, but there are thousands of good products that will help investors meet their goals. When that doesn’t happen, it’s usually investor behavior that’s to blame. (And you’re not under any obligation to invest in a particular product. If you don’t understand it, or you get the sinking feeling that your advisor doesn’t either, you should probably run the other way.)

Investors engage in counterproductive behavior all the time, period. It’s not a matter of encouraging it or not. It happens in every investment vehicle and the problem is almost always the driver. In fact, advisors that can help manage counterproductive investor behavior are worth their weight in gold. We’re not going to solve problems involving investor behavior by blaming the product.

A certain amount of common sense has to be applied to investing, just like it does in any other sphere of life. I know that people try to sue McDonald’s for “making” them fat or put a cup of coffee between their legs and then sue the drive-thru that served it when they get burned, but whose responsibility is that really? We all know the answer to that.

1 Comment |

1 Comment |  From the MM, Investor Behavior, Markets, Media, Thought Process | Tagged: behavioral finance, etf, investor behavior |

From the MM, Investor Behavior, Markets, Media, Thought Process | Tagged: behavioral finance, etf, investor behavior |  Permalink

Permalink

Posted by:

Mike Moody

July 22, 2013

…has been discovered by the Wall Street Journal. Recently, they wrote an article about better ways to index—alternative beta—and referenced a study by Cass Business School. (We wrote about this study here in April.)

Here’s the WSJ’s take on the Cass Business School study:

The Cass Business School researchers examined how 13 alternative index methodologies would have performed for the 1,000 largest U.S. stocks from 1968 to 2011.

All 13 of the alternative indexes produced higher returns than a theoretical market-cap index the researchers created. While the market-cap index generated a 9.4% annualized return over the full period, the other indexes delivered between 9.8% and 11.4%. The market-cap-weighted index was the weakest performer in every decade except the 1990s.

The most interesting part of the article, to me, was the discussion of the growing acceptance of alternative beta. This is truly exciting.

Indeed, a bevy of funds tracking alternative indexes have been launched in recent years. And their popularity is soaring: 43% of inflows into U.S.-listed equity exchange-traded products in the first five months of 2013 went to products that aren’t weighted by market capitalization, up from 20% for all of last year, according to asset manager BlackRock Inc.

And then there was one mystifying thing: although one of the best-performing alternative beta measures is relative strength (“momentum” to academics), relative strength was not mentioned in the WSJ article at all!

Instead there was significant championing of fundamental indexes. Fundamental indexes are obviously a valid form of alternative beta, but I am always amazed how relative strength flies under the radar. (See The #1 Investment Return Factor No One Wants to Talk About.) Indeed, as you can see from the graphic below, the returns of two representative ETFs, PRF and PDP are virtually indistinguishable. One can only hope that relative strength will eventually gets its due.

The performance numbers above are pure price returns, based on the applicable index not inclusive of dividends, fees, commissions, or other expenses. Past performance not indicative of future results. Potential for profits accompanied by possibility of loss. See www.powershares.com for more information.

1 Comment | Portfolio Theory, Relative Strength Research, Thought Process | Tagged: etf, factor investing, momentum, PDP, relative strength | Permalink

Posted by:

Andy Hyer

April 9, 2013

Andy wrote a recent article entitled Smart Beta Gains Momentum. It’s gaining momentum for a good reason! A recent study at Cass Business School in London found that cap-weighting was not a very good way to construct an index. Lots of methods to get exposure to smart beta do better. The results were discussed in an article at Index Universe. Some excerpts:

Researchers have found that equity indices constructed randomly by ‘monkeys’ would produce higher risk-adjusted returns than an equivalent market capitalisation-weighted index over the last 40 years…

The findings come from a recent study by Cass Business School (CBS), which was based on monthly US share data from 1968 to 2011. The authors of the study found that a variety of alternative index weighting schemes all delivered superior returns to the market cap approach.

According to Dr. Nick Motson of CBS, co-author of the study, “all of the 13 alternative indices we studied produced better risk-adjusted returns than a passive exposure to a market-cap weighted index.”

The study included an experiment that saw a computer randomly pick and weight each of the 1,000 stocks in the sample. The process was then repeated 10 million times over each of the 43 years. Clare describes this as “effectively simulating the stock-picking abilities of a monkey”.

