March 2, 2014

Investor behavior has a lot to do with how markets behave, and with how investors perform. To profit from a long mega-bull market, investors have to be willing to buy stocks and hold them through the inevitable ups and downs along the way. Risk tolerance greatly influences their willing to do that—and risk tolerance is greatly influenced by their past experience.

From an article on risk in The Economist:

People’s financial history has a strong impact on their taste for risk. Looking at surveys of American household finances from 1960 to 2007, Ulrike Malmendier of the University of California at Berkeley and Stefan Nagel, now at the University of Michigan, found that people who experienced high returns on the stockmarket earlier in life were, years later, likelier to report a higher tolerance for risk, to own shares and to invest a bigger slice of their assets in shares.

But exposure to economic turmoil appears to dampen people’s appetite for risk irrespective of their personal financial losses. That is the conclusion of a paper by Samuli Knüpfer of London Business School and two co-authors. In the early 1990s a severe recession caused Finland’s GDP to sink by 10% and unemployment to soar from 3% to 16%. Using detailed data on tax, unemployment and military conscription, the authors were able to analyse the investment choices of those affected by Finland’s “Great Depression”. Controlling for age, education, gender and marital status, they found that those in occupations, industries and regions hit harder by unemployment were less likely to own stocks a decade later. Individuals’ personal misfortunes, however, could explain at most half of the variation in stock ownership, the authors reckon. They attribute the remainder to “changes in beliefs and preferences” that are not easily measured.

The same seems to be true for financial trauma. Luigi Guiso of the Einaudi Institute for Economics and Finance and two co-authors examined the investments of several hundred clients of a large Italian bank in 2007 and again in 2009 (ie, before and after the plunge in global stockmarkets). The authors also asked the clients about their attitudes towards risk and got them to play a game modelled on a television show in which they could either pocket a small but guaranteed prize or gamble on winning a bigger one. Risk aversion, by these measures, rose sharply after the crash, even among investors who had suffered no losses in the stockmarket. The reaction to the financial crisis, the authors conclude, looked less like a proportionate response to the losses suffered and “more like old-fashioned ‘panic’.”

I’ve bolded a couple of sections that I think are particularly interesting. Investors who came of age in the 1930s tended to have an aversion to stocks also—an aversion that caused them to miss the next mega-bull market in the 1950s. Today’s investors may be similarly traumatized, having just lived through two bear markets in the last decade or so.

Bull markets climb a wall of worry and today’s prospective investors are plenty worried. Evidence of this is how quickly risk-averse bond-buying picks up during even small corrections in the stock market. If history is any guide, investors could be overly cautious for a very long time.

Of course, I don’t know whether we’re going to have a mega-bull market for the next ten or fifteen years or not. Anything can happen. But it wouldn’t surprise me if the stock market does very well going forward—and it would surprise me even less if most investors miss out.

Comments Off on The Coming Mega-Bull Market? |

Comments Off on The Coming Mega-Bull Market? |  From the MM, Investor Behavior, Markets | Tagged: behavioral finance, decision-making, equities, investor behavior, mega-bull market, stock market |

From the MM, Investor Behavior, Markets | Tagged: behavioral finance, decision-making, equities, investor behavior, mega-bull market, stock market |  Permalink

Permalink

Posted by:

Mike Moody

February 27, 2014

Morgan Housel at Motley Fool has a wonderful article on how investors can learn from failure. He sets the tone with a few different quotes and anecdotes that point out that a lot of being a success is just avoiding really dumb mistakes.

At a conference years ago, a young teen asked Charlie Munger how to succeed in life. “Don’t do cocaine, don’t race trains to the track, and avoid all AIDS situations,” Munger said. Which is to say: Success is less about making great decisions and more about avoiding really bad ones.

People focus on role models; it is more effective to find antimodels—people you don’t want to resemble when you grow up. Nassim Taleb

I’ve added the emphasis, but Mr. Housel makes a good point. Learning from failure is equally important as learning from success. In fact, he argues it may be more important.

If it were up to me, I would replace every book called How to Invest Like Warren Buffett with a one called How to Not Invest Like Lehman Brothers, Long-Term Capital Management, and Jesse Livermore. There are so many lessons to learn from these failed investors about situations most of us will face, like how quickly debt can ruin you. I’m a fan of learning from Buffett, but the truth is most of us can’t devote as much time to investing as he can. The biggest risk you face as an investor isn’t that you’ll fail to be Warren Buffett; it’s that you’ll end up as Lehman Brothers.

But there’s no rule that says you have to learn by failing yourself. It is far better to learn vicariously from other people’s mistakes than suffer through them on your own.

That’s his thesis in a nutshell. He offers three tidbits from his study of investing failures. I’ve quoted him in full here because I think his context is important (and the writing is really good).

1. The overwhelming majority of financial problems are caused by debt, impatience, and insecurity. People want to fit in and impress other people, and they want it right now. So they borrow money to live a lifestyle they can’t afford. Then they hit the inevitable speed bump, and they find themselves over their heads and out of control. That simple story sums up most financial problems in the world. Stop trying to impress people who don’t care about you anyways, spend less than you earn, and invest the rest for the long run. You’ll beat 99% of people financially.

2. Complexity kills. You can make a lot of money in finance, so the industry attracted some really brilliant people. Those brilliant people naturally tried to make finance more like their native fields of physics, math, and engineering, so finance has grown exponentially more complex in the last two decades. For most, that’s been a disservice. I think the evidence is overwhelming that simple investments like index funds and common stocks will demolish complicated ones like derivatives and leveraged ETFs. There are two big stories in the news this morning: One is about how the University of California system is losing more than $100 million on a complicated interest rate swap trade. The other is about how Warren Buffett quintupled his money buying a farm in Nebraska. Simple investments usually win.

3. So does panic. In his book Deep Survival, Laurence Gonzalez chronicles how some people managed to survive plane crashes, getting stranded on boats, and being stuck in blizzards while their peers perished. The common denominator is simple: The survivors didn’t panic. It’s the same in investing. I’ve seen people make a lifetime of good financial decisions only to blow it all during a market panic like we saw in 2008. Any financial decision you make with an elevated heart rate is probably going to be one you’ll regret. Napoleon’s definition of a military genius was “the man who can do the average thing when all those around him are going crazy.” It’s the same in investing.

I think these are really good points. It’s true that uncontrolled leverage accompanies most real blowups. Having patience in the investing process is indeed necessary; we’ve written about that a lot here too. The panic, impatience, and insecurity he references are really all behavioral issues—and it just points out that having your head on straight is incredibly important to investment success. How successful you are in your profession or how much higher math you know is immaterial. As Adam Smith (George Goodman) wrote, “If you don’t know who you are, the stock market is an expensive place to find out.”

Mr. Housel’s point on complexity could be a book in itself. Successful investing just entails owning productive assets—the equity and debt of successful enterprises—acquired at a reasonable price. Whether you own the equity directly, like Warren Buffett and his farm, or in security form is immaterial. An enterprise can be a company—or even a country—but it’s got to be successful.

Complexity doesn’t help with this evaluation. In fact, complexity often obscures the whole point of the exercise.

This is actually one place where I think relative strength can be very helpful in the investment process. Relative strength is incredibly simple and relative strength is a pretty good signaling mechanism for what is successful. Importantly, it’s also adaptive: when something is no longer successful, relative strength can signal that too. Sears was once the king of retailing. Upstart princes like K-Mart in its day, and Wal-Mart and Costco later, put an end to its dominance. Once, homes were lit with candles and heated with fuel oil. Now, electricity is much more common—but tomorrow it may be something different. No asset is forever, not even Warren Buffett’s farmland. When the soil is depleted, that farm will become a lead anchor too. Systematic application of relative strength, whether it’s being used within an asset class or across asset classes, can be a very useful tool to assess long-term success of an enterprise.

Most investing problems boil down to behavioral issues. Impatience and panic are a couple of the most costly. Avoiding complexity is a different dimension that Mr. Housel brings up, and one that I think should be included in the discussion. There are plenty of millionaires that have been created through owning businesses, securities, or real estate. I can’t think of many interest rate swap millionaires (unless you count the people selling them). Staying calm and keeping things simple might be the way to go. And if the positive prescription doesn’t do it for you, the best way to be a good investor may be to avoid being a terrible investor!

8 Comments | From the MM, Investor Behavior, Markets, Thought Process | Tagged: behavioral finance, decision-making, investor behavior, relative strength, stock market, systematic investment process, warren buffett | Permalink

Posted by:

Mike Moody

February 21, 2014

That’s the title of a Marketwatch article by mutual fund columnist Chuck Jaffe. I have to admit that usually I like his columns. But columns like this make me nuts! (See also The $ Value of Patience for an earlier rant on a similar topic.)

Here’s the thesis in a nutshell:

…safe driving comes down to a mix of equipment and personnel.

The same can be said for mutual funds and exchange-traded funds, and while there is growing consensus that ETFs are the better vehicle, there’s growing evidence that the people using them may not be so skilled behind the wheel.

The article goes on to point out that newsletters with model portfolios of mutual funds and ETFs have disparate results.

Over the last 12 months, the average model portfolio of traditional funds—as tracked by Hulbert Financial Digest—was up 20.9%, a full three points better than the average ETF portfolio put together by the same advisers and newsletter editors. The discrepancy narrows to two full percentage points over the last decade, and Hulbert noted he was only looking at advisers who run portfolios on both sides of the aisle.

Hulbert posited that if you give one manager both vehicles, the advantages of the better structure should show up in performance.

It didn’t.

Hulbert—who noted that the performance differences are “persistent” — speculated “that ETFs’ advantages are encouraging counterproductive behavior.” Effectively, he bought into Bogle’s argument and suggested that if you give an investor a trading vehicle, they will trade it more often.

Does it make any sense to blame the vehicle for the poor driving? (Not to mention that DALBAR data make it abundantly clear that mutual fund drivers frequently put themselves in the ditch.) Would it make sense to run a headline like “The Growing Case Against Stocks” because stocks can be traded?

Mutual funds, ETFs, and other investment products exist to fulfill specific needs. Obviously not every product is right for every investor, but there are thousands of good products that will help investors meet their goals. When that doesn’t happen, it’s usually investor behavior that’s to blame. (And you’re not under any obligation to invest in a particular product. If you don’t understand it, or you get the sinking feeling that your advisor doesn’t either, you should probably run the other way.)

Investors engage in counterproductive behavior all the time, period. It’s not a matter of encouraging it or not. It happens in every investment vehicle and the problem is almost always the driver. In fact, advisors that can help manage counterproductive investor behavior are worth their weight in gold. We’re not going to solve problems involving investor behavior by blaming the product.

A certain amount of common sense has to be applied to investing, just like it does in any other sphere of life. I know that people try to sue McDonald’s for “making” them fat or put a cup of coffee between their legs and then sue the drive-thru that served it when they get burned, but whose responsibility is that really? We all know the answer to that.

1 Comment | From the MM, Investor Behavior, Markets, Media, Thought Process | Tagged: behavioral finance, etf, investor behavior | Permalink

Posted by:

Mike Moody

January 6, 2014

“The 1%” phrase has been used a lot to decry income inequality, but I’m using it here in an entirely different context. I’m thinking about the 1% in relation to a recent article by Motley Fool’s Morgan Housel. Here’s an excerpt from his article:

Building wealth over a lifetime doesn’t require a lifetime of superior skill. It requires pretty mediocre skills — basic arithmetic and a grasp of investing fundamentals — practiced consistently throughout your entire lifetime, especially during times of mania and panic. Most of what matters as a long-term investor is how you behave during the 1% of the time everyone else is losing their cool.

That puts a little different spin on it. Maybe your behavior during 1% of the time is how you get to be part of the 1%. (The bold in Mr. Housel’s quotation above is mine.)

In his article, Housel demonstrates how consistency—in this case, dollar-cost averaging—beats a couple of risk avoiders who try to miss recessions. We’ve harped on having some kind of systematic investment process here, so consistency is certainly a big part of success.

But also consider what might happen if you can capitalize on those periods of panic and add to your holdings. Imagine that kind of program practiced consistently over a lifetime! Warren Buffett’s article in the New York Times, “Buy American. I Am.” from October 2008 comes to mind. Here is a brief excerpt of Mr. Buffett’s thinking during the financial crisis:

THE financial world is a mess, both in the United States and abroad. Its problems, moreover, have been leaking into the general economy, and the leaks are now turning into a gusher. In the near term, unemployment will rise, business activity will falter and headlines will continue to be scary.

So … I’ve been buying American stocks.

If prices keep looking attractive, my non-Berkshire net worth will soon be 100 percent in United States equities.

A simple rule dictates my buying: Be fearful when others are greedy, and be greedy when others are fearful. And most certainly, fear is now widespread, gripping even seasoned investors. To be sure, investors are right to be wary of highly leveraged entities or businesses in weak competitive positions. But fears regarding the long-term prosperity of the nation’s many sound companies make no sense. These businesses will indeed suffer earnings hiccups, as they always have. But most major companies will be setting new profit records 5, 10 and 20 years from now.

Let me be clear on one point: I can’t predict the short-term movements of the stock market. I haven’t the faintest idea as to whether stocks will be higher or lower a month — or a year — from now. What is likely, however, is that the market will move higher, perhaps substantially so, well before either sentiment or the economy turns up. So if you wait for the robins, spring will be over.

Gee, I wonder how that worked out for him? It’s no mystery why Warren Buffett has $60 billion—he is as skilled a psychological arbitrageur as there is and he has been at it for a very long time.

As Mr. Housel points out, even with mediocre investing skills, just consistency can go a long way toward building wealth—and the ability to be greedy when others are fearful has the potential to compound success.

2 Comments | Investor Behavior, Markets, Portfolio Theory, Thought Process | Tagged: behavioral finance, decision-making, investor behavior, warren buffett | Permalink

Posted by:

Mike Moody

January 6, 2014

Marshall Jaffe, in a recent article for ThinkAdvisor, made an outstanding observation:

In a world where almost nothing can be predicted with any accuracy, investor behavior is one of the rare exceptions. You can take it to the bank that investors will continue to be driven by impatience, social conformity, conventional wisdom, fear, greed and a confusion of volatility with risk. By standing apart and being driven solely by the facts, the value investor can take advantage of the opportunities caused by those behaviors—and be in the optimal position to create and preserve wealth.

His article was focused on value investing, but I think it is equally applicable to relative strength investing. In fact, maybe even more so, as value investors often differ about what they consider a good value, while relative strength is just a mathematical calculation with little room for interpretation.

Mr. Jaffe’s main point—that investors are driven by all sorts of irrational and incorrect cognitive forces—is quite valid. Dozens of studies point it out and there is a shocking lack of studies (i.e., none!) that show the average investor to be a patient, independent thinker devoid of fear and greed.

What’s the best way to take advantage of this observation about investor behavior? I think salvation may lie in using a systematic investment process. If you start with an investment methodology likely to outperform over time, like relative strength or value, and construct a rules-based systematic process to follow for entry and exit, you’ve got a decent chance to avoid some of the cognitive errors that will assail everyone else.

Of course, you will construct your rules during a period of calm and contemplation—but that’s never when rules are difficult to apply! The real test is sticking to your rules during the periods of fear and greed that occur routinely in financial markets. Devising the rules may be relatively simple, but following them in trying circumstances never is! As with most things, the harder it is to do, the bigger the potential payoff usually is.

39 Comments | Investor Behavior, Markets, Portfolio Theory, Thought Process | Tagged: investor behavior, systematic investment process | Permalink

Posted by:

Mike Moody

December 2, 2013

“I can’t buy now—the stock market is at all-time highs.” I’ve heard that, or some version of it, from multiple clients in the last few weeks. I understand where clients are coming from. Their past experience involves waiting too long to buy and then getting walloped. That’s because clients often wait for the bubble phase to invest. Not only is the stock market at all-time highs, but valuations tend to be stretched as well.

Here’s the thing: buying at all-time highs really doesn’t contain much information about whether you are making an investing mistake or not.