…perhaps most shockingly, we found that nearly every one of the 10 million monkey fund managers beat the performance of the market cap-weighted index,” said Clare.

The findings will be a boost to investors already looking at alternative indexing. Last year a number of European pension funds started reviewing their passive investment strategies, switching from capitalisation-weighting to alternative index methodologies.

Relative strength is one of the prominent smart beta methodologies. Of course, cap-weighting has its uses—the turnover is low and rebalancing is minimized. But purely in terms of performance, the researchers at Cass found that there are better ways to do things. Now that ETFs have given investors a way to implement some of these smart beta methods in a tax-efficient, low-cost manner, I suspect we will see more movement toward smart beta in the future.

1 Comment | Portfolio Theory, Thought Process | Tagged: alternative beta, etf, factor investing, portfolio theory, relative strength, return factor, smart beta | Permalink

Posted by:

Mike Moody

September 26, 2012

Exchange traded funds comprise of groups of assets that are traded on the stock exchange. Similarly to mutual funds, ETFs track a basket of securities. This makes them more diversified than a single stock. Yet like stocks, they are easily traded, can be sold short, and often have lower transaction costs than mutual funds. ETFs tend to perform best under a buy-and-hold approach, but has the ease at which they trade caused investors to trade them more? Vanguard set out to answer this question.

They looked at “3.2 million transactions in more than 500,000 positions held in the mutual fund and ETF share classes of four different Vanguard funds from 2007-2011.” While ETFs were traded more often, mutual funds and exchange traded funds still had similar trading patterns.

Some in the investment community have suggested that ETFs tempt investors to increase their trading activity. Given the lack of investor-level analysis supporting or refuting this presumption, we examined the trading behavior of Vanguard investors. We found that, contrary to speculations in the popular media, most investments are held in a prudent, buy-and-hold manner, regardless of share class. Although behavior in ETFs is more active than behavior in traditional mutual funds, some of that difference is simply due to the fact that investors who are inclined to trade choose ETFs, not that investors who choose ETFs are induced to trade. We conclude that the ETF “temptation effect” is not a significant reason for long-term individual investors to avoid using appropriate ETF investments as part of a diversified investment portfolio.

In short, it is investors themselves that are responsible for increased trading of ETFs, not an inherent quality of the funds. Owning exchange traded funds won’t lure a long-term owner toward short-term trading.

2 Comments | Investor Behavior, Markets | Tagged: etf, mutual fund, trade, trend | Permalink

Posted by:

Amanda Schaible

September 12, 2012

Most professionals have noticed the move to ETFs happening, but a recent article at AdvisorOne makes the magnitude of the shift more clear:

Since the beginning of 2012, investors have pulled almost $15 billion from U.S. stock funds, while boosting money put into ETFs by $16 billion, according to industry studies.

In the latest AdvisorBenchmarking report, for example, 54% of advisors say they are likely to increase their use of the ETFs in the near future, with 43% saying they expect their use of ETFs over the next three years to remain the same.

What is the strategic role of ETFs in portfolios? According to the survey, many strategies lie behind ETF implementation. While “core” and “sector” exposures were most common, several other approaches were all within a few points of each other, including: alternatives exposure, directional market positions, factor or asset class exposures and country/region exposure. Clearly, ETFs are providing advisors and investors with attractive options for expressing their views, and that is translating into strong, consistent growth for these vehicles.

AdvisorBenchmarking provided a nice graphic on the strategic uses of ETFs. It’s clear that ETFs are multipurpose vehicles because advisors are using them to meet a lot of different objectives!

Source: AdvisorBenchmarking/AdvisorOne (click on image to enlarge)

According to their survey, only 8% of ETF use is coming from directional market positions—far less than imagined by people who criticize ETF investors as reckless market timers. For the most part, advisors are using ETFs to get exposures that were unavailable before, whether it is to a specific sector, country, or asset class.

Most of the ETFs now available offer passive exposures to various indexes. More interesting to me are the small number of semi-active ETFs that are designed to provide factor exposure in an attempt to generate alpha. Research suggests that combining factor exposures might be a superior way to capture market returns.

The Technical Leaders indexes are constructed to provide exposure to the momentum (relative strength) factor and there are a couple of low-volatility ETFs around as well. There are a few ETFs explicitly designed for value exposure, although I don’t think this area has been well-exploited yet. (I’m sorry to see Russell close down their suite of ETFs, which I thought had a lot of promise.)

With more and more options available to advisors, I would not be surprised to see ETF use continue to surge.

Comments Off on Advisors Turning to ETFs | Markets, Thought Process | Tagged: etf, ETFs, factor investing, momentum, relative strength, return factors | Permalink

Posted by:

Mike Moody

September 4, 2012

This just in from Institutional Investor: many backtests fail in real life. They write:

Makers of indexes often fill in the blanks with historic data on the components to produce hypothetical index performance. But a recent Vanguard study found that a large percentage of these hypothetical, back-filled indexes that had outperformed the U.S. stock market didn’t keep up after they went live as the index returns subsequently fell. What may be happening, says senior Vanguard ETF strategist Joel Dickson, is that indexes are being developed by “rearview mirror investing,” that is, through selection bias of what worked well in the past. The result can mean a nasty surprise for investors.

Duh.

Pretty much anyone can do data mining with the computing power available on a desktop computer. And index providers will continue to do data mining as long as investors ram money into products with lousy backtests.

Back-filled index funds attract on average twice the cash flow in the initial launch phase than funds with new indexes that don’t have such data, indicating that the availability of a track record makes the fund more attractive — even if it probably won’t last.

Good backtesting can be very useful and can give investors a good idea of what to expect in the future. But how can an investor tell if the backtest is any good or not?

One thing to examine is how robust the index methodology is. For example, when we built our Systematic Relative Strength products, we subjected them to Monte Carlo testing for robustness. That made it apparent that the systematic investment method itself was sound, even though the range of outcomes on a quarterly or annual basis can be significant.

With the proliferation of indexes for ETFs, it’s becoming important to be able to evaluate how robust the backtesting was. Probably partly because of a robust backtesting process, our Technical Leaders Index has outperformed the market since inception. I’m sure many other indexes are thoughtfully constructed—but I’m just as sure that there are some that are not.

Do your homework before you put client money at risk.

See www.powershares.com for more information. Past performance is no guarantee of future returns. A list of all holding for the previous 12 months is available upon request.

Comments Off on Fun With Backtesting | Investor Behavior, Markets, Relative Strength Research | Tagged: backtesting, data mining, etf, monte carlo testing, PDP, relative strength, systematic investment process | Permalink

Posted by:

Mike Moody

August 30, 2012

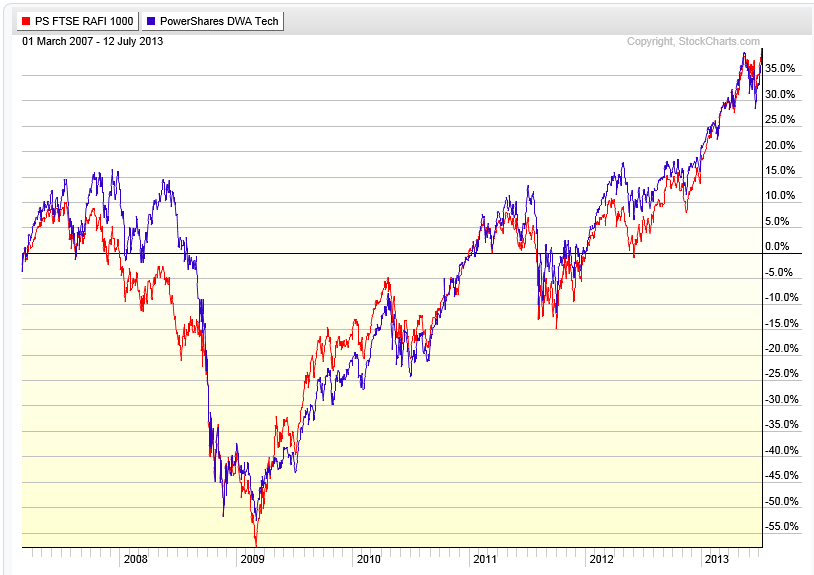

So far, 2012 has been an excellent year for the PowerShares DWA Technical Leaders Index (PDP). Year-to-date, PDP is +14.94%, while the S&P; 500 is +12.16%. PDP, which began trading on March 1, 2007, is a big source of pride for our firm as it has outperformed its benchmark in every year since its inception except for one. For those unfamiliar with the strategy, the index is comprised of 100 high relative strength stocks and is reconstituted on a quarterly basis.