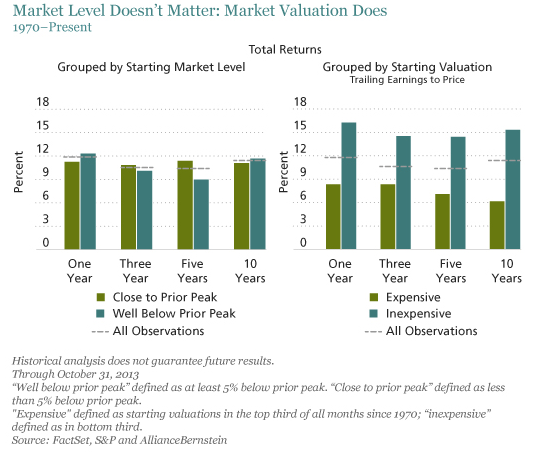

For proof, I will turn to a nice piece in Advisor Perspectives penned by Alliance Bernstein. Here’s what they have to say:

With the US stock market repeatedly reaching all-time highs in recent weeks, many investors are becoming leery of investing in stocks. Focusing on the market’s level is a mistake, in our view. It’s market valuation, not level, that matters.

Since 1900, the S&P; 500 Index has been close to (within 5%) of its prior peak almost half the time. There’s a simple reason for this. The stock market goes up over time, along with the economy and corporate earnings.

Fear of investing at market peaks is understandable. In the short term, there’s always the risk that other investors will decide to take gains, or that geopolitical, economic or company-specific news will trigger a market pullback.

But for longer-term investors, market level has no predictive power. Market valuation—not market level—is what historically has mattered to future returns.

They have a nice graphic to show that investing near the high—or not near the high—is inconsequential. They show that future returns are much more correlated to valuation.

Source: Advisor Perspective (click on image to enlarge)

I’m no fundamental analyst, but commentators from Warren Buffett to Ed Yardeni to Howard Marks have suggested that valuations are reasonable, although slightly higher than average. There’s obviously no guarantee that stocks will go up, but you are probably not tap dancing on a landmine. Or let’s put it this way: if the stock market goes down from here, it won’t be because we are at all-time highs. The trend is your friend until it ends.

30 Comments | Investor Behavior, Markets, Thought Process | Tagged: behavioral finance, equities, investor behavior, stock market | Permalink

Posted by:

Mike Moody

November 4, 2013

Good portfolio management is difficult, while poor portfolio management is almost effortless! In the spirit of David Letterman’s Top Ten list, here is my contribution to the genre of things to avoid, with a special nod to our brand of investing. I made a version of this presentation originally at a 1996 Dorsey Wright Broker Institute.

THE TOP TEN WAYS TO SABOTAGE YOUR PORTFOLIO

1. BE ARROGANT. Assume your competition is lazy and stupid. Don’t do your homework and don’t bother with a game plan. Panic if things don’t go well.

2. WHEN A SECTOR OR THE MARKET REVERSES UP, WAIT UNTIL YOU FEEL COMFORTABLE TO BUY. This is an ideal method for catching stocks 10 points higher.

3. BE AFRAID TO BUY STRONG STOCKS. This way you can avoid the big long-term relative strength winners.

4. SELL A STOCK ONLY BECAUSE IT HAS GONE UP. This is an excellent way to cut your profits short. (If you can’t stand prosperity, trim if you must, but don’t sell it all.)

5. BUY STOCKS IN SECTORS THAT ARE SUPER EXTENDED BECAUSE IT’S DIFFERENT THIS TIME. Not.

6. TRY TO BOTTOMFISH A STOCK IN A DOWNTREND. Instead, jump off a building and try to stop 5 floors before you hit the ground. Ouch.

7. BUY A STOCK ONLY BECAUSE IT’S A GOOD VALUE. There are two problems with this. 1) It can stay a good value by not moving for the next decade, or worse 2) it can become an even better value by dropping another 10 points.

8. HOLD ON TO LOSING STOCKS AND HOPE THEY COME BACK. An outstanding way to let your losses run. Combined with cutting your profits short, over time you can construct a diversified portfolio of losers and register it with the Kennel Club.

9. PURSUE PERFECTION. There are two diseases. 1) Hunting for the perfect method. Trying a new “system” each week will not get you to your goal. It requires remaining focused on one method, maintaining consistency and discipline, and making incremental improvements. 2) Waiting for the perfect trade. The sector is right, the market is supporting higher prices, the chart is good—try to buy it a point cheaper and miss it entirely. Doh. Better to be approximately right than precisely wrong.

10. MAKE INVESTMENT DECISIONS BASED ON A MAGAZINE COVER, MEDIA ARTICLES, OR PUNDITS. Take investment advice from a journalist or a hedge fund manager talking his book! Get fully engaged with your emotions of fear and greed! This is the method of choice for those interested in the fastest route to the poorhouse.

3 Comments | Investor Behavior, Just for Fun, Markets, Thought Process | Tagged: behavioral finance, decision-making, investor behavior, market, stock market | Permalink

Posted by:

Mike Moody

October 9, 2013

Investors—or people generally—find it difficult to think in terms of probability. A quote from a recent ThinkAdvisor article on probability is instructive:

In multiple studies (most prominently those by Edwards and Estes, as reported by Philip Tetlock in his book Expert Political Judgment), subjects were asked to predict which side of a “T-maze” held food for a rat. The maze was rigged such that the food was randomly placed (no pattern), but 60% of the time on one side and 40% on the other. The rat quickly “gets it” and waits at the “60% side” every time and is thus correct 60% of the time. Human observers keep looking for patterns and choose sides in rough proportion to recent results. As a consequence, the humans were right only 52% of the time—they (we!) are much dumber than rats. We routinely misinterpret probabilistic strategies that accept the inevitability of randomness and error.

Even rats get probability better than people! It is for this reason that a systematic investing process can be so valuable. Away from the pressure and hubbub of the markets, strategies can be researched and probabilities investigated and calculated. Decisions can be made on the basis of probability because a systematic process incorporates the notion that there is a certain amount of randomness that cannot be overcome with clever decision-making.

Ironically, because humans have sophisticated pattern recognition skills built in, we see patterns in probability where there are none. A systematic investment process can reduce or eliminate the “overinterpretation” inherent in our own cleverness. When we can base our decisions only on the actual probabilities embedded in the data, those decisions will be much better over a large number of trials.

Good investing is never easy, but a systematic investing process can eliminate at least one barrier to good performance.

31 Comments | Investor Behavior, Markets, Thought Process | Tagged: behavioral finance, decision-making, investor behavior, systematic investment process | Permalink

Posted by:

Mike Moody

October 7, 2013

John Rekenthaler at Morningstar, who usually has some pretty smart stuff to say, took on the topic of smart beta in a recent article. Specifically, he examined a variety of smart beta factors with an eye to determining which ones were real and might persist. He also thought some factors might be fool’s gold.

Here’s what he had to say about value:

The value premium has long been known and continues to persist.

And here’s what he had to say about relative strength (momentum):

I have trouble seeing how momentum can succeed now that its existence is well documented.

The italics are mine. I didn’t take logic in college, but it seems disingenuous to argue that one factor will continue to work after it is well-known, while becoming well-known will cause the other factor to fail! (If you are biased in favor of value, just say so, but don’t use the same argument to reach two opposite conclusions.)

There are a variety of explanations about why momentum works, but just because academics can’t agree on which one is correct doesn’t mean it won’t continue to work. It is certainly possible that any anomaly could be arbitraged away, but Robert Levy’s relative strength work has been known since the 1960s and our 2005 paper in Technical Analysis of Stocks & Commodities showed it continued to work just fine just the way he published it. Academics under the spell of efficient markets trashed his work at the time too, but 40 years of subsequent returns shows the professors got it wrong.

However, I do have a background in psychology and I can hazard a guess as to why both the value and momentum factors will continue to persist—they are both uncomfortable to implement. It is very uncomfortable to buy deep value. There is a terrific fear that you are buying a value trap and that the impairment that created the value will continue or get worse. It also goes against human nature to buy momentum stocks after they have already outperformed significantly. There is a great fear that the stock will top and collapse right after you add it to your portfolio. Investors and clients are quite resistant to buying stocks after they have already doubled, for example, because there is a possibility of looking really dumb.