In every quarterly reconstitution there are stocks that come and stocks that go. Those that retain their strong relative strength stay, and those that have deteriorated are replaced. Interestingly, there are a number of stocks that have remained in the index since its inception over five years ago, including Apple Computer.

As shown above, the S&P; 500 (red line) has gone nowhere, while Apple Computer (blue line) has powered higher. Apple is currently the biggest weight in the index:

Obviously, not all of our holdings work out as well as Apple. However, capturing a few of these big winners can make a big difference.

As we announced just a short time ago, our Technical Leaders Index family was recently expanded to include DWAS, the PowerShares DWA Small-Cap Technical Leaders Index. Now, it is a family of four: PDP, PIE, PIZ, and DWAS.

See www.powershares.com for more information. Past performance is no guarantee of future returns. A list of all holdings for the last 12 months is available upon request.

Comments Off on Checking In On PDP | Markets | Tagged: etf, PDP, powershares, relative strength | Permalink

Posted by:

Andy Hyer

August 29, 2012

Chuck Jaffe wrote a nice article for Marketwatch, pointing out that fund investors are actually more intelligent than they are given credit for. It’s worth pointing out because nearly every change in the industry is greeted with skepticism by the pessimists. His article ends with a nice summary:

“The knee-jerk reaction to almost all of the advances we have seen has been ‘Oh my goodness, what is going to happen to the industry?’ and ‘Investors will blow themselves up with this,’” said Geoff Bobroff of Bobroff Consulting, a leading fund industry observer. “Surprise, surprise, the world hasn’t come to an end yet and, in fact, the fund world has gotten better for each of these developments.

“Joe Six-Pack is going to do exactly what he has always done,” Bobroff added. “He is not going to change, just because the technology exists for him to do something different. He will adapt, and over time become comfortable with the newer products and newer ways. That doesn’t mean he will always make money; the market won’t always work for Joe Six-Pack, but that won’t be because the fund industry is evolving, it will be because that’s just what the way the market is sometimes.”

The article addresses the concern expressed by many that investors will blow themselves up with ETFs because of their daily liquidity. (John Bogle has expressed this view frequently and loudly.) Mr. Jaffe pulls out some data from a Vanguard (!) study that shows, in fact, that’s not how investors are acting.

Over the years, we’ve heard the same refrain about tactical asset allocation: investors will never be able to get it right, they’ll blow themselves up chasing performance, etc., etc. In fact, tactical allocation funds have acquitted themselves quite nicely over the past few years in a very difficult market environment. For the most part, they’ve behaved pretty much as advertised—better than the worst asset classes, and not as well as the best asset classes—somewhere in the middle of the pack. That kind of consistency, over time, can lead to reasonable returns with moderate volatility.

Reasonable returns with moderate volatility is a laudable goal, which probably explains why hybrid funds have seen new assets this year, even as equity funds are seeing outflows.

In markets, pessimism is almost never the way to go. It’s more productive to be optimistic and to try to find investment strategies that will work for you over the long run.

3 Comments | Investor Behavior, Markets, Tactical Asset Alloc, Thought Process | Tagged: etf, innovation, investor behavior, stock market, Tactical Asset Allocation | Permalink

Posted by:

Mike Moody

August 16, 2012

Let’s face it; investors often make bad investment decisions. Commonly, this is due to our emotions getting in the way. BlackRock lists some of the emotional investment tendencies that often cloud our judgment and steer us toward poor decisions:

- Anchoring: Holding onto a reference point, even if it’s irrelevant. For example, a $1.5 million house, being presented on its own, might sound expensive. But if you were first shown a $2 million house, and afterwards shown the $1.5 million house, it might then sound like a good deal.

- Herding: Following the crowd. People often pile into the markets when they are doing well and they see “everyone else” doing it.

- Mental Accounting: Separating money into buckets that are treated differently. Earmarking funds for college savings or a vacation home allows you to save for specific goals. But treating those dollars differently may not make sense when they all have the same buying power.

- Framing: Making a different decision based on context. In a research study, when a four-ounce glass had 2 ounces of water poured out of it, 69% of people said it was now “half empty.” If the same glass starts out empty and has 2 ounces of water poured into it, 88% of people say it is “half full.”