Here’s the reason I think both factors are psychological in origin: it is absurdly easy to screen for either value or momentum. Any idiot can implement either strategy with any free screener on the web. Pick your value metric or your momentum lookback period and away you go. In fact, this is pretty much exactly what James O’Shaughnessy did in What Works on Wall Street. Both factors worked well—and continue to work despite plenty of publicity. So the barrier is not that there is some secret formula, it’s just that investors are unwilling to implement either strategy in a systematic way–because of the psychological discomfort.

If I were to make an argument—the behavioral finance version—about which smart beta factor could potentially be arbitraged away over time, I would have to guess low volatility. If you ask clients whether they would prefer to buy stocks that a) had already dropped 50%, b) had already gone up 50%, or c) had low volatility, I think most of them would go with “c!” (Although I think it’s also possible that aversion to leverage will keep this factor going.)

Value and momentum also happen to work very well together. Value is a mean reversion factor, while momentum is a trend continuation factor. As AQR has shown, the excess returns of these two factors (unsurprisingly, once you understand how they are philosophical opposites) are uncorrelated. Combining them may have the potential to smooth out an equity return stream a little bit. Regardless, two good return factors are better than one!

8 Comments | Investor Behavior, Portfolio Theory, Relative Strength and Value, Thought Process | Tagged: behavioral finance, investor behavior, momentum, portfolio theory, relative strength, systematic investment process, trend following, value | Permalink

Posted by:

Mike Moody

October 3, 2013

According to Morningstar, the whole idea of income-producing securities is flawed—and I think they are right. In an article entitled “Option Selling Is Not Income,” author Philip Guziec points out that option income is not mysterious free money. Option selling can modify the risk-reward tradeoff for a portfolio, but the income is part of the total return, not some extra money that happens to be lying around.

By way of explanation, he shows a chart of an option income portfolio without the reinvestment of the income. As you can see below, it’s pretty grim.

Source: Morningstar

(click on image to enlarge)

Why is that? Well, the plummeting line is the one where you spend the income instead of reinvesting it in the portfolio. So much for an income-producing security that has “free” income. In this graphic context, it is very clear that the income is just one part of the total return. (You can read the whole article—the link is above—if you want more information on the specifics of an option income portfolio.)

However, I thought the article was great for another reason. Mr. Guziec generalizes the case of option income funds to all income securities. He writes:

In fact, the very concept of an income-producing security is a fallacy. A dollar of return is a dollar of return, whether that return comes from capital gains, coupons, dividends, or option premium.

I put the whole thing in bold because 1) I think it is important, and 2) most investors do not understand this apparently simple point. This can be generalized to investors who refuse to buy certain stocks because they don’t “have enough yield” or who prefer high-yield bonds to investment-grade bonds simply because they “have more yield.” In both cases, income is just part of the total return—and may also move you to a different part of the risk-return spectrum. There is nothing magic about income-producing securities, whether they are MLPs, dividend stocks, bonds, or anything else. What matters is the total return.

From a mathematical standpoint, shaving 25 basis points off of your portfolio every month to spend is no different than spending a 3% dividend yield. Once you can wrap your head around this concept, it’s easy to pursue the best opportunities in the market because you aren’t wearing blinders or forcing investments through a certain screen or set of filters. If your portfolio grows, that 25 basis points keeps getting to be a bigger number and that’s really what matters.

6 Comments | Markets, Thought Process | Tagged: income-producing securities, investor behavior, retirement income | Permalink

Posted by:

Mike Moody

September 26, 2013

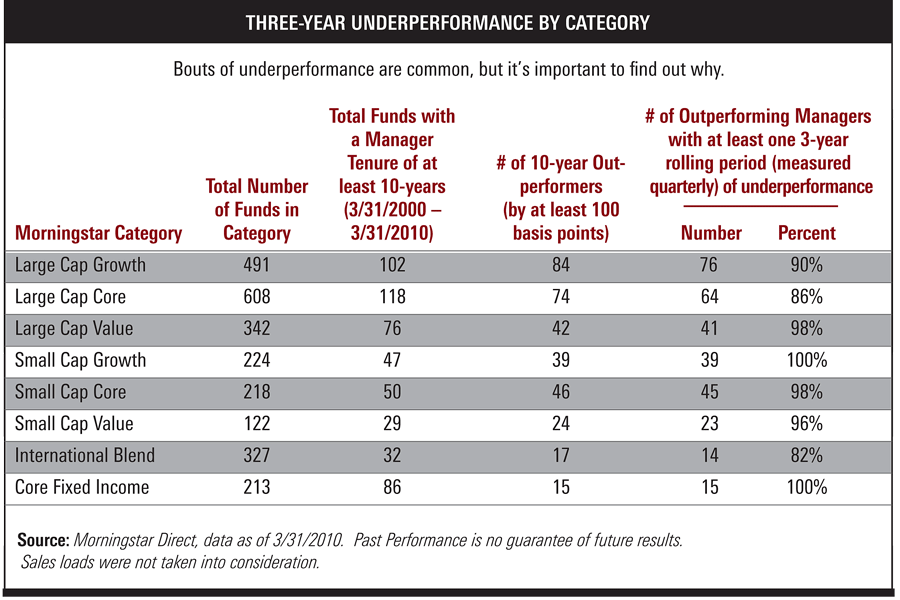

Whether you are an investment manager or a client, underperformance is a fact of life, no matter what strategy or methodology you subscribe to. If you don’t believe me, take a look at this chart from an article at ThinkAdvisor.

Source: Morningstar, ThinkAdvisor (click on image to enlarge)

Now, this chart is a little biased because it is looking at long periods of underperformance—3-year rolling periods—from managers that had top 10-year track records. In other words, these are exactly the kinds of managers you would hope to hire, and even they have long stretches of underperformance. When things are going well, clients are euphoric. Clients, though, often feel like even short periods of underperformance mean something is horribly wrong.

The entire article, written by Envestnet’s J. Gibson Watson, is worth reading because it makes the point that simply knowing about the underperformance is not very helpful until you know why the underperformance is occurring. Some underperformance may simply be a style temporarily out of favor, while other causes of underperformance might suggest an intervention is in order.

It’s quite possible to have a poor experience with a good manager if you bail out when you should hang in. Investing well can be simple, but that doesn’t mean it will be easy!

Comments Off on Underperformance | Markets, Thought Process | Tagged: behavioral finance, decision-making, investor behavior, patience, performance, underperformance | Permalink

Posted by:

Mike Moody

September 24, 2013

A recent article in the Personal Finance section of the Wall Street Journal had a prescription for anxious investors that Andy has been talking about for more than a year: consider asset allocation funds. Our Global Macro separate account has been very popular, partly because it allows investors to get into the market in a way that can be conservative when needed, but one that doesn’t lock investors into a product that can only be conservative.

The stock market’s powerful rally over the past year has gone a long way toward reducing the losses that many mutual-fund investors suffered in late 2007 and 2008.

But the rebound—with the Standard & Poor’s 500-stock index up 74% from its March 9, 2009, low—has done nothing for one group of investors: those who bailed out of stocks and have remained on the sidelines. Some of these investors have poured large sums into bond funds, even though those holdings may take a beating whenever interest rates rise from today’s unusually low levels, possibly later this year. Some forecasters, meanwhile, believe that stocks may finish 2010 up as much as 10%.

So, for investors who want to step back into stocks but are still anxious, here’s a modest suggestion: You don’t have to take your stock exposure straight up. You can dilute it by buying an allocation fund that spreads its assets across many market sectors, from stocks and bonds to money-market instruments and convertible securities.

While the WSJ article is a good general introduction to the idea, I think there are a few caveats that should be mentioned.

There’s still a big difference between a strategic asset allocation fund and a tactical asset allocation fund.

Many [asset allocation funds] keep their exposures within set ranges, while others may vary their mix widely.

Your fund selection will probably depend a lot on the individual client. A strategic asset allocation fund will more often have a tight range or even a fixed or target allocation for stocks or bonds. This can often target the volatility successfully–but can hurt returns if the asset classes themselves are out of favor. Tactical funds will more often have broader ranges or be unconstrained in terms of allocations. This additional flexibility can lead to higher returns, but it could be accompanied by higher volatility.