Emotional investment tendencies can result in all sorts of problems. Typically these behaviors are so ingrained that we don’t even recognize them as irrational!

One way to combat our emotions is to hire a good advisor. As explained in this previous blog post, one important benefit—maybe even the primary benefit—of having a good advisor is behavior modification. An advisor persuading a client to invest more when the market is doing poorly, instead taking money out, is extremely valuable.

Another option is to invest in a managed product like an ETF or mutual fund (here are some of ours) that will make the decisions for you. For an emotional investor, this may be an easier (and presumably safer) option than picking and obsessively monitoring a few random stocks. Even then, it is important try to avoid the herd mentality. Data shows that it’s most important to avoid panic at market bottoms. Although it is difficult not to panic if other people around you are fearful, the potential difference in your investment return can be significant.

In short, understanding your emotional tendencies may help keep them from interfering in investment decisions. If that isn’t enough, try enlisting the help of an outside source. With the steady hand of a good advisor, it may be possible to mitigate emotional investment tendencies.

2 Comments | Investor Behavior, Markets | Tagged: advice, advisor, etf, investment, investor behavior, mental accounting, personal finance | Permalink

Posted by:

Amanda Schaible

July 25, 2012

We’ve just released a small-cap ETF with PowerShares (DWAS), which is the first U.S. relative strength small-cap ETF. We’ve done our own testing, of course, but it might also be instructive to take a look at other small-cap relative strength returns. Once again, we used the Ken French data library to calculate annualized returns and standard deviation. The construction of their relative strength index is explained here. The difference this time around is that we used small-cap stocks instead of large-cap stocks. Generally speaking, a small-cap stock is one whose price times number of outstanding shares (market capitalization) is between $300 million and $2 billion. However, the Ken French data used also includes micro-cap stocks which have an even smaller market capitalization (typically between $50-$300 million). Market cap is above $10 billion for large-cap stocks.

In the past, small-cap stocks have yielded high returns. They often perform well because companies in early stages of development have large growth potential. However, the potential of high earnings also comes with high risk. Small-cap companies face limited reserves, which make them more vulnerable than larger ones. Furthermore, in order to grow, they need to be able to replicate their business model on a bigger scale.

This is the sort of tradeoff investors must think about when choosing how to structure their portfolio. Typical factor models suggest that there are excess returns to be had in areas like value, relative strength, and small-cap, often at the cost of a little extra volatility. If you’re willing to take on more risk for the chance of higher returns, a portfolio that combines relative strength with small-cap stocks might be a good place to look!

Comments Off on Small-Cap Relative Strength Performance | Relative Strength Research | Tagged: cap, capitalization, etf, large, large cap, market, relative strength, small | Permalink

Posted by:

Amanda Schaible

June 26, 2012

Bloomberg has an article today entitled “ETFs Passive No More.” It’s an article about the rise of intelligent indexation. Here’s their thesis:

Exchange-traded funds are posing a new threat to the $7.8 trillion market for active mutual funds by challenging the notion ETFs are only good for tracking benchmarks.

Here’s their blurb about PDP:

The PowerShares DWA fund, which invests in U.S.-listed companies, uses an index that selects them based on “relative strength,” a proprietary screening methodology developed by Richmond, Virginia-based Dorsey, Wright & Associates Inc. The fund has advanced at an annual rate of 2 percent since its inception in March 2007, compared with the 1.2 percent gain for the Standard & Poor’s 500 Index over the same period, and the 3.8 percent increase in the Russell 3000 Growth Index.

Their offerings may further erode the market share of active mutual funds, sold by traditional money managers such as Fidelity Investments, Capital Group Cos. and Franklin Resources Inc. The companies tout the ability of their managers to beat benchmarks mostly through individual security selection.

“Historically, active managers held a unique appeal to prospective investors,” said Steven Bloom, who helped develop the first ETF in the 1980s and is now an assistant professor of economics at the U.S. Military Academy at West Point, New York.“Now, ETFs are infringing on that territory by holding out the prospect of alpha.”

The article points out that by using a rules-based investment process within an ETF, you can shoot for alpha, while getting the tax benefits of the ETF structure. Rules-based ETFs are going to continue to blur the line with active mutual funds over time. It’s also going to be interesting to see how many of the rules-based processes are robust and how many have been optimized. Curve-fitted performance will tend to degrade over time, while a truly adaptive model should be more consistent.