One thing the article does not mention at all, unfortunately, is that you also have a choice between a purely domestic asset allocation fund or a global asset allocation fund. A typical domestic asset allocation fund will provide anxious investors with a way to ease into the market, but will ignore many of the opportunities in international markets or in alternative assets like real estate, currencies, and commodities. With a variety of possible scenarios for the domestic economy, it might make sense to cast your net a little wider. Still, the article’s main point is valid: an asset allocation fund, especially a global asset allocation fund, is often a good way to deal with a client’s Market Anxiety Disorder and get them back into the game.

—-this article originally appeared 4/7/2010. Investors still don’t like this rally, even though we are a long way down the road from 2010! An asset allocation fund might still be a possible solution.

2 Comments | From the Archives, Investor Behavior, Markets, Tactical Asset Alloc, Thought Process | Tagged: asset allocation, investor behavior, Tactical Asset Allocation | Permalink

Posted by:

Andy Hyer

September 9, 2013

John Rekenthaler at Morningstar launched into a spirited defense of buy and hold investing over the weekend. His argument is essentially that since markets have bounced back since 2009, buy and hold is alive and well, and any arguments to the contrary are flawed. Here’s an excerpt:

There never was any logic behind the “buy-and-hold is dead” argument. Might it have lucked into being useful? Not a chance. Coming off the 2008 downturn, the U.S. stock market has roared to perhaps its best four and a half years in history. It has shone in absolute terms, posting a cumulative gain of 125% since spring 2009. It has been fabulous in real terms, with inflation being almost nonexistent during that time period. It’s been terrific in relative terms, crushing bonds, cash, alternatives, and commodities, and by a more modest amount, beating most international-stock markets as well. This is The Golden Age. We have lived The Golden Age, all the while thinking it was lead.

Critics will respond that mine is a bull-market argument. That’s backward. “Buy-and-hold is dead” is the strategy that owes its existence to market results. It only appears after huge bear markets, and it only looks good after such markets. It is the oddity, while buy-and-hold is the norm.

Generally, I think Morningstar is right about a lot of things—and Rekenthaler is even right about some of the points he makes in this article. But in broad brush, buy and hold has a lot of problems, and always has.

Here’s where Rekenthaler is indisputably correct:

- “Buy and hold is dead” arguments always pop up in bear markets. (By the way, that says nothing about the accuracy of the argument.) It’s just the time that anti buy-and-holders can pitch their arguments when someone might listen. In the same fashion, buy and hold arguments are typically made after a big recovery or in the midst of a bull market—also when people are most likely to listen. Everyone has an axe to grind.

- Buy and hold has looked good in the past, compared to forecasters. As he points out in the article, it is entirely possible to get the economic forecast correct and get the stock market part completely wrong.

- The 2008 market crash gave the S&P; 500 its largest calendar year loss in 77 years. No doubt.

The truth about buy and hold, I think, is considerably more nuanced. Here are some things to consider.

- The argument for buy and hold rests on hindsight bias. Historical returns in the US markets have been among the strongest in history over very long time periods. That’s why US investors think buy and hold works. If buy and hold truly works, what about Germany, Argentina, or Japan at various time periods? The Nikkei peaked in 1989. Almost 25 years later, the market is still down significantly. Is the argument, then, that only the US is special? Is Mr. Rekenthaler willing to guarantee that US returns will always be positive over some time frame? I didn’t think so. If not, then buy and hold is not a slam dunk either.

- Individual investors have time frames. We only live so long. A buy and hold retiree in 1929 or 1974 might be dead before they got their money back. Same for a Japanese retiree in 1989. Plenty of other equity markets around the world, due to wars or political crises, have gone to zero. Zero. That makes buy and hold a difficult proposition—it’s a little tough mathematically to bounce back from zero. (In fact, the US and the UK are the only two markets that haven’t gone to zero at some point in the last 200 years.) And plenty of individual stocks go to zero. Does buy and hold really make sense with stocks?

- Rejecting buy and hold does not have the logical consequence of missing returns in the market since 2009. For example, a trend follower would be happily long the stock market as it rose to new highs.

- Individual investors, maddeningly, have very individual tolerances for volatility in their portfolios. Some investors panic too often, some too late, and a very few not at all. How that works out is completely path dependent—in other words, the quality of our decision all depends on what happens subsequently in the market. And no one knows what the market will do going forward. You don’t know the consequences of your decision until some later date.

- In our lifetimes, Japan. It’s funny how buy and hold proponents either never mention Japan or try to explain it away. “We are not Japan.” Easy to say, but just exactly how is human nature different because there is an ocean in between? Just how is it that we are superior? (Because in 1989, if you go back that far, there was much hand-wringing and discussions of how the Japanese economy was superior!)

Every strategy, including buy and hold, has risks and opportunity costs. Every transaction is a risk, as well as an implicit bet on what will happen in the future. The outcome of that bet is not known until later. Every transaction, you make your bet and you take your chances. You can’t just assume buy and hold is going to work forever, nor can you assume it will stop working. Arguments about any strategy being correct because it worked over x timeframe is just a good example of hindsight bias. Buy and hold doesn’t promise good returns, just market returns. Going forward, you just don’t know—nobody knows. Yes, ambiguity is uncomfortable, but that’s the way it is.

That’s the true state of knowledge in financial markets: no one knows what will happen going forward, whether they pretend to know or not.

2 Comments | Investor Behavior, Markets, Tactical Asset Alloc, Thought Process | Tagged: behavioral finance, buy-and-hold, investor behavior, market, stock market, trend following | Permalink

Posted by:

Mike Moody

September 6, 2013

Marshall Jaffe wrote an excellent article on investment process versus investment performance in the most recent edition of ThinkAdvisor. I think it is notable for a couple of reasons. First, it’s pithy and well-written. But more importantly, he’s very blunt about the problems of focusing only on investment performance for both clients and the industry. And make no mistake—that’s how the investment industry works in real life, even though it is a demonstrably poor way to do things. Consider this excerpt:

We see the disclaimer way too often. “Past performance is no guarantee of future results.” It is massively over-used—plastered on countless investment reports, statements and research. It’s not simply meaningless; it’s as if it’s not even there. And that creates a huge problem, because the message itself is really true: Past performance has no predictive value.

Since we are looking for something that does have predictive value—all the research, experience and hard facts say: Look elsewhere.

This is not a controversial finding. There are no fringe groups of investors or scholars penning op-ed pieces in the Wall Street Journal shooting holes in the logic of this reality. Each year there is more data, and each year that data reconfirms that past performance is completely unreliable as an investment tool. Given all that, you would think it would be next to impossible to find any serious investors still using past performance as a guideline. Indeed, that would be a logical conclusion.

But logical conclusions are often wrong when it comes to understanding human behavior. Not only does past performance remain an important issue in the minds of investors, for the vast majority it is the primary issue. In a study I referred to in my August column, 80% of the hiring decisions of large and sophisticated institutional pension plans were the direct result of outstanding past performance, especially recent performance.

The truth hurts! The bulk of the article discusses why investors focus on performance to their detriment and gives lots of examples of top performers that focus only on process. There is a reason that top performers focus on process—because results are the byproduct of the process, not an end in themselves.

The reason Nick Saban, our best athletes, leading scientists, creative educators, and successful investors focus on process is because it anchors them in reality and helps them make sensible choices—especially in challenging times. Without that anchor any investor observing the investment world today would be intimidated by its complexity, uncomfortable with its volatility and (after the meltdown in 2008) visibly fearful of its fragility. Of course we all want good returns—but those who use a healthy process realize that performance is not a goal; performance is a result.

Near the end of the article, I think Mr. Jaffe strikes right to the core of the investment problem for both individual investors and institutions. He frames the right question. Without the right question, you’re never going to get the right answer!

In an obsessive but fruitless drive for performance too many fund managers compromise the single most important weapon in their arsenal: their investment process.

Now we can see the flaw in the argument that an investor’s basic choice is active or passive. An investor indeed has two choices: whether to be goal oriented or process oriented. In reframing the investment challenge that way, the answer is self-evident and the only decision is whether to favor a mechanical process or a human one.

Reframing the question as “What is your investment process?” sidelines everything else. (I added the bold.) In truth, process is what matters most. Every shred of research points out the primacy of investment process, but it is still hard to get investors to look away from performance, even temporarily.

We focus on relative strength as a return factor—and we use a systematic process to extract whatever return is available—but it really doesn’t matter what return factor you use. Value investors, growth investors, or firms trying to harvest more exotic return factors must still have the same focus on investment process to be successful.

If you are an advisor, you should be able to clearly explain your investment process to a client. If you are an investor, you should be asking your advisor to explain their process to you. If there’s no consistent process, you might want to read Mr. Jaffe’s article again.

HT to Abnormal Returns

1 Comment | From the MM, Investor Behavior, Markets, Thought Process | Tagged: investment process, investor behavior, relative strength, return factor, systematic investment process | Permalink

Posted by:

Mike Moody

September 4, 2013

I’ve long been a fan of portfolio buckets or sleeves, for two reasons. The first reason is that it facilitates good diversification, which I define as diversification by volatility, by asset class, and by strategy. (We happen to like relative strength as one of these primary strategies, but there are several offsetting strategies that might make sense.) A bucket portfolio makes this kind of diversification easy to implement.

The second benefit is largely psychological—but not to be underestimated. Investors with bucket portfolios had better performance in real life during the financial crisis because they didn’t panic. While the lack of panic is a psychological benefit, the performance benefit was very real.

Another champion of bucketed portfolios is Christine Benz at Morningstar. She recently wrote a series of article in which she stress-tested bucketed portfolios, first through the 2007-2012 period (one big bear market) and then through the 2000-2012 period (two bear markets). She describes her methodology for rebalancing and the results.

If you have any interest in portfolio construction for actual living, breathing human beings who are prone to all kinds of cognitive biases and emotional volatility, these articles are mandatory reading. Better yet for fans of portfolio sleeves, the results kept clients afloat. I’ve included the links below. (Some may require a free Morningstar registration to read.)

Article: A Bucket Portfolio Stress Test http://news.morningstar.com/articlenet/article.aspx?id=605387∂=1

Article: We Put the Bucket System Through Additional Stress Tests http://news.morningstar.com/articlenet/article.aspx?id=607086

Article: We Put the Bucket System Through a Longer Stress Test http://news.morningstar.com/articlenet/article.aspx?id=608619

2 Comments | From the MM, Investor Behavior, Portfolio Theory, Thought Process | Tagged: behavioral finance, bucket, diversification, investor behavior, portfolio theory, relative strength | Permalink

Posted by:

Mike Moody

September 3, 2013

What the heck is fictive learning? Well, I’m glad you asked. Fictive learning refers to our ability to imagine “what if” situations. We learn not only from our actual actions, but from our perceptions of what would have happened if we had done something differently. It turns out that fictive learning has a lot to do with investor behavior too. Here are a few excerpts about relevant experiments discussed in an article in Wired magazine.

To better understand the source of our compulsive speculation, Read Montague, a neuroscientist now at Virginia Tech, has begun investigating the formation of bubbles from the perspective of the brain. He argues that the urge to speculate is rooted in our mental software. In particular, bubbles seem to depend on a unique human talent called “fictive learning,” which is the ability to learn from hypothetical scenarios and counterfactual questions. In other words, people don’t just learn from mistakes they’ve actually made, they’re able to learn from mistakes they might have made, if only they’d done something different.

Investors, after all, are constantly engaging in fictive learning, as they compare their actual returns against the returns that might have been, if only they’d sold their shares before the crash or bought Google stock when the company first went public. And so, in 2007, Montague began simulating stock bubbles in a brain scanner, as he attempted to decipher the neuroscience of irrational speculation. His experiment went like this: Each subject was given $100 and some basic information about the “current” state of the stock market. After choosing how much money to invest, the players watched nervously as their investments either rose or fell in value. The game continued for 20 rounds, and the subjects got to keep their earnings. One interesting twist was that instead of using random simulations of the stock market, Montague relied on distillations of data from famous historical markets. Montague had people “play” the Dow of 1929, the Nasdaq of 1998 and the S&P; 500 of 1987, so the neural responses of investors reflected real-life bubbles and crashes.

Montague, et. al. immediately discovered a strong neural signal that drove many of the investment decisions. The signal was fictive learning. Take, for example, this situation. A player has decided to wager 10 percent of her total portfolio in the market, which is a rather small bet. Then, she watches as the market rises dramatically in value. At this point, the investor experiences a surge of regret, which is a side-effect of fictive learning. (We are thinking about how much richer we would be if only we’d invested more in the market.) This negative feeling is preceded by a swell of activity in the ventral caudate, a small area in the center of the cortex. Instead of enjoying our earnings, we are fixated on the profits we missed, which leads us to do something different the next time around.

When markets were booming, as in the Nasdaq bubble of the late 1990s, people perpetually increased their investments. In fact, many of Montague’s subjects eventually put all of their money into the rising market. They had become convinced that the bubble wasn’t a bubble. This boom would be different.

And then, just like that, the bubble burst. The Dow sinks, the Nasdaq collapses, the Nikkei implodes. At this point investors race to dump any assets that are declining in value, as their brain realizes that it made some very expensive mistakes. Our investing decisions are still being driven by regret, but now that feeling is telling us to sell. That’s when we get a financial panic.

Montague has also begun exploring the power of social comparison, or what he calls the “country club effect,” on the formation of financial bubbles. “This is what happens when you’re sitting around with your friends at the country club, and they’re all talking about how much money they’re making in the market,” Montague told me. “That casual conversation is going to change the way you think about investing.” In a series of ongoing experiments, Montague has studied what happens when people compete against each other in an investment game. While the subjects are making decisions about the stock market, Montague monitors their brain activity in two different fMRI machines. The first thing Montague discovered is that making more money than someone else is extremely pleasurable. When subjects “win” the investment game, Montague observes a large increase in activity in the striatum, a brain area typically associated with the processing of pleasurable rewards. (Montague refers to this as “cocaine brain,” as the striatum is also associated with the euphoric high of illicit drugs.) Unfortunately, this same urge to outperform others can also lead people to take reckless risks.

More recently, a team of Italian neuroscientists led by Nicola Canessa and Matteo Motterlini have shown that regret is also contagious, so that “observing the regretful outcomes of another’s choices reactivates the regret network.” (In other words, we internalize the errors of others. Or, as Motterlini wrote in an e-mail, “We simply live their emotions like these were our own.”) Furthermore, this empathy impacts our own decisions: The “risk-aptitude” of investors is significantly shaped by how well the risky decisions of a stranger turned out. If you bet the farm on some tech IPO and did well, then I might, too.

If you are an investment advisor, all of this is sounding pretty familiar. We’ve all seen clients make decisions based on social comparison, regret, or trying to avoid regret. Sometimes they are simply paralyzed, trapped between wanting to do as well as their brother-in-law and wanting to avoid the regret of losing money if their investment doesn’t work out.

The broader point is that a lot of what drives trends in the market is rooted in human behavior, not valuations and fundamentals. Human nature is unlikely to change, especially a feature like fictive learning which is actually incredibly helpful in many other contexts. As a result, markets will continue to trend and reverse, to form bubbles and to have those bubbles implode periodically.

While social science may be helpful in understanding why the market behaves as it does, we still have to figure out a way to navigate it. As long as markets trend, relative strength trend following should work. (That’s the method we follow.) As long as bubbles form and implode, other methods like buying deep value should help mitigate the risk of permanent loss. Most important, the discipline to execute a systematic investment plan and not get sucked into all of the cognitive biases will be necessary to prosper with whatever investment method you choose.

180 Comments | From the MM, Investor Behavior, Thought Process | Tagged: behavioral finance, fictive learning, investor behavior, relative strength, systematic investment process | Permalink

Posted by:

Mike Moody

August 28, 2013

At first, you might not think that relative strength and philosophy are related in any way. But they are, because every strategy is based on some philosophy of the market. Different philosophies lead to different strategies. We like relative strength because it is simple, straightforward, and performs well over time. Of course, there are other strategies that work also, including some that are quite complementary to relative strength. A nice encapsulation of philosophy leading to strategy appeared on The Bloodhound System blog. A couple of excerpts from the article are instructive. The first is a quote from Rick Ferri in a Morningstar interview:

“Strategy comes from philosophy. If you don’t have a philosophy, you can develop a strategy, but it’s only going to blow apart the next time it doesn’t work for a month or two. And you are going to go onto another strategy, and that’s the worst thing you can do.”