We think the trend toward intelligent indexes will continue and we’re excited to be one of the pioneers.

See www.powershares.com for more information about PDP. Past performance is no guarantee of future returns. A list of all holdings for the trailing 12 months is available upon request.

Comments Off on PDP in the News | From the MM, Media, Thought Process | Tagged: etf, PDP, relative strength, rules-based, systematic investment process, Technical Leaders | Permalink

Posted by:

Mike Moody

June 19, 2012

Investment News reports that assets in model ETF portfolios tracked by Morningstar Inc. grew to $46 billion by the end of the first quarter, up 43% from a year earlier.

The growing popularity of exchange-traded funds has led to a boom among money managers who specialize in using low-cost passive investments to build go-anywhere portfolios.

These model ETF portfolios typically use ETFs to invest globally across all asset classes, such as equities, fixed income and commodities, to shoot for a real return.

Financial advisers increasingly are outsourcing some of their client assets to these managers so that they can spend more time on clients and less time managing portfolios.

“As the ETF landscape has gotten more complicated, not all advisers feel comfortable building their own portfolios,” said Sue Thompson, head of iShares’ RIA Group. “Advisers have to either be the expert or find one.”

Managing go-anywhere portfolios is near and dear to our hearts here at Dorsey Wright. Click here to view a video presentation on our Global Macro portfolio, which has become our most widely used separate account strategy.

To receive the brochure for our Global Macro strategy, click here. For information about the Arrow DWA Tactical Fund (DWTFX), click here.

Click here and here for disclosures. Past performance is no guarantee of future returns.

2 Comments | Markets, Tactical Asset Alloc | Tagged: etf, exchange traded fund, investment, portfolio | Permalink

Posted by:

Andy Hyer

May 15, 2012

ETFdb describes the growing ETF universe as follows:

At times, it seems as if the number of ETFs available to U.S. investors will soon exceed the number of stars in the sky. That might be overstating things a bit, but the pace of expansion in the ETF industry has truly been impressive over the last several years. With multiple products seemingly debuting every week and very few shutting down (despite countless predictions to the contrary), the size of the ETF lineup has effectively doubled in a relatively short period of time. And there’s no indication that the product development front is going to be slowing down any time soon; issuers continue to file for both innovative and duplicative products, producing a pipeline full of hundreds of funds that could debut at some point in the next several months.

The proliferation of ETFs, ETNs, and other exchange-traded cousins of these vehicles is, in many ways, a very positive development for investors. There are now ETPs for just about every investment objective, ranging from the very broad and very straightforward to the hyper-targeted and rather complex. And many of the more recent additions to the ETF lineup have further “democratized” the business of investing, delivering cheap and easy access to sophisticated strategies that would otherwise be time consuming and expensive to implement.

My emphasis added. Up to this point, I wholeheartedly agree–the expansion of the ETF universe has been extremely beneficial to investors. It has also played right into our hands here at Dorsey Wright because it has provided a very tax-efficient means of getting exposure to relative strength (See PDP, PIE, and PIZ). Furthermore, the expansion of the ETF universe has enabled us to provide innovative global tactical asset allocation strategies (See DWAFX and DWTFX) where we can efficiently get exposure to a wide variety of global asset classes.

However, ETFdb then states the following:

But the growth spurt for the industry has also made it increasingly difficult to navigate. Moreover, the tremendous variance in level of sophistication and risk tolerance among ETFs can set the stage for confusion and potentially lead to a less-than-ideal experience with ETFs.

That last part is only true if there is no framework for efficiently and thoroughly evaluating each of the ETFs. Without such a framework then, yes, I can certainly understand why some find it “increasingly difficult to navigate.” However, within the context of a relative strength model, more choices are potentially a good thing. The more options for finding uncorrelated returns, the more likely it is that a global tactical asset allocation strategy can generate favorable returns in a variety of market environments. Furthermore, relative strength models evaluate each member of the universe in a systematic fashion and only allocate if dictated by the relative strength rank–a true meritocracy!

Source: Wikipedia

See www.powershares.com and www.arrowfunds.com.

1 Comment | Markets, Tactical Asset Alloc | Tagged: arrowfunds, etf, exchange traded funds, powershares | Permalink

Posted by:

Andy Hyer