This is very true. Over my career, I’ve seen many investors careen from strategy to strategy, never sticking long enough with any of them to enjoy success. The author of the blog piece, Bill Moore, I think really cuts to the core of why a deeply held philosophy is so important to success. Having some kind of belief system is necessary to have conviction. With conviction comes discipline—and discipline is the key to everything. I put the good part in bold.

…what’s really important is that you have a philosophy that makes sense to you and that you believe in–and that you then create a strategy which you would execute with discipline. As much as pundits might dogmatically espouse one investing philosophy or another–making it seem like it’s their way or the highway–there are thousands of investment philosophies–and in turn strategies. The reason multiple philosophies can work out well is that inherent in having a philosophy, or belief system, is that you have conviction in it. That kind of discipline, not so much the philosophy itself, is the key to an investment plan.

One of our senior portfolio managers, Harold Parker, likes to say “to the disciplined go the spoils.” He’s right. Even a good strategy that is poorly executed will lead to bad results. Every strategy might be driven by some philosophy, but none of them are worth a darn without conviction and the resultant discipline to execute well.

Comments Off on Relative Strength and Philosophy | From the MM, Investor Behavior, Thought Process | Tagged: investor behavior, relative strength, strategy | Permalink

Posted by:

Mike Moody

August 23, 2013

Avoiding danger is no safer in the long run than outright exposure. The fearful are caught as often as the bold.—Helen Keller

I doubt that Helen Keller was thinking about bond investors when she wrote this, but she may as well have been. The safe haven trade hasn’t worked out too well since May. Bond investors sometimes think they have an extra measure of security versus stock investors. And it is true that most bonds are less volatile than stocks. Volatility, however, is a pretty poor way to measure risk. An alternative way to measure risk is to look at drawdown—and measured that way, bonds have had drawdowns in real returns that rival drawdowns in stocks.

In truth, bonds are securities just like stocks. They are subject to the same, sometimes irrational, swings in investor emotion. And given that bonds are priced based on the income they produce, they are very vulnerable to increases in interest rates and increases in inflation.

So I think that Helen Keller’s point is well taken—instead of pretending that you are safe, make sure you understand the exposures you have and make sure you take them on intentionally.

Source: Wikipedia (click on image to enlarge)

9 Comments | From the MM, Thought Process | Tagged: drawdown, investor behavior, portfolio theory, risk | Permalink

Posted by:

Mike Moody

August 19, 2013

Every time I read an article about how active investing is hopeless, I shake my head. Most of the problem is investor behavior, not active investing. The data on this has been around for a while, but is ignored by indexing fans. Consider for example, this article in Wealth Management that discusses a 2011 study conducted by Morningstar and the Investment Company Institute. What they found doesn’t exactly square out with most of what you read. Here are some excerpts:

But studies by Morningstar and the Investment Company Institute (ICI) suggest that fund shareholders may not be so dumb after all. According to the latest data, investors gravitate to low-cost funds with strong track records. “People make reasonably intelligent choices when they pick active funds,” says John Rekenthaler, Morningstar’s vice president of research.

The academic approach produces a distorted picture, says Rekenthaler. “It doesn’t matter what percentage of funds trail the index,” says Rekenthaler. “What matters most is how the big funds do. That’s where most of the money is.”

In order to get a realistic picture of fund results, Rekenthaler calculated asset-weighted returns—the average return of each invested dollar. Under his system, large funds carry more weight than small ones. He also calculated average returns, which give equal weight to each fund. Altogether Morningstar looked at how 16 stock-fund categories performed during the ten years ending in 2010. In each category, the asset-weighted return was higher than the result that was achieved when each fund carried the same weight.

Consider the small-growth category. On an equal-weighted basis, active funds returned 2.89 percent annually and trailed the benchmark, which returned 3.78 percent. But the asset-weighted figure for small-growth funds exceeded the benchmark by 0.20 percentage points. Categories where active funds won by wide margins included world stock, small blend, and health. Active funds trailed in large blend and mid growth. The asset-weighted result topped the benchmark in half the categories. In most of the eight categories where the active funds lagged, they trailed by small margins. “There is still an argument for indexing, but the argument is not as strong when you look at this from an asset-weighted basis,” says Rekenthaler.

The numbers indicate that when they are choosing from among the many funds on the market, investors tend to pick the right ones.

Apparently investors aren’t so dumb when it comes to deciding which funds to buy. Most of the actively invested money in the mutual fund industry is in pretty good hands. Academic studies, which weight all funds equally regardless of assets, don’t give a very clear picture of what investors are actually doing.

Where, then, is the big problem with active investing? There isn’t one—the culprit is investor behavior. As the article points out:

But investors display remarkably bad timing for their purchases and sales. Studies by research firm Dalbar have shown that over the past two decades, fund investors have typically bought at market peaks and sold at troughs.

Active investing is alive and well. (I added the bold.) In fact, the recent trend toward factor investing, which is just a very systematic method for making active bets, reinforces the value of the approach.

The Morningstar/ICI research just underscores that much of the value of an advisor may lie in helping the client control their emotional impulse to sell when they are fearful and to buy when they feel confident. I think this is often overlooked. If your client has a decent active fund, you can probably help them more by combatting their destructive timing than you can by switching them to an index fund. After all, owning an index fund does not make the investor immune to emotions after a 20% drop in the stock market!

5 Comments | From the MM, Investor Behavior, Markets, Thought Process | Tagged: factor investing, investor behavior, systematic investment process | Permalink

Posted by:

Mike Moody

July 2, 2013

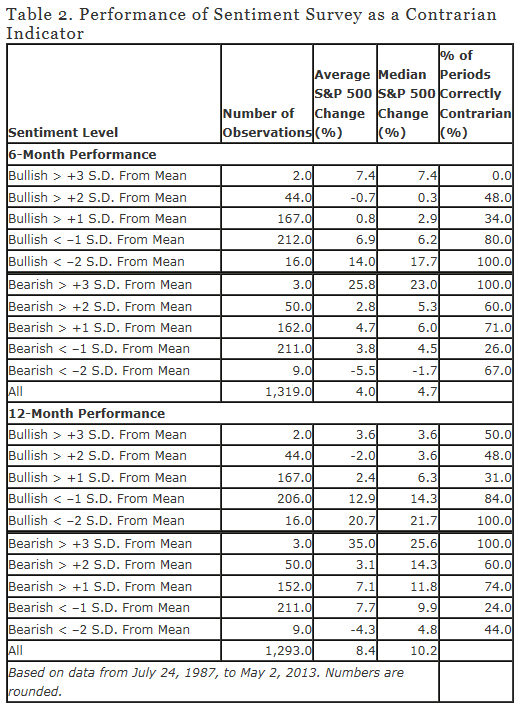

Greenbackd, a deep value blog, had a recent piece on the value of stock market sentiment. Stock market sentiment surveys have been a staple of technical analysis for decades, ever since the advent of Investors Intelligence in the 1960s, so I was curious to read it. The study that Greenbackd referenced was done by Charles Rotblut, CFA. The excerpts from Mr. Rotblut that are cited give the impression that the results from the survey are unimpressive. However, they showed a data table from the article. I’ll reproduce it here and let you draw your own conclusions.

Source: Greenbackd (click on image to enlarge)

From Greenbackd, here’s an explanation of what you are looking at:

Each week from Thursday 12:01 a.m. until Wednesday at 11:59 p.m. the AAII asks its members a simple question:

Do you feel the direction of the stock market over the next six months will be up (bullish), no change (neutral) or down (bearish)?

AAII members participate by visiting the Sentiment Survey page (www.aaii.com/sentimentsurvey) on AAII.com and voting.

Bullish sentiment has averaged 38.8% over the life of the survey. Neutral sentiment has averaged 30.5% and bearish sentiment has averaged 30.6% over the life of the survey.

In order to determine whether there is a correlation between the AAII Sentiment Survey and the direction of the market, Rotblut looked at instances when bullish sentiment or bearish sentiment was one or more standard deviations away from the average. He then calculated the performance of the S&P; 500 for the following 26-week (six-month) and 52-week (12-month) periods. The data for conducting this analysis is available on the Sentiment Survey spreadsheet, which not only lists the survey’s results, but also tracks weekly price data for the S&P; 500 index.

There are some possible methodological problems with the survey since it is not necessarily the same investors answering the question each week (Investors Intelligence uses something close to a fixed sample of newsletter writers), but let’s see if there is any useful information embedded in their responses.

The way I looked at it, even the problematic AAII poll results were very interesting at extremes. When there were few bulls (more than 2 standard deviations from the mean) or tons of bears (more than 3 standard deviations from the mean), the average 6-month and 12-month returns were 2x to 5x higher than normal for the 1987-2013 sample. These extremes were rare—only 19 instances in 26 years—but very useful when they did occur. (And it’s possible that there were really only 16 instances if they were coincident.)

Despite the methodology problems, the data shows that it is very profitable to go against the crowd at extremes. Extremes are times when the emotions of the crowd are likely to be most powerful and tempting to follow—and most likely to be wrong. Instead of bailing out at times when the crowd is negative, the data shows that it is better to add to your position.

HT to Abnormal Returns

1 Comment | Investor Behavior, Portfolio Theory | Tagged: investor behavior, sentiment, stock market | Permalink

Posted by:

Mike Moody

June 28, 2013

Jason Zweig has written one of the best personal finance columns for years, The Intelligent Investor for the Wall Street Journal. Today he topped it with a piece that describes his vision of personal finance writing. He describes his job as saving investors from themselves. It is a must read, but I’ll give you a couple of excerpts here.

I was once asked, at a journalism conference, how I defined my job. I said: My job is to write the exact same thing between 50 and 100 times a year in such a way that neither my editors nor my readers will ever think I am repeating myself.

That’s because good advice rarely changes, while markets change constantly. The temptation to pander is almost irresistible. And while people need good advice, what they want is advice that sounds good.

The advice that sounds the best in the short run is always the most dangerous in the long run. Everyone wants the secret, the key, the roadmap to the primrose path that leads to El Dorado: the magical low-risk, high-return investment that can double your money in no time. Everyone wants to chase the returns of whatever has been hottest and to shun whatever has gone cold. Most financial journalism, like most of Wall Street itself, is dedicated to a basic principle of marketing: When the ducks quack, feed ‘em.

In practice, for most of the media, that requires telling people to buy Internet stocks in 1999 and early 2000; explaining, in 2005 and 2006, how to “flip” houses; in 2008 and 2009, it meant telling people to dump their stocks and even to buy “leveraged inverse” exchange-traded funds that made explosively risky bets against stocks; and ever since 2008, it has meant touting bonds and the “safety trade” like high-dividend-paying stocks and so-called minimum-volatility stocks.

It’s no wonder that, as brilliant research by the psychologist Paul Andreassen showed many years ago, people who receive frequent news updates on their investments earn lower returns than those who get no news. It’s also no wonder that the media has ignored those findings. Not many people care to admit that they spend their careers being part of the problem instead of trying to be part of the solution.

My job, as I see it, is to learn from other people’s mistakes and from my own. Above all, it means trying to save people from themselves. As the founder of security analysis, Benjamin Graham, wrote in The Intelligent Investor in 1949: “The investor’s chief problem – and even his worst enemy – is likely to be himself.”

……..

From financial history and from my own experience, I long ago concluded that regression to the mean is the most powerful law in financial physics: Periods of above-average performance are inevitably followed by below-average returns, and bad times inevitably set the stage for surprisingly good performance.

But humans perceive reality in short bursts and streaks, making a long-term perspective almost impossible to sustain – and making most people prone to believing that every blip is the beginning of a durable opportunity.

……..

But this time is never different. History always rhymes. Human nature never changes. You should always become more skeptical of any investment that has recently soared in price, and you should always become more enthusiastic about any asset that has recently fallen in price. That’s what it means to be an investor.

Simply brilliant. Unless you write a lot, it seems deceptively easy to write this well and clearly. It is not. More important, his message that many investment problems are actually investor behavior problems is very true—and has been true forever.

To me, one of the chief advantages of technical analysis is that it recognizes that human nature never changes and that, as a result, behavior patterns recur again and again. Investors predictably panic when market indicators get deeply oversold, just when they should consider buying. Investors predictably want to pile into a stock that has been a huge long-term winner when it breaks a long-term uptrend line—because “it’s a bargain”—just when they might want to think about selling. Responding deliberately at these junctures doesn’t usually require the harrowing activity level that CNBC commentators seem to believe is necessary, but can be quite effective nonetheless. Technical indicators and sentiment surveys often show these turning points very clearly, but as Mr. Zweig describes elsewhere in the article, the financial universe is arranged to deceive us—or at least to tempt us to deceive ourselves.

Investing is one of the many fields where less really is more.

1 Comment | From the MM, Investor Behavior | Tagged: behavioral finance, investor behavior, investor sentiment, technical analysis | Permalink

Posted by:

Mike Moody

June 12, 2013

From Barry Ritholz at The Big Picture comes a great article about what he calls “competency transference.” His article was triggered by a Bloomberg story about a technology mogul who turned his $1.8 billion payoff into a bankruptcy just a few years later. Mr. Ritholz points out that the problem is generalizable:

Be aware of what I call The Fallacy of Competency Transference. This occurs when someone successful in one field jumps in to another and fails miserably. The most widely known example is Michael Jordan, the greatest basketball player the game has ever known, deciding he was also a baseball player. He was a .200 minor league hitter.

I have had repeated conversations with Medical Doctors about this: They are extremely intelligent accomplished people who often assume they can do well in markets. (After all, they conquered what I consider a much more challenging field of medicine).

The problem they run into is that competency transference. After 4 years of college (mostly focused on pre-med courses), they spend 4 years in Medical school; another year as an Interns, then as many as 8 years in Residency. Specialized fields may require training beyond residency, tacking on another 1-3 years. This process is at least 12, and as many as 20 years (if we include Board certification).

What I try to explain to these highly educated, highly intelligent people is that they absolutely can achieve the same success in markets that they have as medical professionals — they just have to put the requisite time in, immersing themselves in finance (like they did in medicine) for a decade or so. It is usually around this moment that the light bulb goes off, and the cause of prior mediocre performance becomes understood.

To me, the funny thing is that competency transference mostly applies to the special case of financial markets. For example, no successful stock market professional would ever, ever assume themselves to be a competent thoracic surgeon without the requisite training. Nor would a medical doctor ever assume that he or she could play a professional sport or run a nuclear submarine without the necessary skills. (I think the Michael Jordan analogy is a poor one, since there have been numerous multi-sport athletes. Many athletes letter in multiple sports in high school and some even play more than one in college. Michael Jordan may have been wrong about his particular case, but it wasn’t necessarily a crazy idea.)

Nope, competency transference is mostly restricted to the idea that anyone watching CNBC can become a market maven. (Apparently even talking heads on CNBC believe this.) This creates no end of grief in advisor-client relationships if 1) the advisor isn’t very far up the learning curve, and 2) if the client thinks they know better. You would have the same problem if you had a green medical doctor and you thought you knew more than the doctor did. That is a situation that is ripe for problems!

Advisors need to work continuously to expand their skills and knowledge if they are to be of use to investors. And investors, in general, would do well to spend their efforts vetting advisors carefully rather than assuming financial markets are a piece of cake.

1 Comment | From the MM, Investor Behavior, Markets | Tagged: financial markets, investor behavior, stock market | Permalink

Posted by:

Mike Moody

June 5, 2013

Motley Fool had an excellent article by Morgan Housel on a couple of the most common cognitive biases that cause problems for investors, cognitive dissonance and confirmation bias. The information is not new, but what makes this article so fun is Housel’s writing style and good analogies. A couple of excerpts should suffice to illuminate the problem with cognitive biases.

Study successful investors, and you’ll notice a common denominator: They are masters of psychology. They can’t control the market, but they have complete control over the gray matter between their ears.

And lucky them. Most of us, on the other hand, are mental catastrophes. As investor Barry Ritholtz once put it:

You’re a monkey. It all comes down to that. You are a slightly clever, pants-wearing primate. If you forget that you’re nothing more than a monkey who has been fashioned by eons on the plains, being chased by tigers, you shouldn’t invest. You have to be aware of how your own psychology affects what you do.